Mad Hedge Technology Letter

June 24, 2024

Fiat Lux

Featured Trade:

(E-COMMERCE PARTNERSHIPS WILL THRIVE)

(TGT), (SHOP), (WMT)

Mad Hedge Technology Letter

June 24, 2024

Fiat Lux

Featured Trade:

(E-COMMERCE PARTNERSHIPS WILL THRIVE)

(TGT), (SHOP), (WMT)

Target (TGT) is partnering with e-commerce specialist Shopify (SHOP) to expand its marketplace for third-party merchants.

This is a big deal so don’t diminish this news.

I honestly applaud this maneuver by Target, because it adds e-commerce footprint without paying a premium for it.

Everyone knows that everything is a total rip-off these days like adding an incremental addressable audience at a tech company.

Target has a lot to do to catch up with Amazon, but that’s the direction they should be headed in.

In the future, there is a highly likelihood that TGTs digital business will determine whether they succeed or fail as a tech company.

Everyone is going digital now. Adapt or die.

Shopify is a powerful back-end ecommerce foundation and integrating that with Target appears as a win-win decision moving forward.

We only need to look at competitor Walmart (WMT) which presides over a booming e-commerce business.

That is by decision as they launched a digital-first strategy and have made serious inroads into picking up e-commerce market share.

This partnership also on boards Target into a whole load of new products that they could only dream of selling and the process was rather painful.

Target Plus operates on an invite-only basis for merchants and currently offers more than 2 million items through more than 1,200 sellers.

Online marketplaces can also be launch pads for profitable advertising businesses, with merchants paying for prominent placement in front of shoppers.

Target more than doubled the number of sellers and products on its marketplace over the past year.

The company plans to maintain its invite-only model and continue vetting sellers on the platform.

Curating the selection — for example, allowing only one vendor to offer any given item — is a strategy that will let Target stand out.

Target’s partner, Shopify, makes software that helps vendors quickly set up online stores and process payments.

The company says it works with millions of merchants in about 175 countries. Globally, shoppers will spend $282 billion this year on stores managed with Shopify software. That’s more than double Target’s projected sales for the year.

We are at the late stage of the tech cycle that has been long in the tooth.

It’s not a shocker at this point for tech models to be petering out and management looking for that extra juice to kick-start revenue growth for however long the rest of the business cycle lasts.

Clearly, debt financing isn’t an option these days and I do believe this is a time when management showed their worth as conditions have been extraordinarily tight for the last 2 years.

There is also no guarantee that business conditions will reverse and go back into that pre-pandemic goldilocks phase.

The jury is still out but higher interest rates could be in the mix for the foreseeable future.

Therefore, it is clever by TGT and SHOP to strike up a partnership in which TGT expands their offerings and SHOP merchants get a crack at a new audience.

These opportunities are limited in fashion, but tech in 2024 isn’t about an unlimited addressable audience.

Tech in 2024 is more about efficiency and staying lean because the past 2 years have really been about cutting the bloat.

Target obviously has the more upside in this relationship and I expect them to add other partners that can move the needle.

TGTs share price has been flat for the past 6 months and migrating further into a digital strategy could be the formula to nudge that share price back into high gear.

The stock price is now at $150 per share and I do believe TGT has the chance to grind higher closer to $200 per share by year-end.

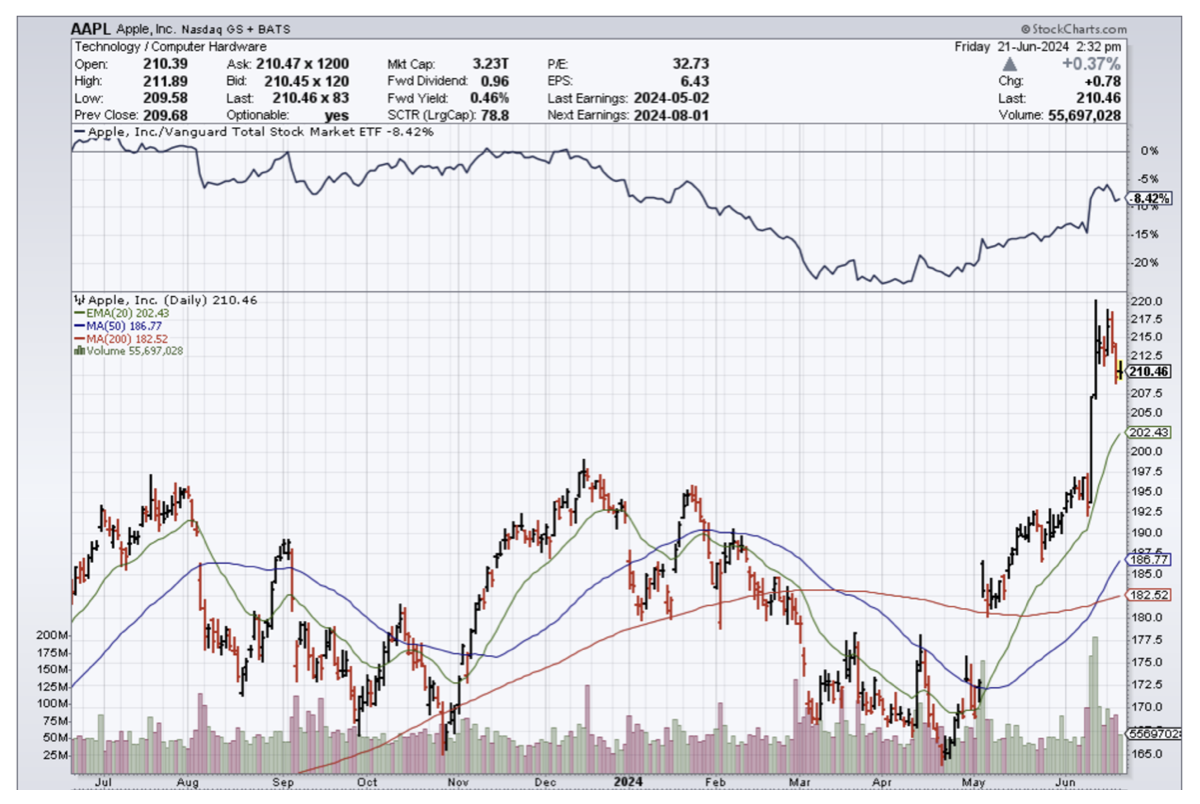

Mad Hedge Technology Letter

June 21, 2024

Fiat Lux

Featured Trade:

(CUPERTINO NEEDS A REBOOT)

(AAPL), (PYPL), (SQ)

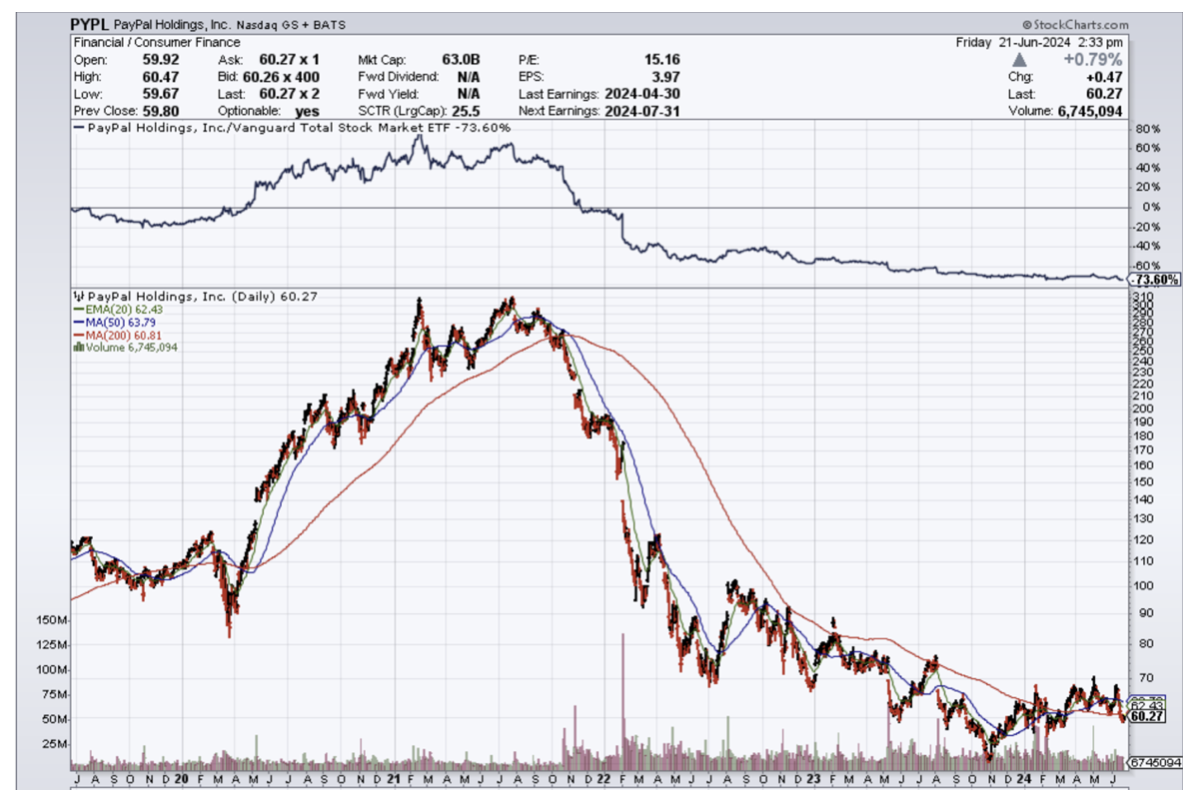

Fintech used to be the shiny new car and in the last year or two, the sub-sector has entirely reversed.

Look at stock like PayPal (PYPL) or Square (SQ), their market cap is only 20% of what it was in 2021.

The fintech hype didn’t match the results and it definitely wouldn’t be something that Steve Jobs would be interested in getting into.

Getting into the weeds a little, the fintech industry has been saturated.

Too many vendors chasing after the same customers with the same homogenous products doesn’t seem like something Apple is usually associated with.

Almost as if the behavior suggests a mea culpa, Apple officially stopped issuing loans through Apple Pay Later, its buy-now-pay-later program that launched last year.

The move comes after Apple said it would start allowing installment loans later this year in its Apple Pay checkout process through third-party companies, such as Affirm, and credit and debit cards from issuers, such as Citigroup.

This Apple product certainly would have turned into a buy now – pay never platform.

I won’t say that Apple should stay in their lane – they certainly shouldn’t.

The reason is that they are a one-trick pony hoping to pivot into another lucrative cash cow business like the iPhone business. They desperately need to become a two-trick pony but they can’t find that special sauce yet.

Apple also recently announced they are putting their Apple Vision VR goggles on the backburner.

It is sad to see Apple go from project to project with such little follow-through.

They are Apple and many still think that brand still carries a lot of weight.

In the short term, they will get a pass for contracting some terrible projects, but only for so long.

One could argue that wearables like the Apple Watch and the iPad have been somewhat successful and I do acknowledge they have had some stickiness in terms of revenue.

However, the already saturated fintech payments business is a head-scratcher.

Sometimes it’s best to let fintech be fintech and allow them to experience the race to zero.

Apple is bigger and better – their customers deserve something that delivers higher value.

Clearly, the management at Apple at the highest levels is lacking the creative juices to push through something trendsetting or cutting edge and now that is starting to become a serious threat to future cash flows.

The OpenAI partnership was a copycat move and I am not sure if they have really planned how they will seemingly integrate this new tool into their products.

Remember, OpenAI could destroy some of Apple’s products because AI is still rife with errors and can even cause major losses to the share price.

What if the CEO of Apple Tim Cook wakes up one day and AI has deleted half of Apple’s internal software or emailed all of Apple’s intellectual property to a fierce rival?

What if AI magically wires $100 billion of Apple’s war chest to a 3rd world bank under the banner of improving world hunger or balancing income inequality?

Remember that AI has no common sense and that could be very dangerous.

Kids who grew up in front of computers all day are also notorious for having little common sense and the end of the day results show.

Nobody knows what will happen, but Apple sure appears defensive and that is always big trouble in Silicon Valley in an industry where you need to know what will happen in the future.

“Greatness does not come from intelligence. Greatness comes from character, and character isn't formed out of smart people: it's formed out of people who have suffered.” – Said Nvidia CEO Jensen Huang

Mad Hedge Technology Letter

June 17, 2024

Fiat Lux

Featured Trade:

(INNOVATION IS THE SAVIOR)

(TTDKY), ($COMPOQ)

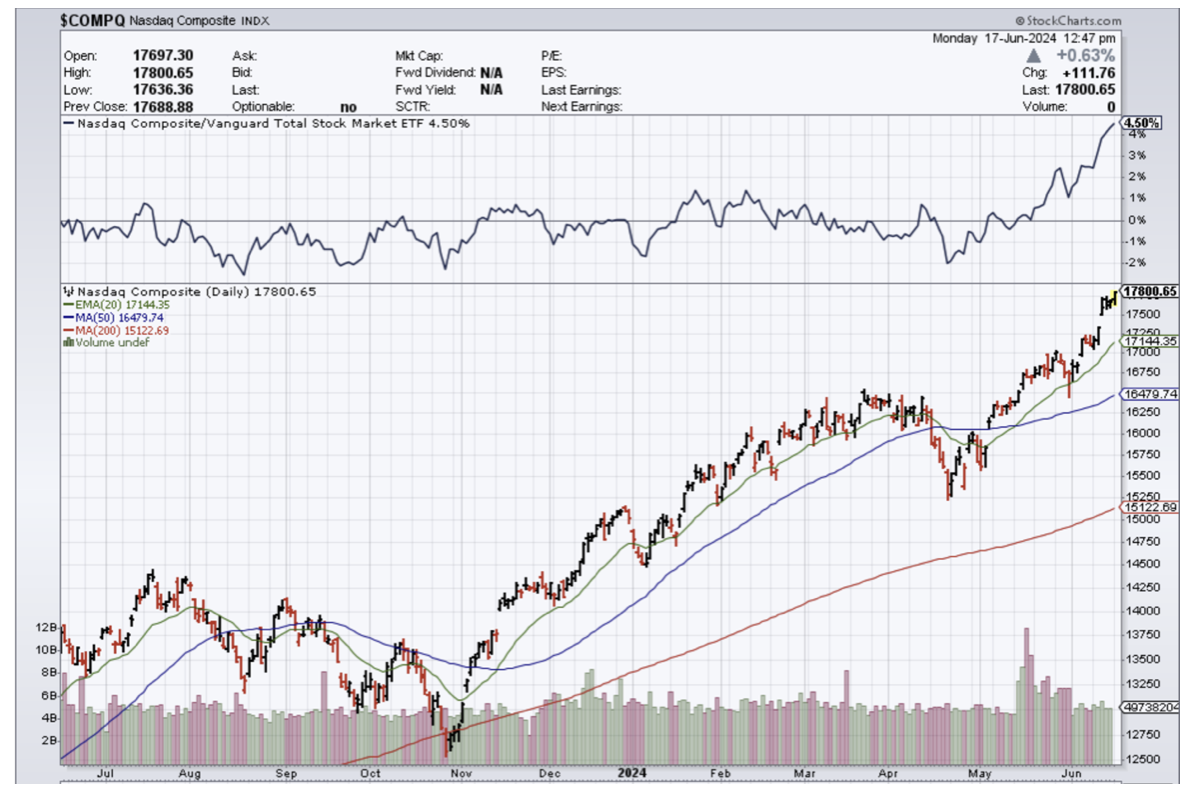

The only way out of the mountain of US Federal debt black hole is to innovate out of it via the tech sector ($COMPQ).

That is the only way.

A savior can only come in one form and that is it.

Nothing will forgive these trillions of debt and the pile is growing by the day.

The close to $35 trillion and counting will increasingly be a pain in the side of US businesses and that includes tech companies listed on the stock exchange.

Innovation leads to surging productivity manifesting in revenue gains that make it possible to dig ourselves out of this situation where interest expense drags us further down the rabbit hole.

Innovation has happened before to the US economy in the past like the gas-powered car and the creation of the internet.

It’s likely to happen again as well.

Instead of one big idea, it could come in the form of many solid yet meaningful gains.

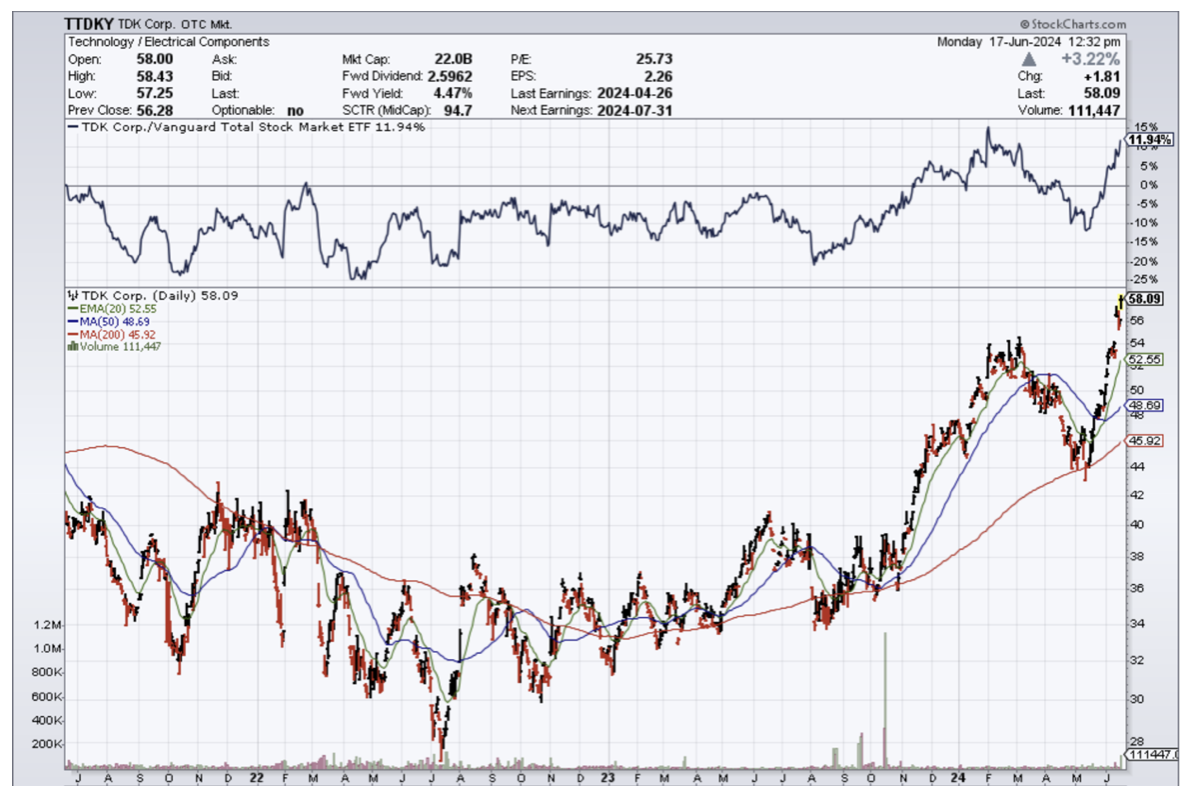

One just came in that could truly improve the productivity of American tech and that is from Japan’s TDK (TTDKY) which boasted a breakthrough in materials used in its small solid-state batteries.

The batteries set to be produced will be made of an all-ceramic material, with oxide-based solid electrolyte and lithium alloy anodes.

The high capability of the battery to store electrical charge, TDK said, would allow for smaller device sizes and longer operating times, while the oxide offered a high degree of stability and thus safety.

The breakthrough is the latest step forward for a technology industry experts think can revolutionize energy storage, but which faces significant obstacles on the path to mass production, particularly at larger battery sizes.

Solid-state batteries are safer, lighter, and potentially cheaper and offer longer performance and faster charging than current batteries relying on liquid electrolytes. Breakthroughs in consumer electronics have filtered through to electric vehicles, although the dominant battery chemistries for the two categories now differ substantially.

The most significant use case for solid-state batteries could be in electric cars by enabling greater driving range.

TDK, which was founded in 1935 and became a household name as a top cassette tape brand in the 1960s and 1970s, has lengthy experience in battery materials and technology.

The US federal debt is annualizing at a loss of $2 trillion at a time of full employment.

Imagine the devastation if we need to do quantitative easing again while already burning $2 trillion per year.

The number needed to pull us out of a recession could be $8-$15 trillion and that will come with a nasty set of inflationary outbursts.

The number of full-time jobs has fallen off a cliff and tech firms have cut the bloat.

It will be the ingenuity of tech companies like Japan’s TDK that will infuse the US economy will much-needed productivity.

I believe if the tech sector can keep peppering us with these breakthroughs in productivity, progress can supersede the out-of-control fiscal spending that has launched an uncontrollable bout of inflation in the US.

Remember that the top tech stocks in the world have been shielded from inflation only because they have hopped on the generative AI train.

For the rest of tech, inflation is hitting them like a sledgehammer between the eyes.

The biggest beneficiaries of cutting-edge innovation would be the share prices of the best tech stocks.

As it stands, tech will keep grinding higher in the current conditions, but better-than-expected innovation would shoot tech stocks to the moon and include a wide breadth of participation while putting a cap on inflation.

“Recession is when a neighbor loses his job. Depression is when you lose yours.” – Said Former US President Ronald Reagan

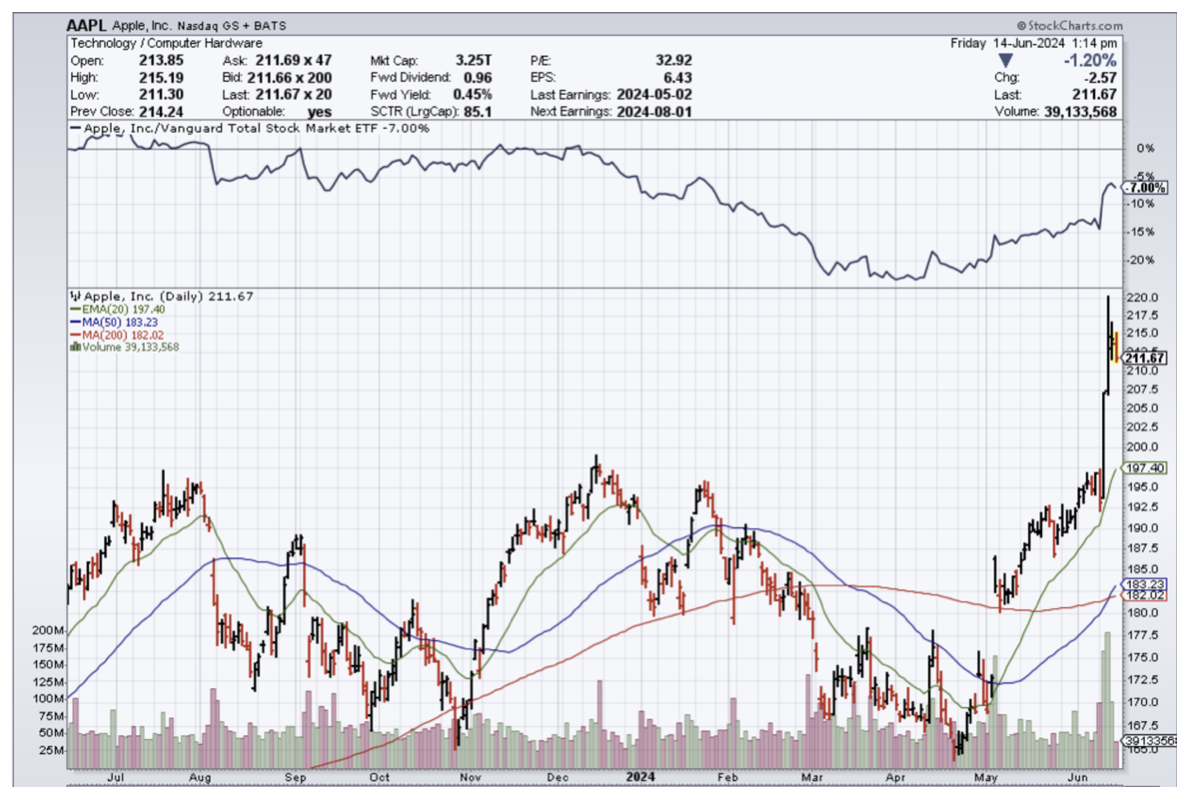

Mad Hedge Technology Letter

June 14, 2024

Fiat Lux

Featured Trade:

(ON BOARD THE AI TRAIN TO UNCERTAINTY)

(AAPL), (MSFT)

Apple (AAPL) has been on a one-way street to nowhere lately with their China business falling into the backstreet dumpster.

They had to do something before desperation took hold in the Cupertino headquarters.

It’s not like they could turn to Steve Jobs to figure this all out.

Tim Cook is an operations manager masquerading as the CEO and has little vision if any.

Announcing something AI was not a shocker as even legacy firms like Oracle and Dell had done the same with great success. But this isn’t data center stuff, the AI here will affect the Apple iPhone software.

Out the window goes privacy on your little iPhones – do people still even care about that?

Privacy was handed over to Sam Altman’s OpenAI.

Doing a deal like this opens up Pandora’s box and ensures that the Apple of the future will look a lot different than the one today.

Not everyone will like it, but that is tough. It is business.

The CEO of Apple, Tim Cook announced an unexpected and deep cooperation with the company OpenAI, which develops the chatbot ChatGPT, and the biggest loser has to be Microsoft.

MSFT usually doesn’t lose at its own game so this one is a bit of a surprise.

Apple has so far only flirted with the idea of its integration. The company surprised and took many people's breath away.

It is a paradox that the biggest investor in OpenAI is its rival Microsoft. The cooperation agreement took place behind closed doors to the dismay of Microsoft CEO Satya Nadella.

Thanks to artificial intelligence, Siri will be able to access all data stored in the user's phone and cloud through a secure channel.

Siri will no longer have a problem understanding the wider context of your question, connecting the answer with previous questions, or deciphering what you wanted to say if you accidentally mixed up the words.

CEO of OpenAI Altman now has fulfilled a longtime dream by striking a deal with Apple to use OpenAI’s conversational artificial intelligence in its products.

MSFT thought it had a big lead in AI over its peers and apparently, OpenAI, being the newest hottest thing in tech, has decided to sleep with everyone in bed instead of just picking one. MSFT has a right to be angry when they handed over $13 billion to OpenAI and that perceived lead in AI has evaporated.

It will be quite funny to see the software and the algorithms in these firms slowly merge into one product backed by the same AI company.

It screams of too many mouths to feed with just one nipple.

OpenAI has taken full advantage to entrench itself as the preeminent force at the forefront of technological modernity. They are the biggest winner here.

Right away, I wouldn’t say that Apple hit a home run even though the price action in their share price suggests so.

They are simply just boarding a train to uncertainty with the rest of big tech, and this maneuver looks highly defensive in nature.

Since Apple has stated they committing no money to the deal then it has to be coined as a win. It's $13 billion less spent and at a risk the software could turn clunky and unusable.

At that point, they could just terminate the relationship. This move was highly controversial inside of Apple headquarters, but management thought it was worth the risk.

Apple stock has most likely reached a short-term peak.

Lastly, I found it interesting that the Former head of the National Security Agency, retired Gen. Paul Nakasone has joined OpenAI which could mean that OpenAI will also be integrated into the Armed Forces. Apple won’t have much of a say in OpenAI going forward so we will see how it pans out.