Mad Hedge Technology Letter

February 10, 2025

Fiat Lux

Featured Trade:

(SILICON VALLEY GHOST CITY)

(AMZN), (GOOGL), (MSFT), (DEEPSEEK)

Mad Hedge Technology Letter

February 10, 2025

Fiat Lux

Featured Trade:

(SILICON VALLEY GHOST CITY)

(AMZN), (GOOGL), (MSFT), (DEEPSEEK)

This AI infrastructure build-out is starting to smell more and more like the Chinese ghost city phenomenon.

Yeh, I said it.

It is starting to feel more like that type of “growth”, and that is not good for the future of tech stocks.

If the AI build-out becomes something trending closer to a Chinese ghost city, then we can expect a sharp pullback in tech stocks.

When that abrupt pullback will be is the hard question to answer, but each day we inch closer to that scenario.

There are 65 million empty homes in China that were built by developers and registered as “growth.” This type of parallel growth or paper growth can’t be ignored, and the concrete producers and wiring folks made large fortunes off that whole racket.

Sam Altman, head of OpenAI, is starting to seem more like one of these construction contractors selling 65 million appliances and calling it a success while the apartments are unused and investors get fleeced.

Wasteful spending by corporations swept into the dustbin of history. Looks more like it by the day.

When tech managers are asked about the specific numbers about what kind of revenue we can expect from the AI investment, they tell us to “spend now and ask questions later.”

That is a massive red flag, and I am calling out the whole movement now.

That being said, I bought the dip in mid-January on the Deepseek news, and I am riding that technical reversion to profits as it stands.

If there are no short-term pullbacks, we will end the month up over 15% YTD.

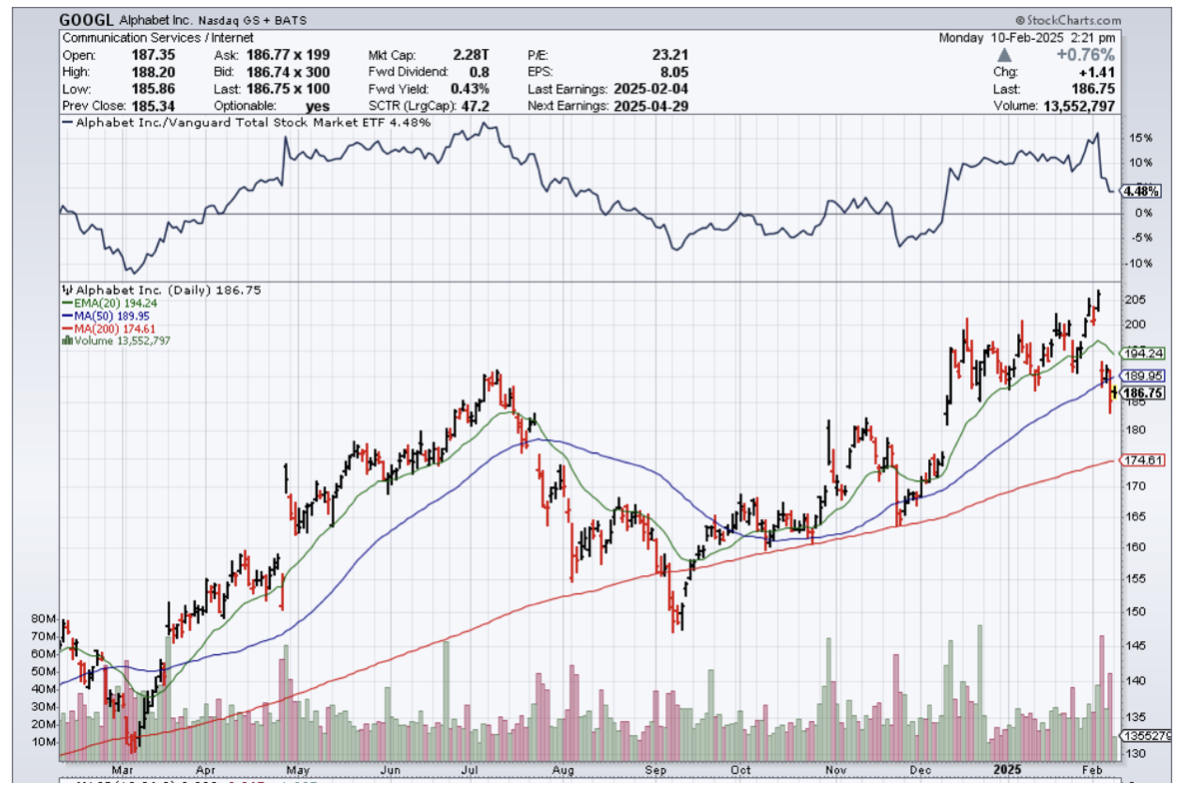

Meta (META), Microsoft (MSFT), Amazon (AMZN), and Google parent Alphabet (GOOGL) are expecting to spend a cumulative $325 billion in capital expenditures and investments in 2025, driven by a continued commitment to building out artificial intelligence infrastructure.

Taken together, this marks a 46% increase from the roughly $223 billion those companies reported spending in 2024.

The Chinese startup Deepseek rattled markets last week after it debuted open-source AI models competitive with OpenAI’s for a fraction of the price. Tech stocks sold off across the board as the model cast doubt on the rationale behind tech giants’ mammoth spending on artificial intelligence infrastructure.

But the DeepSeek surprise didn't seem to impact tech companies' big spending plans.

Amazon is by far the biggest spender on capital investments of the group, with its $78 billion for 2024 far eclipsing Microsoft's $56 billion and Alphabet's $53 billion.

Looking ahead, Amazon said in a post-earnings call Thursday evening that its spending of $26.3 billion in its most recent quarter is "reasonably representative" of its 2025 investment plans, suggesting investments will total roughly $105 billion this year.

Late last month, Meta confirmed that it would spend $60 billion-$65 billion in 2025, a massive bump from its prior guidance to investors of $38 billion-$40 billion in investment for the year.

Google said on Tuesday that it expects to spend $75 billion this year.

In the short-term, I expect earnings reports to be met with a selloff producing optimal buying opportunities.

These dips are bought by traders then take profits – rinse and repeat.

It’s not guaranteed that tech will go up in a straight line, so it’s better to use the volatility in your favor for some profits.

“The goal of auditing the Social Security Administration is to stop the extreme levels of fraud taking place, so that it remains solvent and protects the social security checks of honest Americans! That’s it. That’s the goal. End of story.” – Said Elon Musk

Mad Hedge Technology Letter

February 7, 2025

Fiat Lux

Featured Trade:

(TESLA IS IN A PICKLE)

(TSLA)

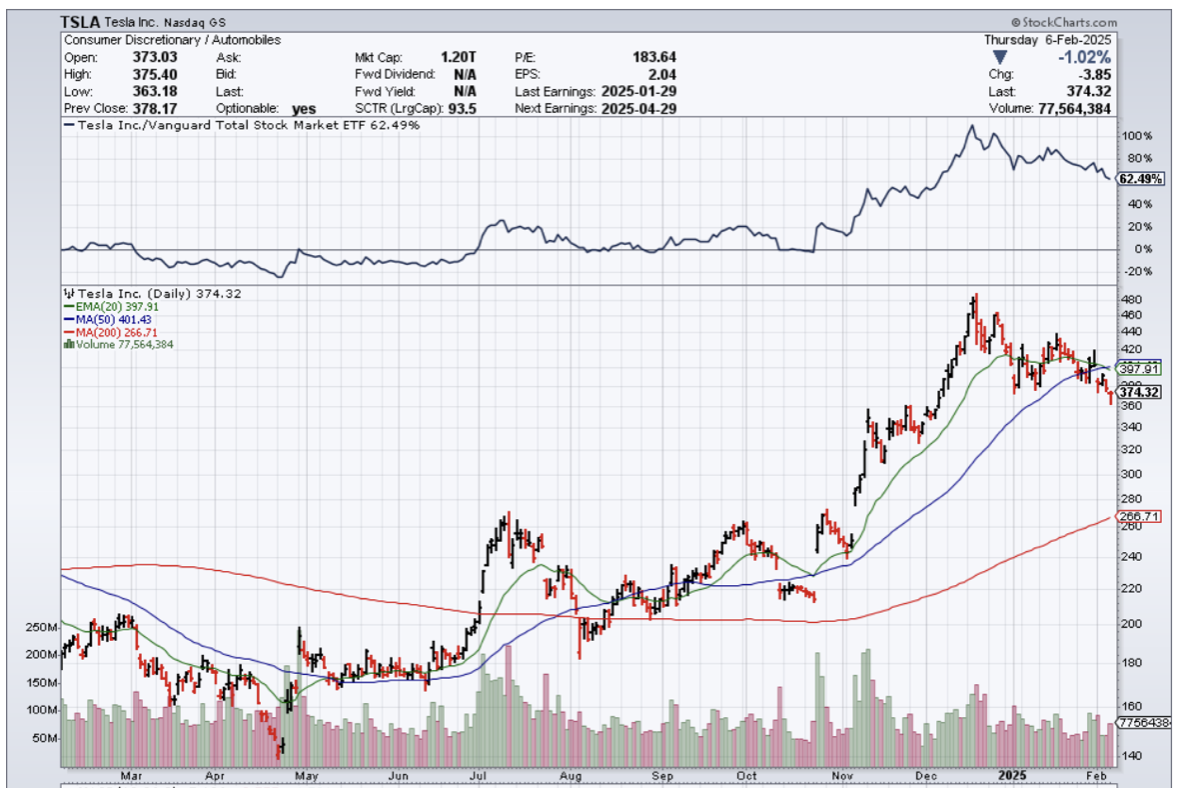

Tesla stock has been falling since the mid of last December, and I expect the short-term trajectory of the stock to be a real slippery slope.

There are a variety of factors causing the stock to struggle.

I won’t ignore the issue that the eccentric and strongly opinionated CEO Elon Musk has aggressively inserted himself into European politics and turning off the political establishment in Europe, which has always been radically left, is just asking for trouble.

It’s my opinion that he has essentially written off doing business in Europe and is throwing his efforts on making political inroads in the old continent.

Long term, I am not sure Musk can compete against the Chinese pricing power, and securing political gains in Western government will help his empire grow.

His sights have shifted away from EVs to rockets, and the stock will likely suffer from this.

Don’t forget that Europeans are facing a stark and grueling cost of living crisis that is degrees of magnitudes worse than what is happening in the United States.

Interesting that Americans complain that rental costs consume half the salary, but in Europe, tenant obligations via leases consume 100% of the average white-color job salary.

The end result is that young Europeans cannot afford to buy cars, whether it be gas powered or electric.

How bad are things for Tesla?

Sales of its EVs dropped 13% in the European Union in 2024.

They are also facing growing pressure as Chinese and Euorpean rivals launch a wave of cheaper electric vehicles.

Tesla saw big drops in sales in major markets dominated by ultra-progressive politics like Germany, France, and Italy.

In Germany, the hub of Europe's auto industry and the home of Tesla's Berlin gigafactory, sales of Tesla vehicles fell by 41% in 2024, outstripping the 27% sales decline in the general battery EV market.

Swedish brand Volvo, which is owned by Chinese conglomerate Geely, saw its sales rise nearly 30% in the EU last year, driven by the popularity of its $40,000 EX30 electric crossover.

Several German companies have announced they will stop buying Tesla vehicles over Musk's political and social comments in recent months.

This trend is likely to grow in 2025.

Musk has also become entangled in UK politics, feuding with British Prime Minister Keir Starmer.

I expect Musk's active political involvements to have a damaging impact on Tesla's European sales for the foreseeable future, and rivals would likely reap the benefit of disgruntled Tesla owners ditching their vehicles.

Tesla makes a great car – I don’t deny that.

Musk has already sold 2 to 3 EVs to every Western progressive that could ever want an EV. Conservatives aren’t interested in EVs. Try selling a Tesla in rural Poland to a Polish milk farmer where it would be almost impossible to find a charging station. EVs are almost entirely reserved for an urban environment where EV infrastructure is beefy and widespread.

Since Musk cannot get that EV sales growth boost in the short-term, he is riding on the coattails of the global populist movement to secure political victories, and it is working to his benefit.

At the end of the day, consumers would ultimately be more concerned about factors such as price and performance, rather than Musk's politics, but with people who can afford buying multiple EVs in Europe, they care about the name on your passport, the university you went to, and especially your political views.

Europe is just like that, and Musk is going ahead and alienating the European market.

In the short-term, I don’t see a lot of individual catalysts that could boost Tesla in the short-term, although after the Deepseek black swan, Tesla could ride a general tech market revision to the mean rally.

Let’s hope the general tech market heals itself from the Deepseek nuclear bomb, but I would stay away from Tesla in the short-term and opt for something more attractive in tech like Meta or Netflix in 2025.

Mad Hedge Technology Letter

February 5, 2025

Fiat Lux

Featured Trade:

(AMAZON DOESN’T NEED WORKERS)

(AMZN), (AAPL)

Flatten the curve!

No, I am not talking about that 2020 thing, I am talking about the CEO of Amazon Andy Jassy’s vendetta to remove the middle manager tier out of the company he runs.

Flatten the curve so there is no more middle manager and everyone is on the same level with higher-ups rejoicing with the entry levels.

Everything sounds ideal, right?

So why buy this company’s stock?

Why do it?

Easy answer – the stock price goes higher.

Jassy’s campaign to gut the bloat out including the higher earners of Amazon is ringing alarm bells within the employee ecosystem at Amazon.

Amazon is probably the worst FANG company to search for a job at this point. I would never recommend it to a friend.

The thing about Jeff Bezos, he paid his employees well and promised promotions and lots of other perks.

Jassy is promising the inverse and employee morale has fallen off a cliff then mixed into the fact that workers now go back to the office 5 days per week when the standard at other tech companies is a hybrid 3 days per week in-office requirement.

Tried and Tested Amazon's career paths are drying up faster than the Salt Lake in Utah.

Managers fear replacement by lower-paid people with less experience and half a brain.

Jassy has even coined a new term “horizontal development” which he wants workers to understand as a fake promotion.

Jassy even codified his philosophy into a published 1,400-word manifesto for change on Amazon’s corporate blog — where investors could read it — and appears to have targeted an entire layer of middle managers.

Jassy is pressuring HR to hire from a pool of recent college graduates to fill positions while finding reasons to remove more senior workers.

Jassy’s cost-cutting has helped increase profits in each of the past six quarters, and the shares have surged 42% in the last 12 months.

Targeting middle managers rather than front-line workers has become more common recently in corporate America because these people tend to have higher salaries and usually don’t contribute directly to a project by coding or negotiating deals.

Like 2024, I do believe Amazon has a great chance at defying the tech malaise by pushing the financials over the line.

The stock will be rewarded by a higher share price.

Let’s be straight, Amazon isn’t reinventing the wheel.

There is no big new shiny thing to hang their hat on.

But much like Tim Cook came in for Steven Jobs, Jassy has come in for Jeff Bezos to operate the hell out of Amazon and search for nickels in the corner of every couch.

Sadly, that is what has come of Silicon Valley and the “most innovative” place in the world.

The truth is that Silicon Valley isn’t innovating like it used to aside from a few people like the guy who figured out how to re-use rockets.

However, Amazon and Silicon Valley don’t need to offer something new when there is little competition besides the Chinese (which are taking over the iPhone and EV business).

Unluckily for China, it’s harder for the Chinese to replace a foreign e-commerce and logistics company while easier to rip off a smartphone.

Buy the dip in Amazon in 2025.

Mad Hedge Technology Letter

February 3, 2025

Fiat Lux

Featured Trade:

(TARIFFS COME FOR TECH STOCKS)

(NVDA), (META)

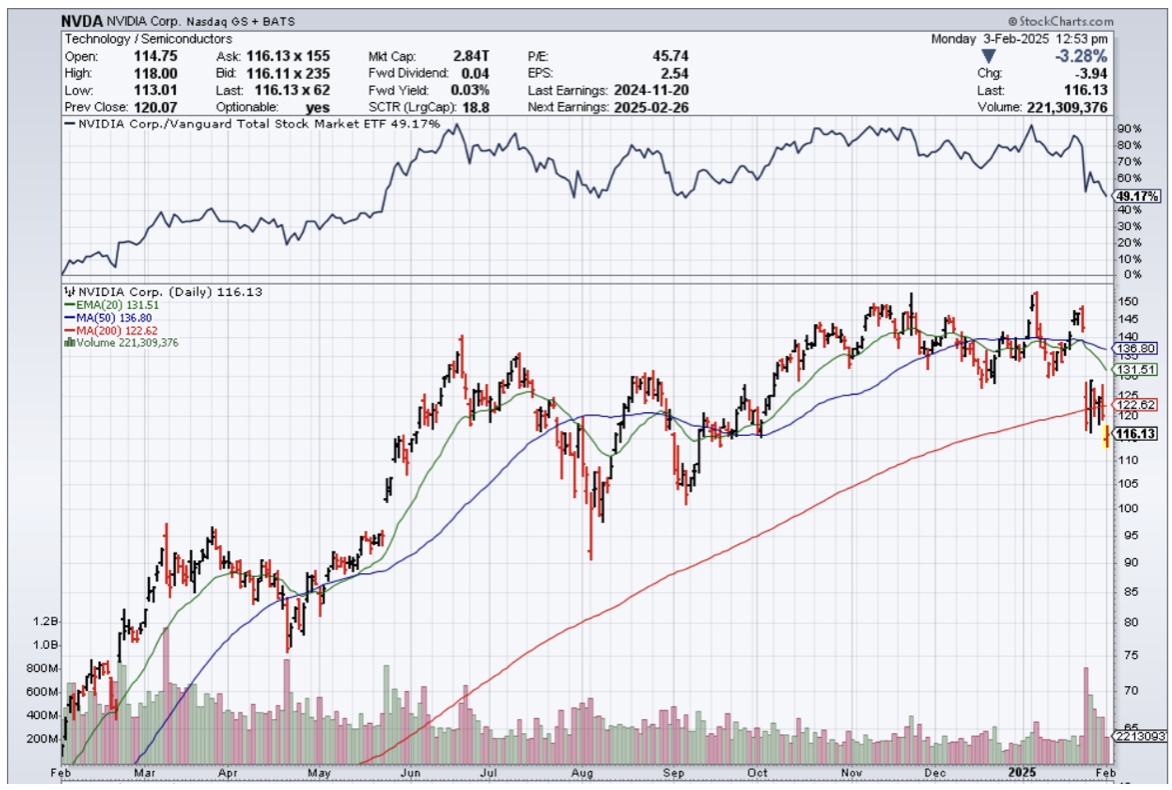

Tech stocks have felt the full effect of the volatile nature of the new federal government in charge in Washington.

Tech stocks aren’t looking too pretty today.

The new admin levied a 25% tariff on goods from Mexico only to give the Mexicans a 1-month reprieve.

Like a game of high-stakes poker, but Trump is wielding the American economy at the poker table with reckless abandon.

Tech stocks whipsawed and most stocks opened up in the red, however, a stock like Meta was able to ride out the instability by surging at the open.

Not all tech stocks are created equal.

If many investors thought Trump wouldn’t follow through with his sabre-rattling, then think again.

He is hell-bent on going full throttle and pushing allies to the brink whether they can tolerate it or not.

The surge in interest rates because of the perception of higher inflation and higher geopolitical risk was the reason tech stocks were jolted at the beginning of this week.

Indeed, tech stocks are in for a sideways correction if American government policy becomes constantly aggressive and brutal.

Tech stocks will have a narrow path to go higher, but not like the prior 10 years when stocks were cheered higher by almost everyone.

Trump said this will boost US manufacturing.

The tariffs will grow the US economy, protect jobs, and raise tax revenue, he argues.

Canada’s Trudeau declared retaliatory 25% tariffs on $107 billion dollars worth of US goods on Saturday.

Mexican President Claudia Sheinbaum has directed the Secretary of Economy to impose a plan including "tariff and non-tariff measures in defense of Mexico's interests".

Together, China, Mexico, and Canada accounted for more than 40% of imports into the US last year.

Most goods from Mexico don’t affect tech stocks such as fruits like avocado, vegetables, tequila, and beer.

Canadian goods such as steel, lumber, grains, and potatoes are also likely to get pricier.

It is expected that the car manufacturing sector could see the brunt of the effects of the tariff.

It’s not like Trump is only going after Mexico and Canada, he also has the U.K. and Europe in his crosshairs.

Do tariffs cause inflation?

In the short term, tariffs will hit consumers in the U.S. with corporations front-running price increases by passing on the higher inputs to the end buyer.

The market also senses higher inflation and interest rate yields will get bid up, which is negative for tech stocks.

It is naïve to think that tech stocks will go up in a straight line like the past 10 years – they certainly will not.

If the government is hell-bent on this type of tactic, global markets will feel the pain.

Even if this doesn’t directly affect tech stocks, the American consumer will not go unscathed.

Interest rates exploding higher will certainly mean tech stocks opening up Monday mornings 3% down.

That is not a good starting point for the week and explains why the bellwether Nvidia (NVDA) is down 15% year to date.

Then throw in the chaos from the Deepseek fiasco that threatens the valuations of many AI stocks.

It’ll be tough sledding from here on out and tech investors need to be mindful to not get caved in out of nowhere.

Mad Hedge Technology Letter

January 31, 2025

Fiat Lux

Featured Trade:

(AMAZON CUTS OFF THE OUTSIDE)

(AMZN), (UPS)