“It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” – Said American Investor Warren Buffett

“It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” – Said American Investor Warren Buffett

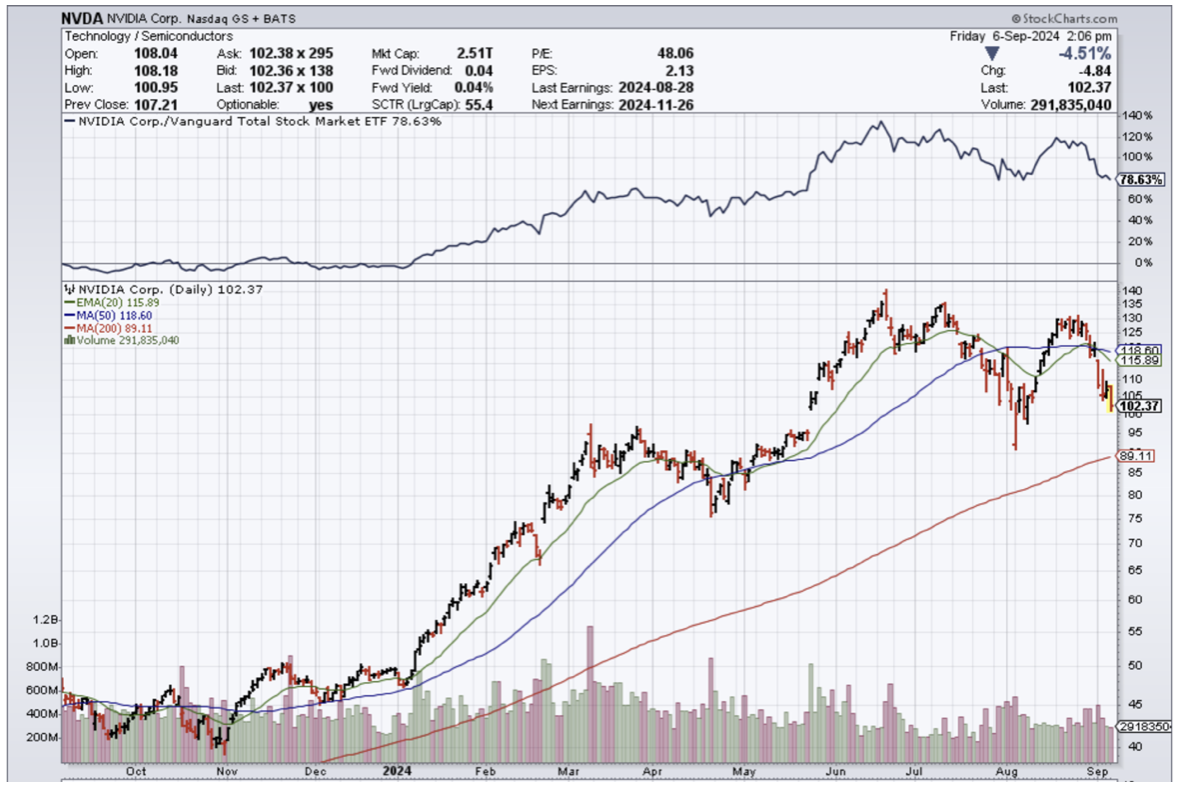

Mad Hedge Technology Letter

September 6, 2024

Fiat Lux

Featured Trade:

(BROADCOM A LONG-TERM WINNER)

(AI), (NVDA), (AVGO),

The chip trade isn’t in the dumps, but traders are taking a fine tooth comb to earnings guidance to see if the numbers are stacking up with the hype.

Today we got yet another data point that suggests chip stocks are great, but they aren’t living up to the lofty expectations of growth that tech companies are used to.

In short, they are too expensive and investors want a cheaper multiple for chip stocks right here and now.

So be prepared for a little bit of a selloff in the immediate short term.

One of the best second-tier chip stocks and one of Apple's biggest customers gave us a glimpse into operations behind the scenes at one of Silicon Valley’s robust silicon makers.

Broadcom (AVGO) delivered a disappointing sales forecast, hurt by the parts of its business that aren’t tied to artificial intelligence.

The company projected sales of roughly $14 billion in the fourth quarter while they expect $12 billion of revenue from AI-related products for the full year, beating the average estimate of $11.8 billion.

The forecast showed that Broadcom’s non-AI operations are growing more slowly than anticipated. Though the company has benefited from a surge in artificial intelligence spending, not all of its wide-ranging divisions are significantly profiting.

The AI spending boom has turned Broadcom’s rival Nvidia (NVDA) into the richest, most valuable company in the industry. Nvidia sells so-called AI accelerators that help develop tools such as ChatGPT. Broadcom has benefited as well by supplying related components and software.

Datacenter providers rely on Broadcom’s custom-chip design and networking semiconductors to build their AI systems. The company also sells components for cars, smartphones, and internet access gear. Its push into software, meanwhile, includes products for mainframe computers, cybersecurity, and data center optimization.

Over the long term, the AVGOs CEO believes that the AI chip market will move to custom, in-house designs. That would mean shifting away from Nvidia components — a change that could benefit Broadcom since it helps customers produce their chips.

Apple is a top customer as well: Broadcom provides key components for the iPhone.

Chip stocks were hovering at an all-time high just a few weeks ago.

The scandal that spurred a selloff in chips was the accounting issues at SuperMicro.

The initial event opened up a can of worms and signaled to traders to take profits while conditions were still favorable.

Now chip stocks are telling traders that they cannot keep up with the high expectations and investors will need to taper back the whole idea that AI is about to overtake the world.

Even if AVGOs AI business is doing exceptionally well, they have a legacy business that is bringing up the rear and could be a drag on the overall business for years to come.

AVGO is still a stalwart in the chip business with interests in the right verticals and I do believe it is still a long-term buy especially considering they still haven’t successfully integrated VMware.

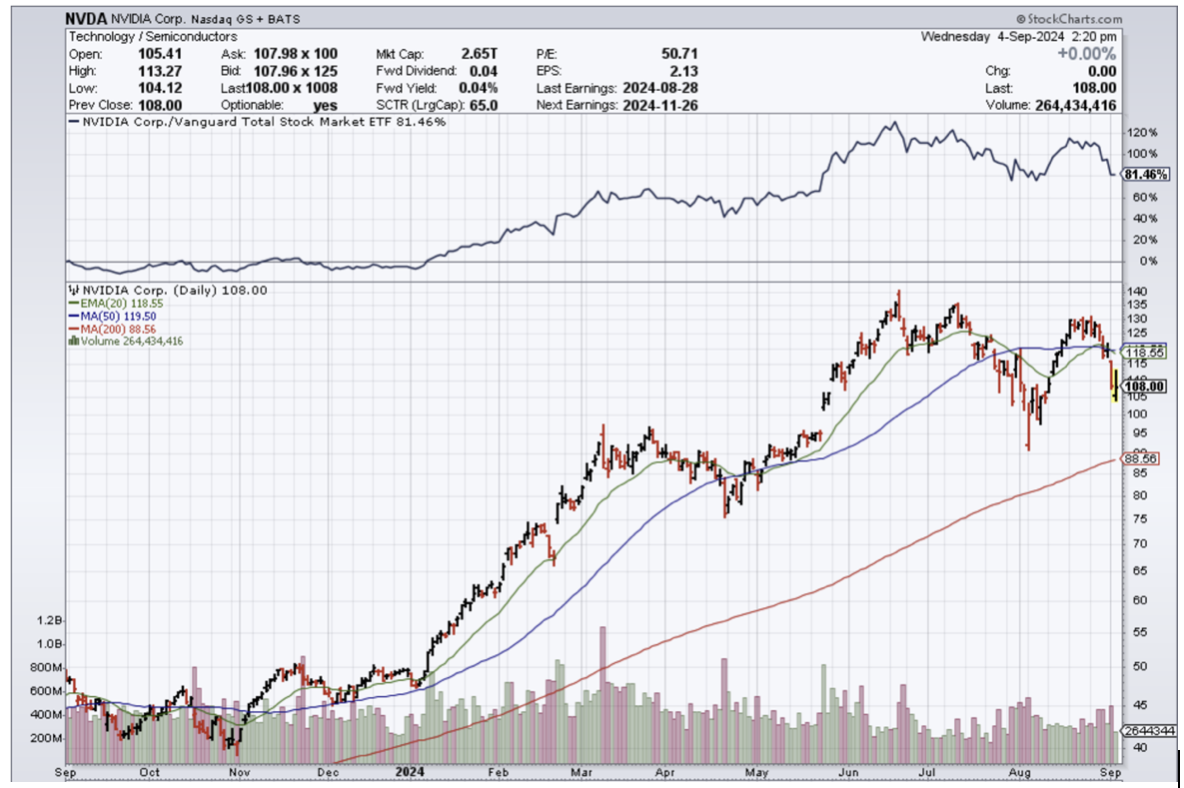

Mad Hedge Technology Letter

September 4, 2024

Fiat Lux

Featured Trade:

(FEDS KNOCK THE WIND OUT OF TECH)

(AI), (NVDA), (MSFT), (META)

The U.S. Federal government just took the air out of the tech market rally in the short term.

Good thing the market usually has a short memory.

Mr. Market did not expect the US Justice Department to barge in and subpoena Nvidia (NVDA).

Nvidia is the gem of the tech industry and the leader of the cutting-edge generative artificial intelligence sub-sector.

To take out Nvidia and destroy it, the tech market would be valued at significantly less than it is today.

Not to mention we are just 2 months away from the U.S. election, this sounds and feels like a bold political move behind the scenes.

Why not wait until after the election?

As it stands, the timing is pretty terrible for tech stocks as the amount of catalysts to take us to new highs has disappeared.

The past earnings seasons were nothing stellar and many tech companies sold off on poor forward guidance.

It is no joke that we have been waiting for over 4 years for the recession that still hasn’t come.

However, it seriously looks like we won’t be able to kick the can down the road anymore and the job market is starting to fall apart to the point where we will need rate cuts.

The DOJ believes Nvidia is too dominant and appears to look like a monopoly and the government is inching closer to filing a formal complaint.

Antitrust officials are concerned that Nvidia is making it harder to switch to other suppliers and penalizes buyers that don’t exclusively use its artificial intelligence chips.

Nvidia has drawn regulatory scrutiny since becoming the world’s most valuable chipmaker and a key beneficiary of the AI spending boom. Sales have been more than doubling each quarter.

Regulators also are digging into whether Nvidia gives preferential supply and pricing to customers who use its technology exclusively or buy its complete systems.

Nvidia Chief Executive Officer Jensen Huang said he prioritizes customers who can make use of his products in ready-to-go data centers as soon as he provides them, a policy designed to prevent stockpiling and speed up the broader adoption of AI.

Microsoft (MSFT) and Meta (META) spend more than 40% of their budget on hardware on the chipmaker’s gear. During the peak of shortages of Nvidia’s H100 accelerator, individual components were retailing for as much as $90,000 each.

There also are broader regulatory questions about Nvidia’s practices. Access to AI capabilities has become a key focus for governments around the world, with the technology becoming increasingly vital to economic strength and national security.

If NVDA shares drop to anything close to the $100 level, I do believe that is a great entry point to add to shares.

Much of the bad news has been priced in and at the end of the day, even if NVDA is broken up, it will happen 10 years later.

As for the larger tech story, September could be a weak month for tech stocks and it is a seasonably slow month.

However, the infrastructure build for AI data centers relentlessly continues, and from my channel checks, I see tech firms increasing their purchases of Nvidia AI chips.

This bodes well for the future and explains why sales keep doubling and doubling like it never ends.

“I've actually not read any books on time management.” – Said Elon Musk

Mad Hedge Technology Letter

August 30, 2024

Fiat Lux

Featured Trade:

(AI SQUEEZES OUT TECH WORK FORCE)

(AI), (NVDA)

Don’t be in denial about artificial intelligence.

The more you fight it – it will fight you back.

It is coming for us and you need to adjust your life accordingly.

That is largely the message I want to convey to readers because the existence of tech companies and how they function has never been changing at such warp speed until today.

Instead of getting all worked up about the hoopla of what it will bring like it is some shiny new Porsche in the garage, we need to get into the weeds to see how it will manifest itself inside the real world.

While the rest of the world still has no idea what artificial intelligence is, tech workers in the Philippines are already living and breathing the new reality every day for better or worse.

The spoiler here is that it is mostly bad for the local workforce in the beautiful island and sovereign nation of the Philippines but positive for the bottom line.

It’s not a shocker that foreign companies don’t like to pay high wages and will even skirt around the low-wage area if they have their way.

Until today, tech workers in the likes of Moldova, Montenegro, and the Philippines were irreplaceable because they represented good value for labor.

Now these workers are getting crushed by the dreaded AI substitute software.

All of the major players in its vast outsourcing industry, which is forecast to cross $38 billion in revenue this year, are rushing to roll out AI tools to stay competitive and defend their business models.

Over the past eight or nine months, most have introduced some form of AI “copilot.” These algorithms mainly work alongside human operators.

Avasant, an outsourcing advisory firm that works extensively in the Philippines, estimates that up to 300,000 business process outsourcing (BPO) jobs could be lost in the country to AI in the next five years.

In February, payments company Klarna Bank announced AI bots were conducting two-thirds of all customer service interactions, equaling the work of 700 full-time agents.

Readers cannot fall asleep at the wheel by downplaying this transition in the business model of tech companies.

This movement to bots has the potential to save many percentage points of expenses on labor.

I don’t know any CEO who is actively ignoring this hard pivot to software.

For every success story, there will also be failures because let's get this straight, not every CEO or COO knows how to implement and harness the powers of AI.

Not all managers are created equally.

I know it sounds cliché to look at big tech but they are the powerbrokers of the AI industry and unsurprisingly are the ones pouring the most capital into this new technology.

The end results are that only a handful of companies will secure the bounty of profits that AI will deliver.

There will be surprises on the way but Nvidia relaying to investors that the AI narrative is still here is just as important as management talking about how great AI is.

The only caveat I would say is that the honeymoon phase of AI is definitely coming to a close.

Now the real tough sledding starts ahead of us.

For the time being, pick up shares in Nvidia on this nice dip.

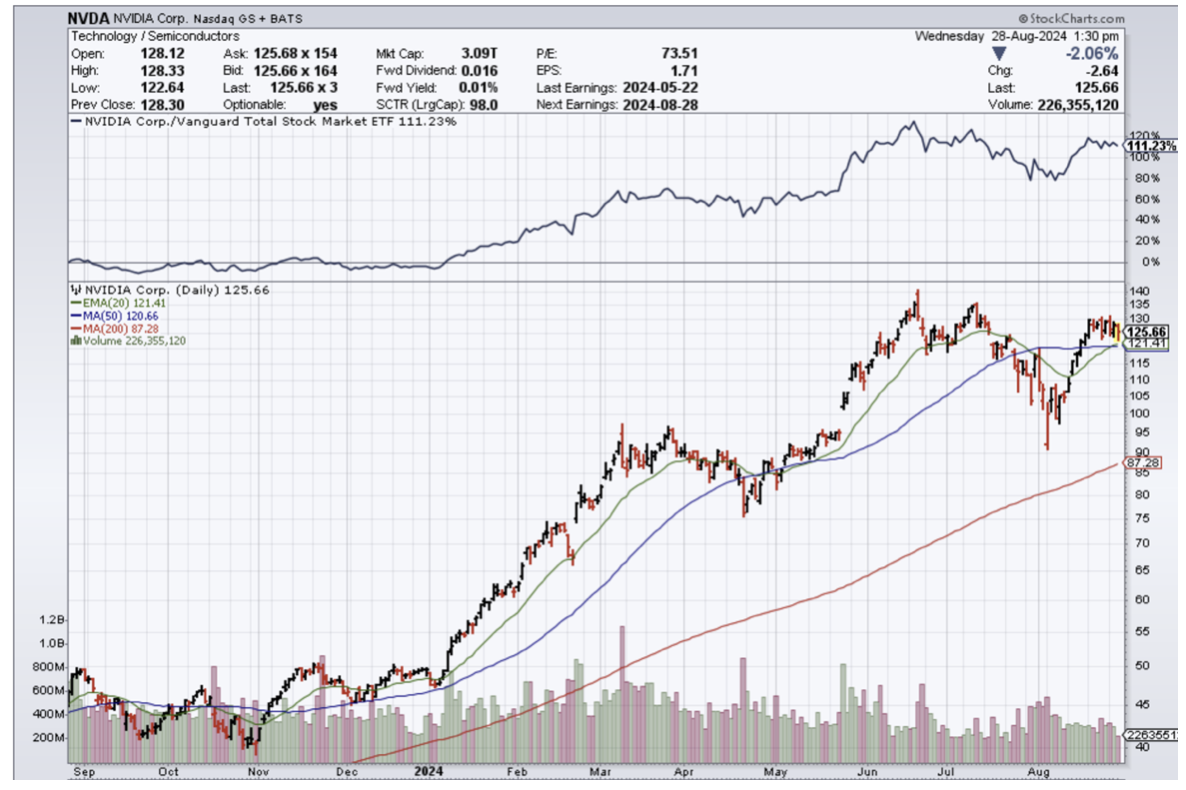

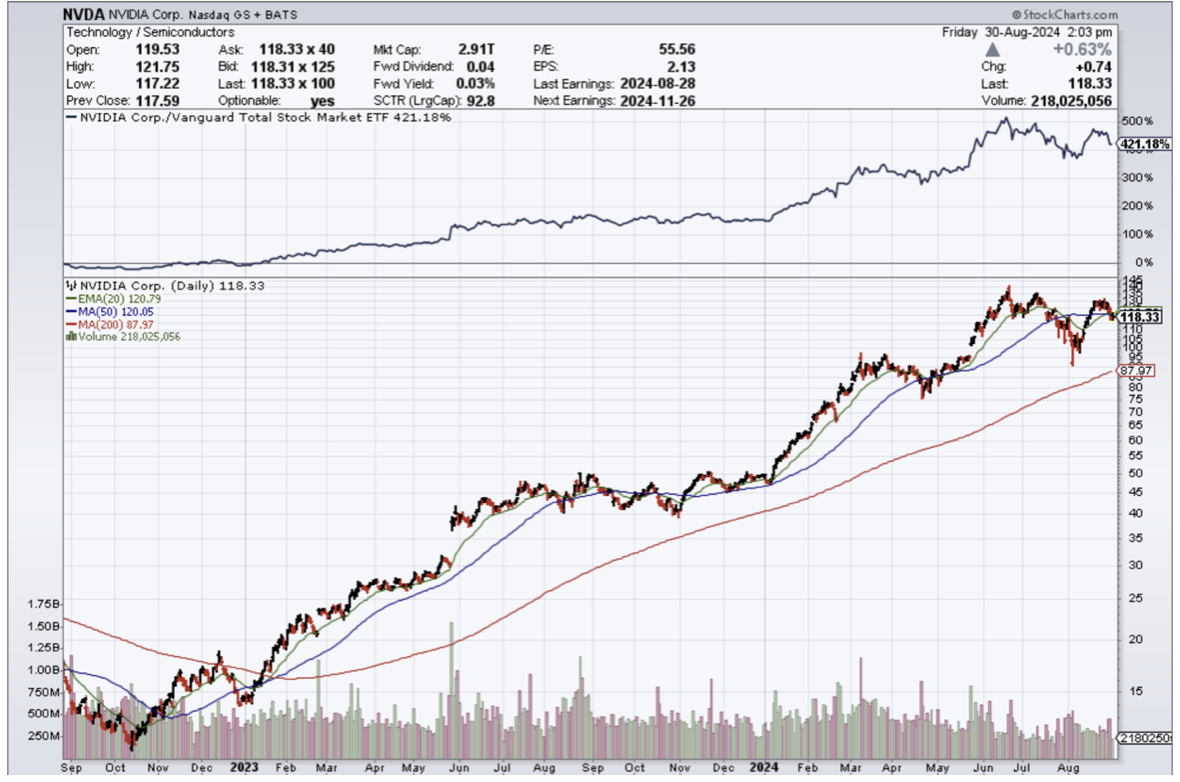

Mad Hedge Technology Letter

August 28, 2024

Fiat Lux

Featured Trade:

(NOT SUPER BY SUPER MICRO)

(SMCI), (NVDA)

This is the first blip in quite a while for the chip sector.

It has almost been perfect in the latest leg up in the tech market carried by heavy hitter Nvidia (NVDA).

I don’t think this will have a significant knock-on effect on the prospects of NVDA.

NVDA is an animal of its own and I do believe we will see great earnings and positive forward guidance that could mean the next gasp up in tech stocks.

Today represents the first black eye for the AI generative movement when short seller Hindenburg research accused Super Micro Computer (SMCI) of “account manipulation.”

There was a three-month investigation and many former insiders were contacted.

Hindenburg research has a pretty good track record calling out tech frauds.

Most of their calls focus on public stocks helmed by predominately Chinese nationals.

SMCI stock crashed 25% on the day, and it is an ominous setup going into Nvidia earnings later today.

Hindenburg said it reviewed various instances that suggested there were ongoing bookkeeping issues within the $35 billion tech firm even after the SEC charged it with "widespread accounting violations" in 2020.

Workers within the company said they faced pressure to meet high sales quotas, even after the company was charged by regulators.

The high quotas incentivized some workers to ship defective products.

Some of Super Micro's partners appeared to do little business outside their relationship with Super Micro. Ablecom, one such partner, exported 99.8% of its product in the US to Super Micro, while Compuware, another partner, exported 99.7% of its product to Super Micro.

Hindenburg also said Super Micro also ramped up exports to Russia after Moscow invaded Ukraine, which violated US sanctions.

Hindenburg highlighted quality concerns among Super Micro's customers, some of whom have turned to alternative suppliers. Tesla and CoreWeave, two of Super Micro's major customers, have inked high-profile deals with Dell over the past year because they found SMCIs products inferior.

The tsunami of bad news for SMCI means it is time to avoid the stock.

The company faces a torrent of accounting, governance, and compliance issues and offers an inferior product and service now being eroded away by more impactful competition.

The accusations are quite structural and investors won’t be able to just turn a blind eye to all of this.

SMCI delayed reporting their earnings at the last second which tells an investor audience that much of the accusation has some truth to it.

There is a lot to solve internally and I don’t think investors should swoop in and buy the dip just yet.

If there is a bounce, it most likely will be a dead cat bounce.

Although not an existential problem, this short seller report will set back SMCI 5 years and that is a long time in the world of tech.

Readers should avoid this chip stock and head to higher ground.

There is a possibility that this is just the tip of the iceberg and the core could find out to be a lot more rotten than first thought.

Readers will be better off sticking with the likes of Nvidia, Broadcom, AMD, and Micron.