“The superior man understands what is right; the inferior man understands what will sell.” – Said Chinese Philosopher Confucius

“The superior man understands what is right; the inferior man understands what will sell.” – Said Chinese Philosopher Confucius

Mad Hedge Technology Letter

August 16, 2024

Fiat Lux

Featured Trade:

(BIG RISKS TO TECH DISSIPATE)

($COMPQ), ($TNX), (FXY)

I don’t believe the tech sector is toast and it isn’t true to say that the burnt crust is the only part left over.

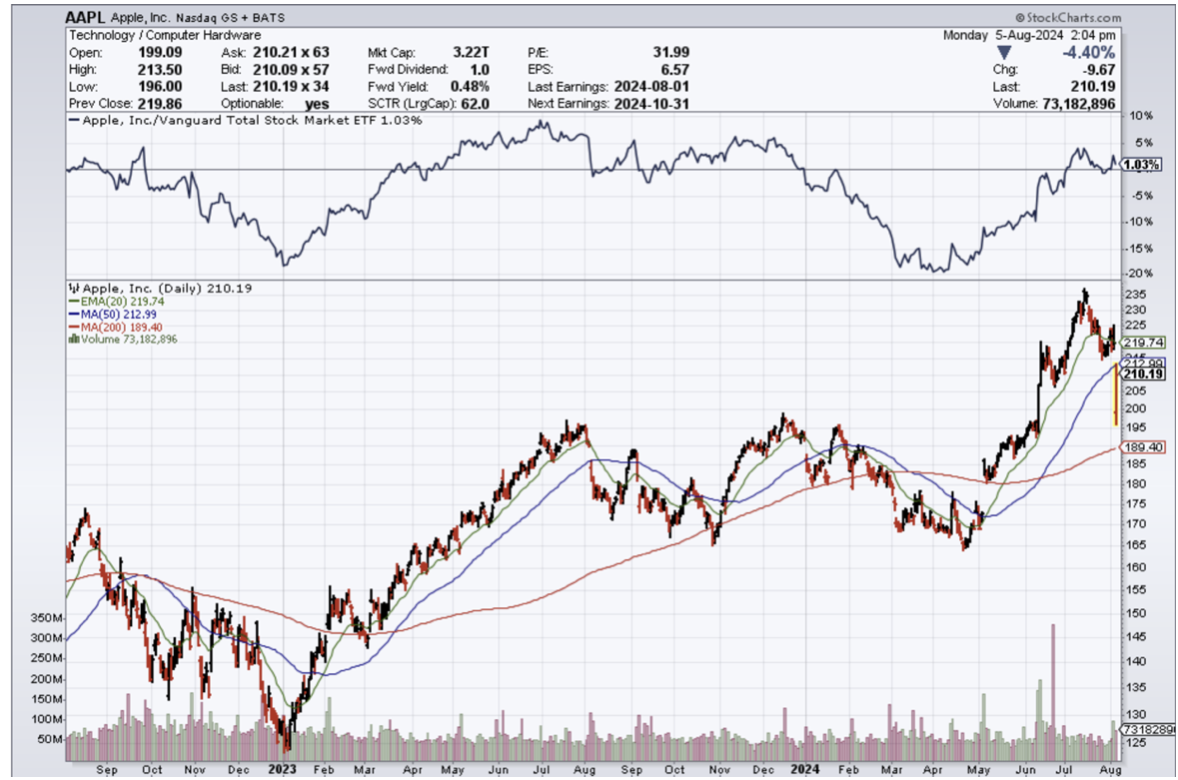

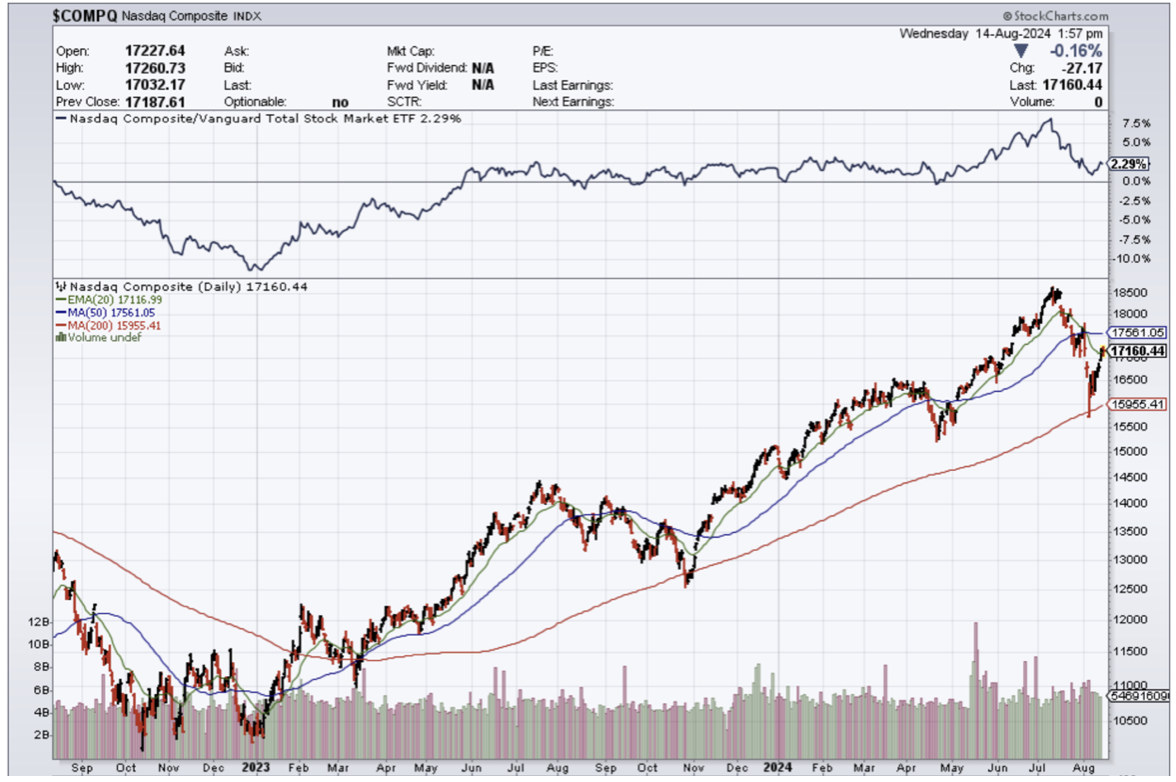

There is still vitality in it at the core of the tech sector ($COMPQ).

Granted, the trajectory left isn’t enough to propel tech stocks to a meteoric rise, but tech stocks should perform quite robustly in the run-up to the next earnings report.

So for all that are waiting for the bubble to burst – wait a little longer my friends.

In the meantime, let’s take a quick barometer of some of the outsized risks to big tech and ponder about the idea that outside or indirect events could possibly takedown tech shares.

China bailed the world out of the last three recessions and now they are a risk to drag down the rest of the world.

In each case, China's high growth and massive issuance of stimulus kick-started global expansion, and now that is gone with the wind.

China's model of economic development which worked so brilliantly in the boost phase, is now out of potency.

If American tech shares are sideswiped by global contagion, don’t bet on China to come bail out the radical overlords of Silicon Valley. China has its own problems and is entirely focused on that.

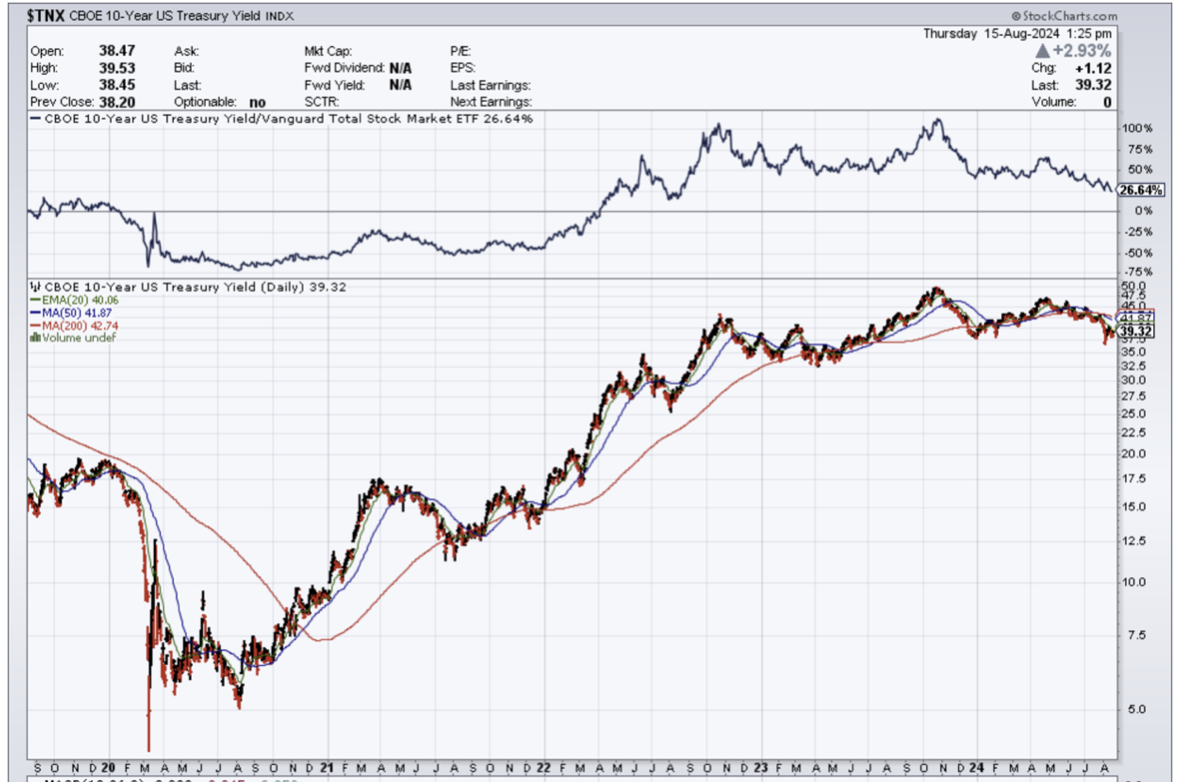

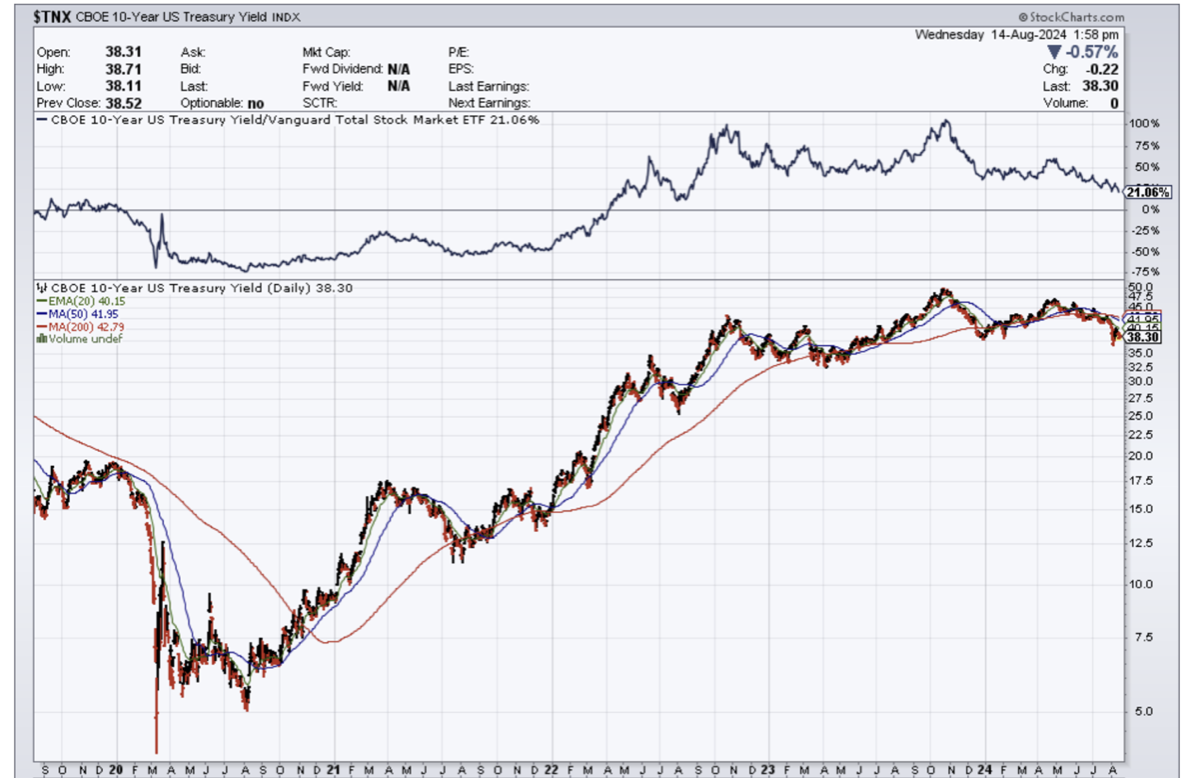

The era of zero-interest rates and unlimited government borrowing has ended. As Japan has shown, even at insane low rates ($TNX) of 1%, interest payments on skyrocketing government debt eventually consume virtually all tax revenues.

Japan was the black swan that could have cratered the tech market. Instead, it was a mild selloff yet manageable selloff creating a beautiful entry point for most of tech stocks.

Money is coming off the sideline to join in on a sharp rally into the U.S. presidential election so in the end the Japanese currency (FXY) risk was basically much-a-do-about-nothing.

At the start of the cycle, global debt levels (government and private sector) were low. Now they are high. The boost phase of debt expansion and debt-funded spending is over, and we're in the stagnation-decline phase where adding debt generates diminishing returns.

The era of low inflation has also ended for multiple reasons, but the tech shares have proven they can unequivocally march higher in an era of high inflation.

This is ironically due to tech being better positioned than other industries on a relative basis, because of their strong moats and iron-clad balance sheets.

The resilience in tech also echoes the idea that every company has become a tech company by integrating its products and revenue streams into daily business operations.

Tech productivity boom is hardly a one-off so as readers fret, please don’t think shares will magically drop to zero.

Dips are being bought and prices will go higher in the short term.

Economists were in awe in the early 1990s by the productivity stemming from the tremendous investments made in personal and corporate computers, a boom launched in the mid-1980s with Apple's (AAPL) Macintosh and desktop publishing, and Microsoft's Mac-clone Windows operating system.

By the mid-1990s, productivity continued to rise and the emergence of the Internet triggered the adoption of most of the population to get online and do business.

All the doomsday prophets who said high debt and high interest rates were the cocktails to finally stop tech stocks in their tracks got it completely wrong.

I am not saying debt and high interest rates are positive for equities, but tech has been able to skillfully navigate the headwinds with their excellent management skills and pivot towards leanness.

The buzz around AI holds still has a lot to prove, but the market is still celebrating its deflection of the Japanese yen carry trade.

I am not saying that tech shares will never have to confront anything that can drag them down meaningfully, but many of the high risks have either been postponed or dealt with.

We are in a position where tech should steamroll into the end of the year barring some type of crazy event.

“Life's tragedy is that we get old too soon and wise too late.” – Said Benjamin Franklin

Mad Hedge Technology Letter

August 14, 2024

Fiat Lux

Featured Trade:

(POSITIVE SIGNAL FOR THE TECH RALLY)

($COMPQ), ($TNX)

We received highly bullish news from the fiscal policy side today.

Conditions are everything in the short-term which is why macro events sometimes steal the whole show by destroying or propping up market sentiment.

Scare events can shock investors and become the impetus to take profits to protect capital.

Fortunately, the data from the CPI index has most likely given the green light for the US Central Bank to officially initiate its easing cycle next month.

My guess is that Fed Governor Jerome Powell cuts by 25 basis points and it could turn out to be a hawkish cut.

This is massively bullish for tech stocks ($COMPQ) leading up to the next earnings report in October.

This sets the backdrop for tech stocks to motor towards the upper left in upcoming months.

Lower rates ($TNX) translate into lower costs of capital for tech stocks to borrow money for paying stuff like salaries, software, and hardware.

The high-rate environment has translated into a dearth of companies going public and has stifled the creative juices at the formative stages of Silicon Valley.

That last jobs report offered new signs of a cooling labor market, which stoked fears that the Fed may have waited too long to start lowering interest rates after keeping them at a 23-year high for the last year.

A milder inflation reading released Wednesday removes one of the last hurdles the Federal Reserve needed to clear before cutting rates in September.

The Consumer Price Index (CPI) increased 2.9% over the prior year in July, down from June's 3% annual gain in prices. On a "core" basis, which strips out the more volatile costs of food and gas, prices in July climbed 3.2% over last year — down from 3.3% in June. That was the smallest increase since April 2021.

The new numbers are the latest confirmation that inflation is in fact dropping off a cliff after heating back up during the first quarter of the year, a development that prompted the Fed to warn at one point that rates would likely stay higher for longer.

Fed Chair Jerome Powell made it clear at the end of last month that a cut in September was “on the table” as long as the data supported it. He and other policymakers have said they want to be sure that inflation is in fact moving “sustainably” down to their 2% goal.

Tech stocks have positively correlated with interest yields since 2020, which is counterintuitive.

What this really means is that the growth rate of tech has overpowered the 5% Fed Funds rate which is quite impressive.

That high rate was supposed to pummel tech stocks and that fear-mongering failed to materialize.

No doubt the AI boom delivered a helping hand to tech shares as well.

Tech stocks were one of the few sectors in the public market that remained attractive in the face of aggressive rate hikes.

With the Fed almost to the point of reversing hawkish policy, I do believe it is “all systems go” for tech stocks in the short-term and this removes yet another possible black swan event off the table.

I am bullish on tech shares in the short-term.

“I believe you have to be willing to be misunderstood if you're going to innovate.” – Said Founder of Amazon Jeff Bezos

Mad Hedge Technology Letter

August 12, 2024

Fiat Lux

Featured Trade:

(UNLOCKING THE FUTURE OF TECH)

(TSLA), (NVDA), (AMZN)

Unshackling the restraints on human labor – that is where tech is headed.

I’m talking about AI.

Robots aren’t able to perform complicated tasks and that is the holy grail of AI.

If headway is made just on this one issue then the sky is the limit.

Profits are then unlimited and the world will change into something we could have never imagined.

If stakes weren’t high enough, the next explosive leg up in tech shares is now centered on this concept.

There is only so much balance sheet maneuvering can add to the bottom line.

Magnificent 7 stocks who are experts are juicing up the balance sheet will gradually run out of levers to pull.

Technology stocks demand that management move the needle along because the alternative is that the company will get left behind.

When the Department of Defense commenced its robotics challenge in 2015, the stated goal was to develop ground robots that can aid in disaster recovery with the help of human operators.

Nearly a decade later, generative AI is accelerating that learning curve, pushing human-like machines to pick up new tasks in real-time.

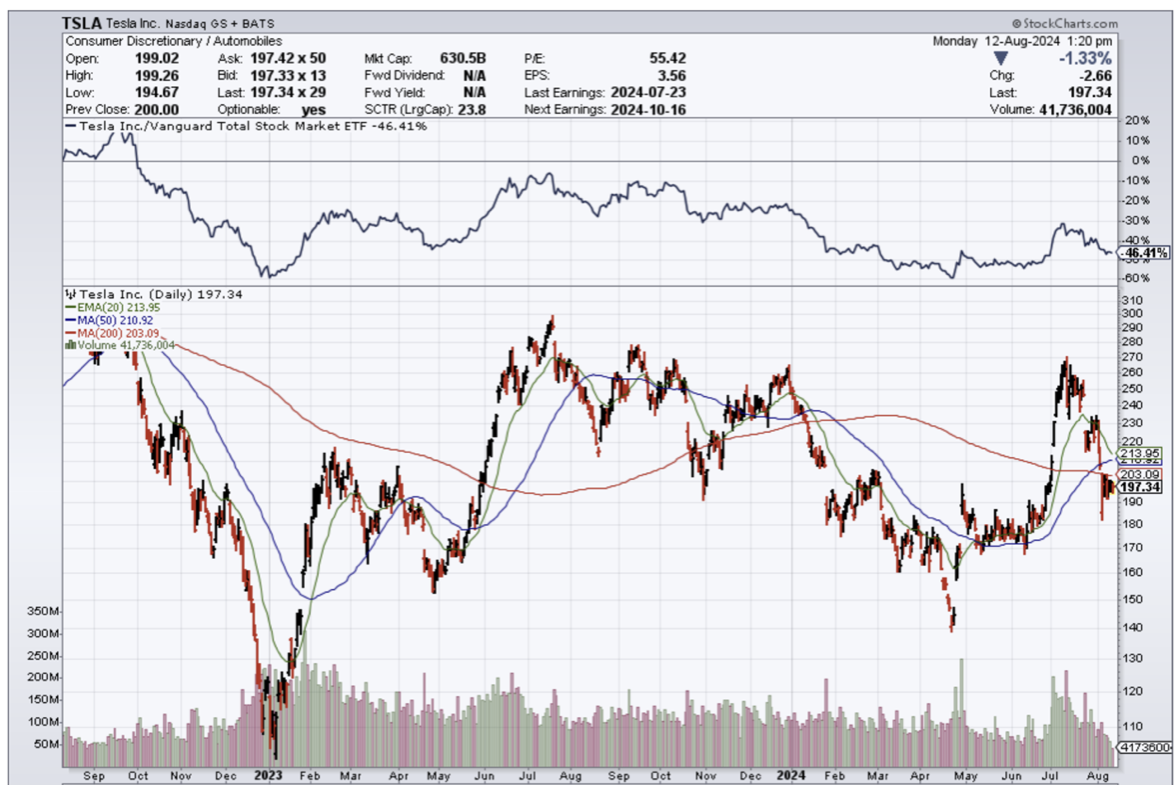

And in June, Tesla (TSLA) presented an updated version of its Optimus robot at Tesla’s Investor Day and showed it roaming a factory floor. CEO Elon Musk touted the robot’s potential, saying it had the ability to push the company’s market cap to $25 trillion.

Humanoids that can adapt to existing environments have long been seen as the ultimate test if they can work alongside humans in spaces built for them.

Nvidia (NVDA) is driving rapid development through an ecosystem built specifically for humanoids. It combines high-powered chips that process data at high speeds with a digital world that allows users to train robots on skills applied in the real world.

Just last month, Nvidia unveiled “NIM Microservices,” a visual training ground that allows generative AI models to visually interpret their surroundings in 3D.

Nvidia’s ecosystem now enables robots to train using text and speech input, in addition to live demonstrations.

Humanoids have already begun taking their first steps into reality. Musk has said two Optimus robots are working at Tesla’s Fremont factory, and he expects a few thousand to be deployed by next year. Amazon (AMZN) has partnered with Oregon-based Agility to utilize its Digit robot at a test facility. Apptronik is working with Mercedes-Benz to integrate Apollo into its manufacturing line.

The goal is to adapt humanoid for the future which will allow them to operate beyond industrial use. They could become as ubiquitous if companies are able to scale and bring costs down to $10,000 per machine.

Technology is still in the stage of calculating how they bring the expenses under control.

It is not very cost-effective if a company needs to spend 5 times the actual cost of running the AI division on retrofitting the environment for a humanoid and resetting the language models for different tasks.

Much of these technical aspects are being worked out, and these companies are inching their way closer to a day when companies might be able to work fully without a human worker or alongside a minimum amount of workers.

Tesla is a company long-term that needs to be looked at and this assumption is solely based on their robotics and humanoid business. It is highly plausible that Elon Musk is at peace with sacrificing his EV business in the medium time as long as moving up the value chain to become the leader of what is next which is looking more like robotics using AI.

Musk is skating to where the puck is next and that is where the future will be.

Mad Hedge Technology Letter

August 9, 2024

Fiat Lux

Featured Trade:

(WARNING SIGNS LITTER THE TECH NARRATIVE)

(ABNB), (BKNG), (EXPE)