Mad Hedge Technology Letter

October 4, 2024

Fiat Lux

Featured Trade:

(TECH WANTS TO GET RID OF LABOR COSTS)

(TSLA), (NVDA)

Mad Hedge Technology Letter

October 4, 2024

Fiat Lux

Featured Trade:

(TECH WANTS TO GET RID OF LABOR COSTS)

(TSLA), (NVDA)

Unshackling the restraints on human labor – that is where tech is headed.

I’m talking about AI.

Robots aren’t able to perform complicated tasks and that is the holy grail of AI.

If headway is made just on this one issue then the sky is the limit.

Profits are then unlimited and the world will change into something we could have never imagined.

If stakes weren’t high enough, the next explosive leg up in tech shares is now centered on this concept.

There is only so much balance sheet maneuvering can add to the bottom line.

Magnificent 7 stocks who are experts are juicing up the balance sheet will gradually run out of levers to pull.

Technology stocks demand that management move the needle along because the alternative is that the company will get left behind.

When the Department of Defense commenced its robotics challenge in 2015, the stated goal was to develop ground robots that can aid in disaster recovery with the help of human operators.

Nearly a decade later, generative AI is accelerating that learning curve, pushing human-like machines to pick up new tasks in real-time.

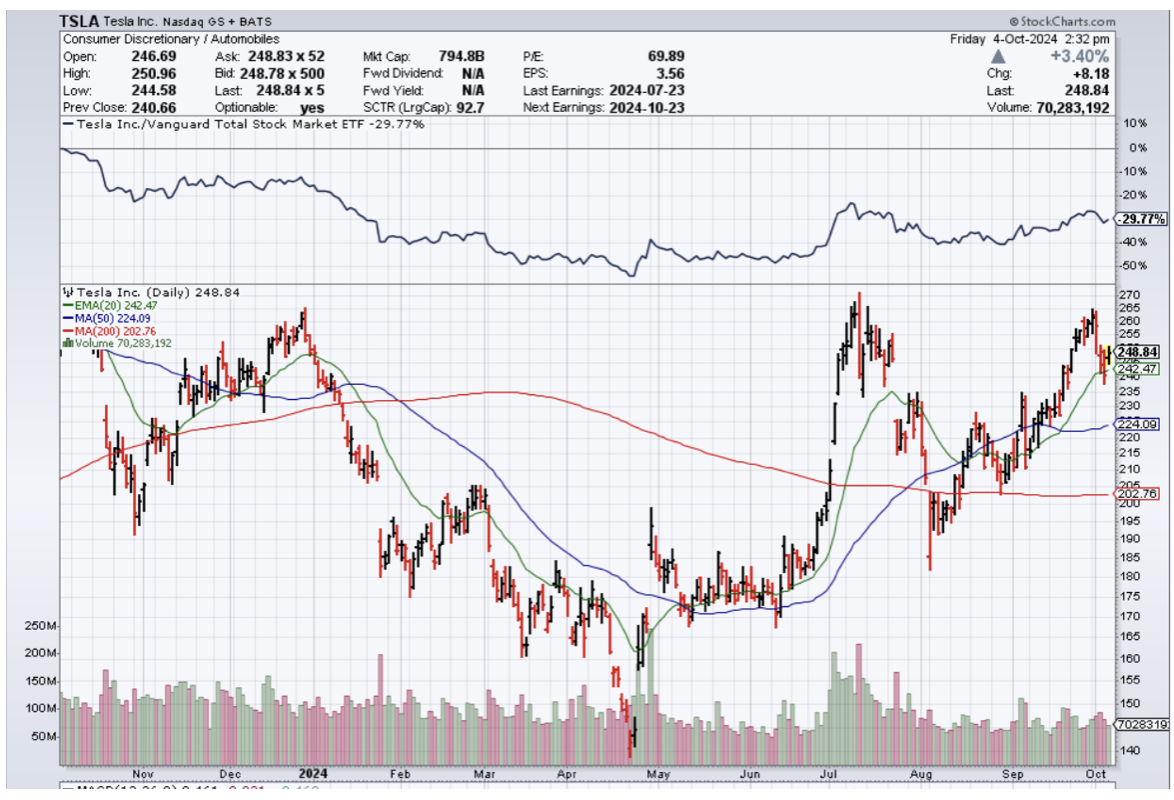

And just recently, Tesla (TSLA) presented an updated version of its Optimus robot at Tesla’s Investor Day and showed it roaming a factory floor. CEO Elon Musk touted the robot’s potential, saying it had the ability to push the company’s market cap to $25 trillion.

Humanoids that can adapt to existing environments have long been seen as the ultimate test if they can work alongside humans in spaces built for them.

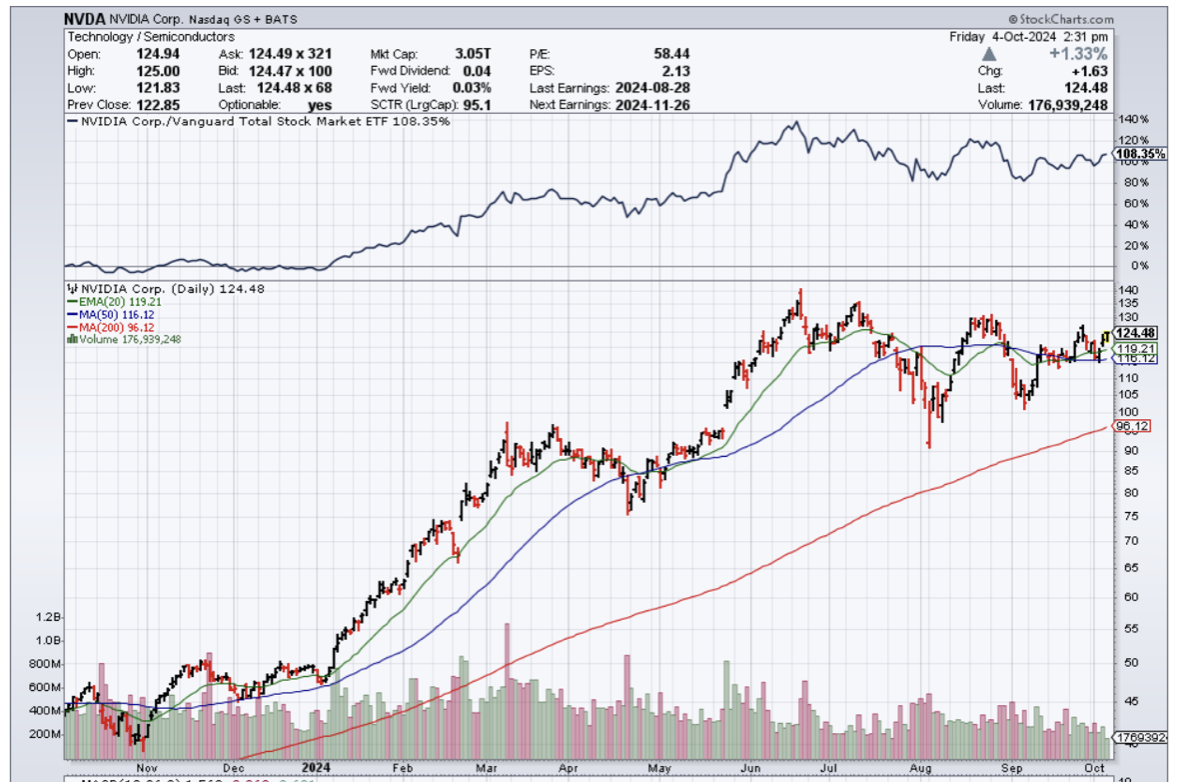

Nvidia (NVDA) is driving rapid development through an ecosystem built specifically for humanoids. It combines high-powered chips that process data at high speeds with a digital world that allows users to train robots on skills applied in the real world.

Just this past summer, Nvidia unveiled “NIM Microservices,” a visual training ground that allows generative AI models to visually interpret their surroundings in 3D.

Nvidia’s ecosystem now enables robots to train using text and speech input, in addition to live demonstrations.

Humanoids have already begun taking their first steps into reality. Musk has said two Optimus robots are working at Tesla’s Fremont factory, and he expects a few thousand to be deployed by next year. Amazon (AMZN) has partnered with Oregon-based Agility to utilize its Digit robot at a test facility. Apptronik is working with Mercedes-Benz to integrate Apollo into its manufacturing line.

The goal is to adapt humanoid for the future which will allow them to operate beyond industrial use. They could become as ubiquitous if companies are able to scale and bring costs down to $10,000 per machine.

Technology is still in the stage of calculating how they bring the expenses under control.

It is not very cost-effective if a company needs to spend 5 times the actual cost of running the AI division on retrofitting the environment for a humanoid and resetting the language models for different tasks.

Much of these technical aspects are being worked out, and these companies are inching their way closer to a day when companies might be able to work fully without a human worker or alongside a minimum amount of workers.

Tesla is a company long-term that needs to be looked at and this assumption is solely based on their robotics and humanoid business. It is highly plausible that Elon Musk is at peace with sacrificing his EV business in the medium time as long as moving up the value chain to become the leader of what is next which is looking more like robotics using AI.

Musk is skating to where the puck is next and that is where the future will be.

Mad Hedge Technology Letter

October 2, 2024

Fiat Lux

Featured Trade:

(INFLATION COULD AFFECT TECH STOCKS)

($COMPQ)

Either way, accelerating inflation is coming back.

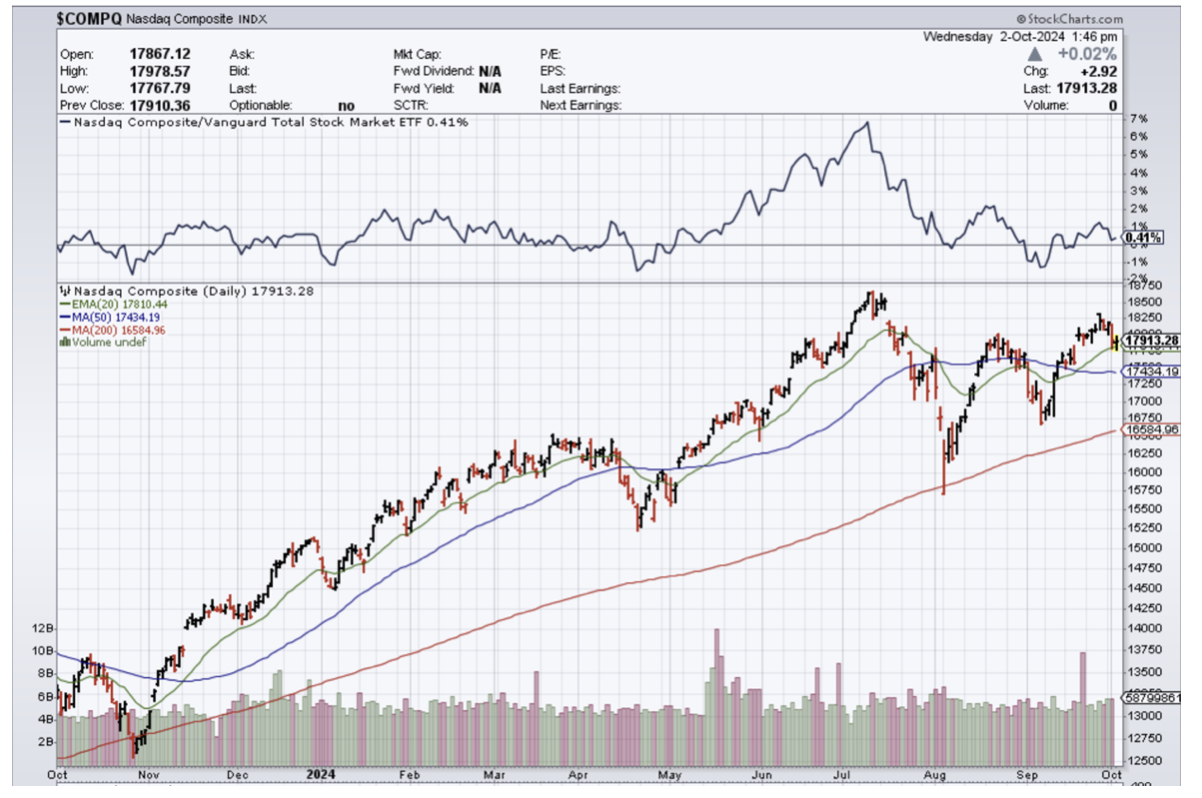

What does that mean for your tech portfolio ($COMPQ)?

It is complicated is the simple answer, and prices threaten to escalate because of the economic disruption ahead caused by the International Longshoremen's Association (ILA) protesting at 14 major ports along the East and Gulf coasts, halting container traffic from Maine to Texas.

This fight is first about pay but more about rejecting automation.

The action marks the first such shutdown in almost 50 years.

On Monday, USMX (United States Maritime Alliance) said it had increased its offer, which would raise wages by almost 50%, triple employers' contributions to pension plans, and strengthen health care options.

USMX has accused the union of refusing to bargain, filing a complaint with labor regulators that asked them to order the union back to the table.

The union wants to see per-hour pay increase by five dollars per year over the life of the six-year deal, which he estimated amounted to about 10% per year.

Imports in the US surged over the summer as many businesses took steps to rush shipments ahead of the strike.

She said more than 100,000 people could find themselves temporarily out of work as the impact of the stoppage spreads.

That would hit consumers and businesses which tend to rely on so-called "just-in-time" supply chains for goods, he added.

In case you are wondering, it takes an estimated 4-8 years to convert a port to full automation and between $500 million to $2B.

For reference, Shanghai’s Yangshan port took about 4-6 years from conception to full operations.

Yangshan’s port barely needs humans to operate, and it mostly down by a handful of IT guys behind computers.

They don’t need 50,000 people to do the job.

Clearly, the amount of job destruction is something that the longshoremen association is aware of and is actively fighting against modernization.

What it does mean is that Americans will pay higher prices.

Higher inflation will result in rising bond yield, which will strengthen the dollar.

Last time, the US dollar skyrocketed, tech prices rose during covid, and the rest of the equity market sank relative to big tech except energy stocks.

The USMX is fighting against any and all automation, shows the gaining power of unions in the United States.

Tech firms have been cutting staff in bunches and automating as fast as possible with AI.

With the possibilities of another covid-style shortage of many everyday goods, price inflation could return instantly, and that is very bad news for the S&P and Dow index.

The tech-heavy Nasdaq has proven that it fights calamities quite well and is durable in times of catastrophe, albeit if the electricity and keyboard are still functioning.

Ultimately, I see chaos happening and, at best, agreed on wage hikes that are not insignificant that will be passed on to the consumer.

From what I can understand, each time chaos rears its ugly head in the United States, tech somehow is unscathed in the aftermath and benefits.

If crazy wage increases are agreed on, get ready for another tech rally, and even if there is a long work stoppage, tech will gain over any other sector.

With interest rates dropping, it is hard not to see tech stocks experiencing a melt-up going into yearend, even if bond yields spike higher because of external events outside the realm of tech.

Automation is coming for all industries, and the longshoremen are trying to kick the can down the road at the expense of the end customer.

I am bullish tech going into Christmas.

Mad Hedge Technology Letter

September 30, 2024

Fiat Lux

Featured Trade:

(CHINESE TECH GLITTERS IN THE SHORT-TERM)

(BABA), (JD), (PDD), (BIDU)

The bazookas have been unloaded, and the results are big.

The aftermath is reverberating through the rest of the world’s equity markets.

The Chinese economy is in the dumps and the Chinese communist party is using every tool in the proverbial toolkit to pull them out of their slump.

Juxtapose that in the face of a demographic time bomb and we could say that it is in the nick of time.

Now that we have decades of data on the issue, the Chinese economy has major structural issues and instead of fixing it, they are throwing liquidity at it.

Chinese purchasing power is about to drop through the toilet pipes, but I believe bellwether stocks like Alibaba (BABA), JD.com (JD), Pinduoduo (PDD), and Baidu (BIDU) will perform quite well.

China is all about ecommerce at the retail level anyway and Alibaba will be able to reverse a years-long slump on the back of Beijing’s sweeping stimulus measures.

Flooding the system with liquidity will paper over the cracks and should get consumers out and about instead of eating instant noodles in their little apartments.

Retail is now moving in the right direction again.

Although, long term this does nothing to address the major structural issues in the system, the short-term transfusion should help putting money in consumer’s pockets and liquidity on Chinese corporates will outperform.

Market-support measures initiated by the People’s Bank of China included mortgage rate cuts and an unprecedented $114 billion stock-buying facility.

The renewed positive market sentiment for Alibaba reflects its resilience after struggling in recent years, owing to Beijing’s 32-month crackdown on Big Tech firms and the mainland’s shaky post-pandemic economic recovery.

BABA lost nearly half their value over the past five years.

China’s largest operator of online shopping platforms and a major domestic artificial intelligence (AI) technology player, Alibaba recently won praise from the State Administration for Market Regulation for complying with rectification measures, ending more than three years of regulatory scrutiny that has hung over the company’s operations.

Alibaba’s cloud computing services unit last week announced at an event in Hangzhou the release of more than 100 large language models – the deep-learning technology underpinning generative AI applications like ChatGPT – to the global open-source community and a new text-to-video model, as the company showed its rapid progress in this field.

Earlier this month, Alibaba founder Jack Ma called on employees of the business empire he created 25 years ago to “believe in the future” and “believe in the market” amid stiff competition.

The Chinese Communist Party and their heavy handed approach has a lot to do with many tech companies fizzling out.

It is impossible to really kick start growth when they are suppressing it.

However, now is the time when the government has realized they are overdoing it and have unleashed the animal spirits.

Ultimately, the Chiense government is the arbiter of who gets to do business and how well in China.

In the short-term, Chinese tech stocks will outperform American tech stocks.

Chinese tech stocks are cheap by almost every metric – buy the dip in Chinese tech.

Mad Hedge Technology Letter

September 27, 2024

Fiat Lux

Featured Trade:

(CHIPS SHINE THROUGH AGAIN)

(MU), (NVDA)

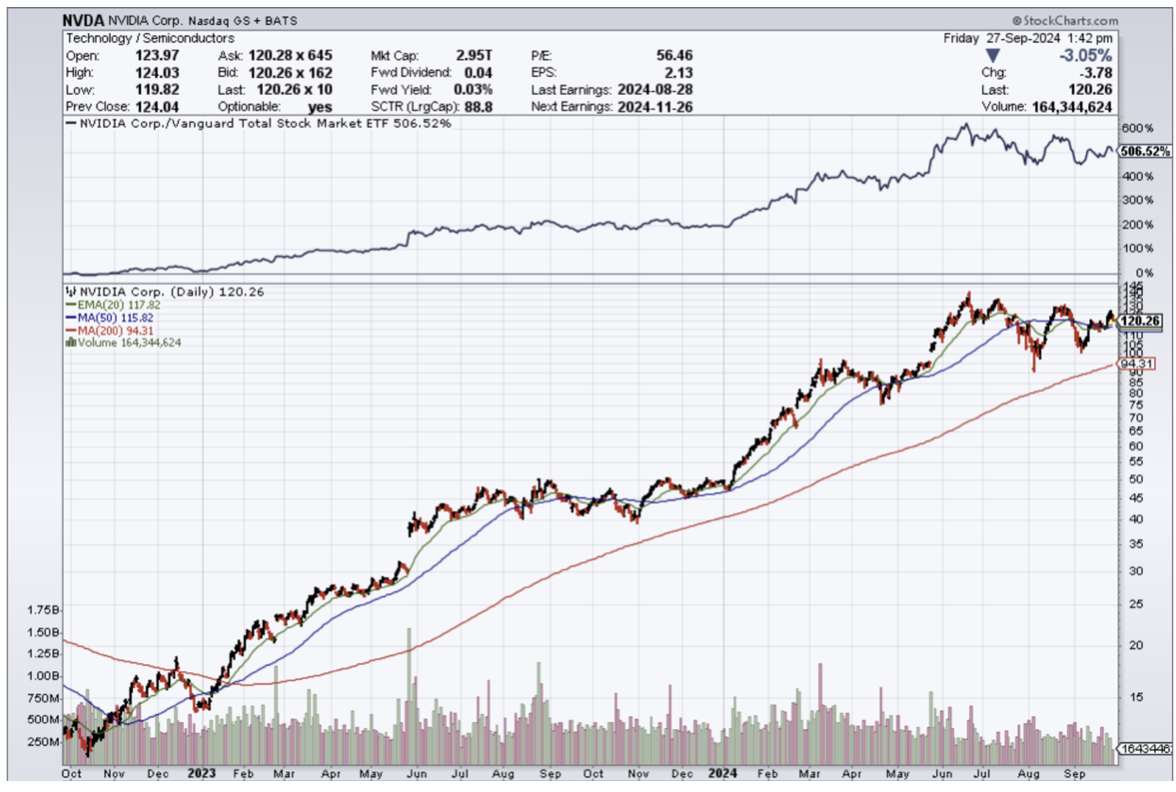

I have been pounding on the table urging my readers to buy chip stocks.

Why?

Because chip stocks will carry the Nasdaq to higher highs.

Jump on the bandwagon while you can.

My thesis was validated when Micron stock (MU) jumped over 17% yesterday and is up over 20% for the week.

That type of stock appreciation isn’t as widely found in the tech sector anymore now that much of the tech sector is deadweight.

The sub-sector that isn’t dead weight is chips and specifically the AI chips which Micron is part of.

So when we talk about growth, you won’t hear stuff like earnings or revenue growing in the single digits.

We hear numbers more similar to revenue growing at 90% or 100% or even 300% in some cases.

The outperformance in growth is helping these stocks reach greater heights and this is just the beginning.

The commentary has been widespread that AI data spend on chips is going through the roof.

Micron’s management told us they raised guidance because of a more favorable pricing environment as well as robust demand for Micron's memory chips used in data centers to power artificial intelligence.

Executives now expect the market for high-bandwidth memory (HBM) chips used in AI data centers to increase to $25 billion in 2025, up from $5 billion this year — and heightened demand for its HBM chips to bring in multiple billions of dollars next year.

Micron is the first chipmaker to report quarterly results this earnings season and their stellar earnings bode well for the rest of its peers.

The company reported revenue of $7.75 billion — 93% higher than last year.

Micron distinguishes itself by partnering with, rather than competing against, industry superpower Nvidia (NVDA). Micron supplies memory chips for Nvidia’s hotly demanded GPUs.

The company is also set to benefit from a bill awaiting signature from President Joe Biden that would loosen environmental requirements for microchip projects funded by the CHIPS and Science Act. Micron is one of the biggest beneficiaries of CHIPS Act funding, and the Building Chips in America Act passed by the US House of Representatives Monday would allow it to access funding for its projects in Idaho and New York faster.

It is quite transparent that these companies cannot make enough chips in the short term and tech companies are throwing money at them to try to produce the supply that is required for the AI build-out.

Whatever you think of how many AI chips will be needed to deploy AI in full capacity - the real number will dwarf that.

The energy generation needed to power this new technology is so immense that it could even raise the temperature of the earth a few degrees from the sheer energy it will emit.

We are at the beginning of the AI revolution and the chips are currently the best way to play it.

I am bullish chip companies who produces AI chips.

“Rule No. 1 is never lose money. Rule No. 2 is never forget Rule No. 1.” – Said American investor Warren Buffett

Mad Hedge Technology Letter

September 25, 2024

Fiat Lux

Featured Trade:

(FROM 85 to 2,000 AI DATA CENTERS)

(ORCL), (NVDA)