Mad Hedge Technology Letter

June 5, 2024

Fiat Lux

Featured Trade:

(A HIGH RISK STRATEGY)

(NVDA), (AAPL)

Mad Hedge Technology Letter

June 5, 2024

Fiat Lux

Featured Trade:

(A HIGH RISK STRATEGY)

(NVDA), (AAPL)

“Heavy losses” is something that any investor would not want to hear but over time, it has become synonymous with short sellers.

Tech stocks are unusually volatile so it has been fashionable in the past to start a fund proclaiming that great performance can be secured by finding the most likely tech stocks to drop.

It’s like shooting fish in a barrel? Right?

Not even close.

In reality, it is hard to predict a big drop and identify the perfect timing in which tech stocks will blow up.

Even if a short seller guesses right, the timing could be off by years and to hold a position forever eats at the profitability.

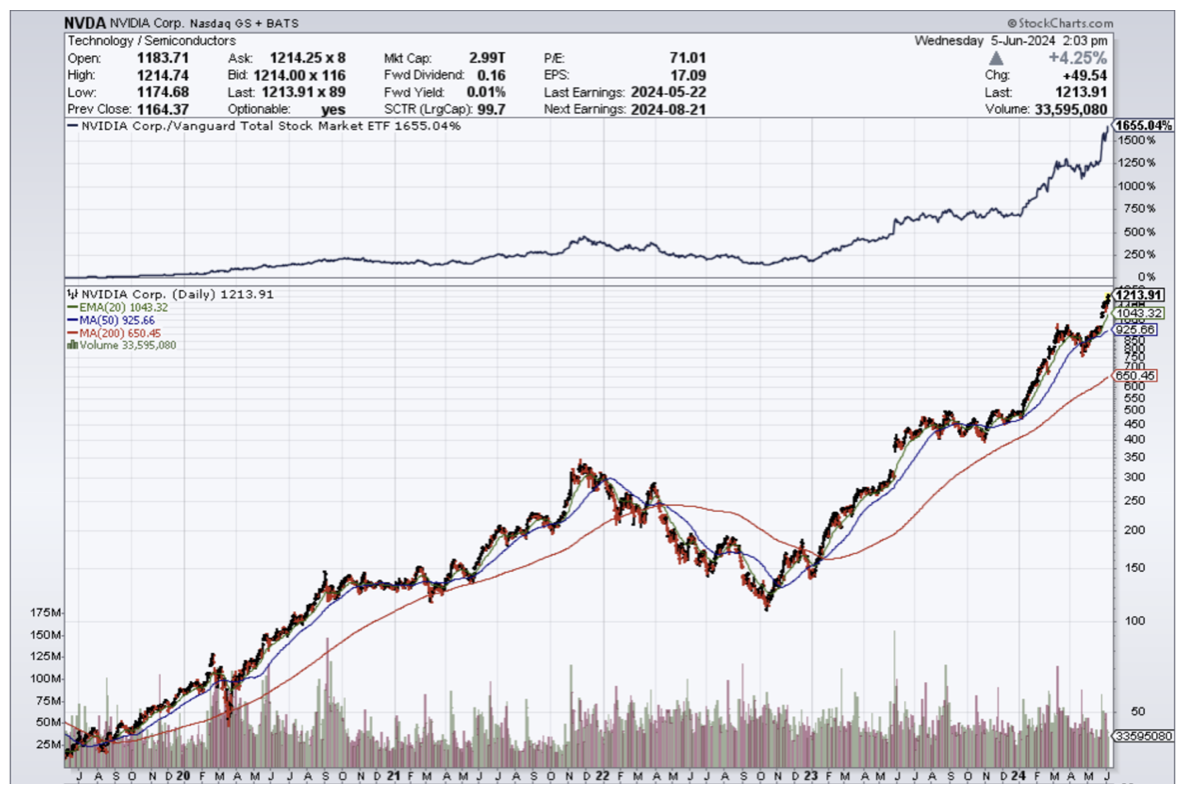

If anyone knows a successful trader that has made a nice living shorting Nvidia (NVDA) in the last year then I would like to meet that person.

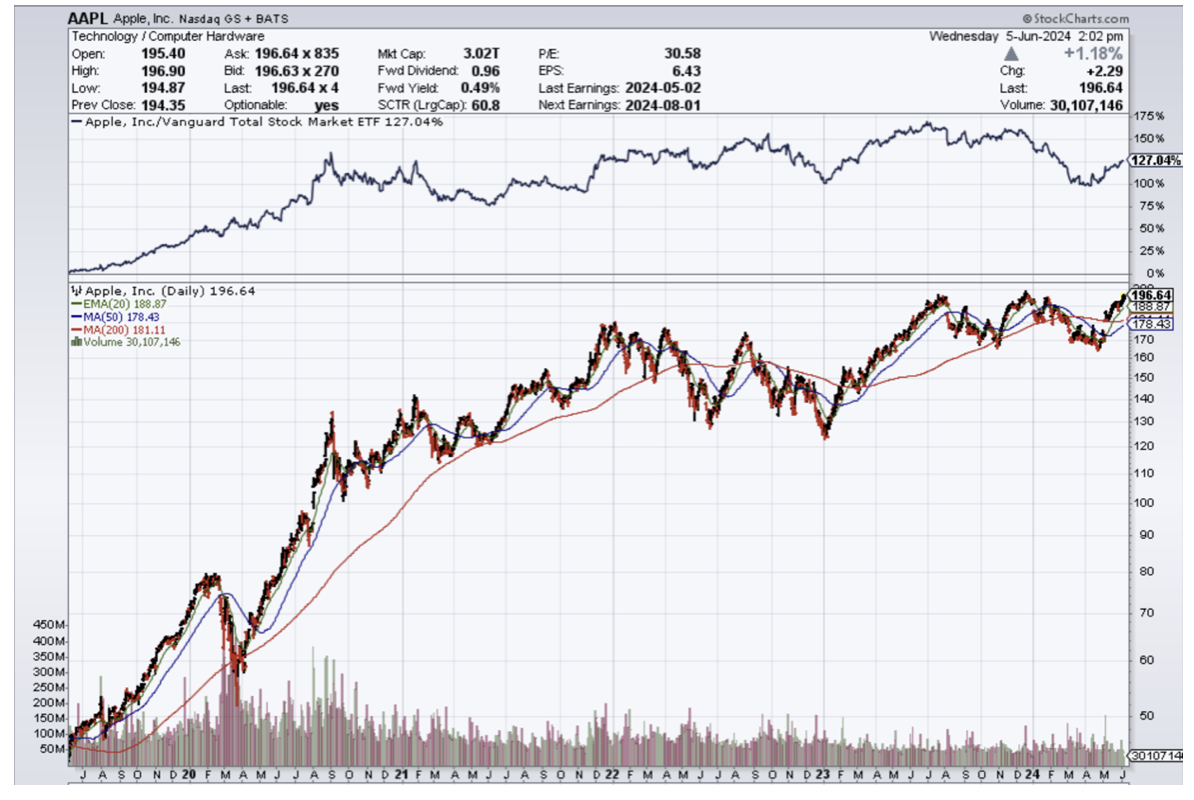

Likewise goes for Apple over their massive bull run.

Shorting the best tech stocks in the world usually meant financial underperformance.

Just in recent memory, the whole Gamestop spike up when a bunch of hedge funds had massive short positions.

Short sellers were the ones run over by the GameStop phenomenon.

Retail traders have flexed their muscles again in the past two months, with shares of several meme-stock favorites including GameStop surging anew.

Meme-stock dramas demonstrate a “gamification” of the market that has undermined the whole short-selling industry.

And remember that GME is a garbage company with paltry revenue that surges for alternative reasoning.

Practitioners say it’s getting increasingly difficult to attract new cash for a risky bearish approach (the downside of short selling is theoretically limitless), whether for an activist firm or simply a short-biased fund.

Assets in his RC Global Fund, which wagered against tech companies both in China and the US, had dropped to $200 million from about $1.7 billion six years earlier. The Asia positions had paid off, but going against mighty American megacaps hammered performance.

The longer the cycles go, the more short selling seems to be simply a bad investment strategy and out of favor.

The idea is that a relentlessly rising market not only creates the kind of overvalued companies short sellers will ultimately feast on, it also masks badly run and sometimes fraudulent businesses.

That may be especially true when short selling is at such a low ebb since bearish activity has been shown to act as a brake on bad corporate behavior and keep the prices of companies with questionable financial statements in check.

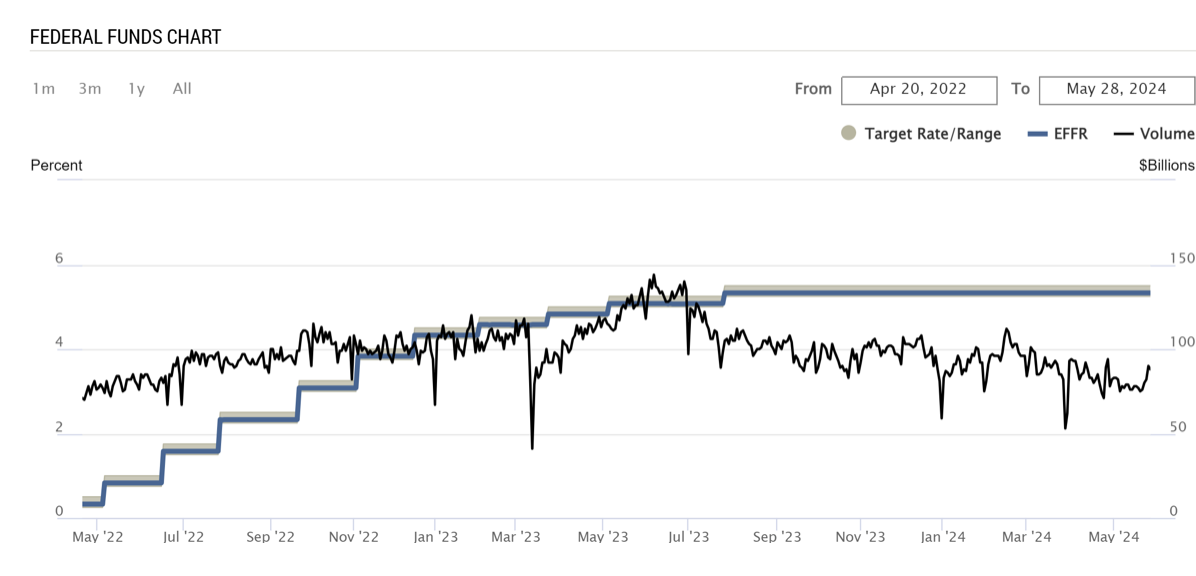

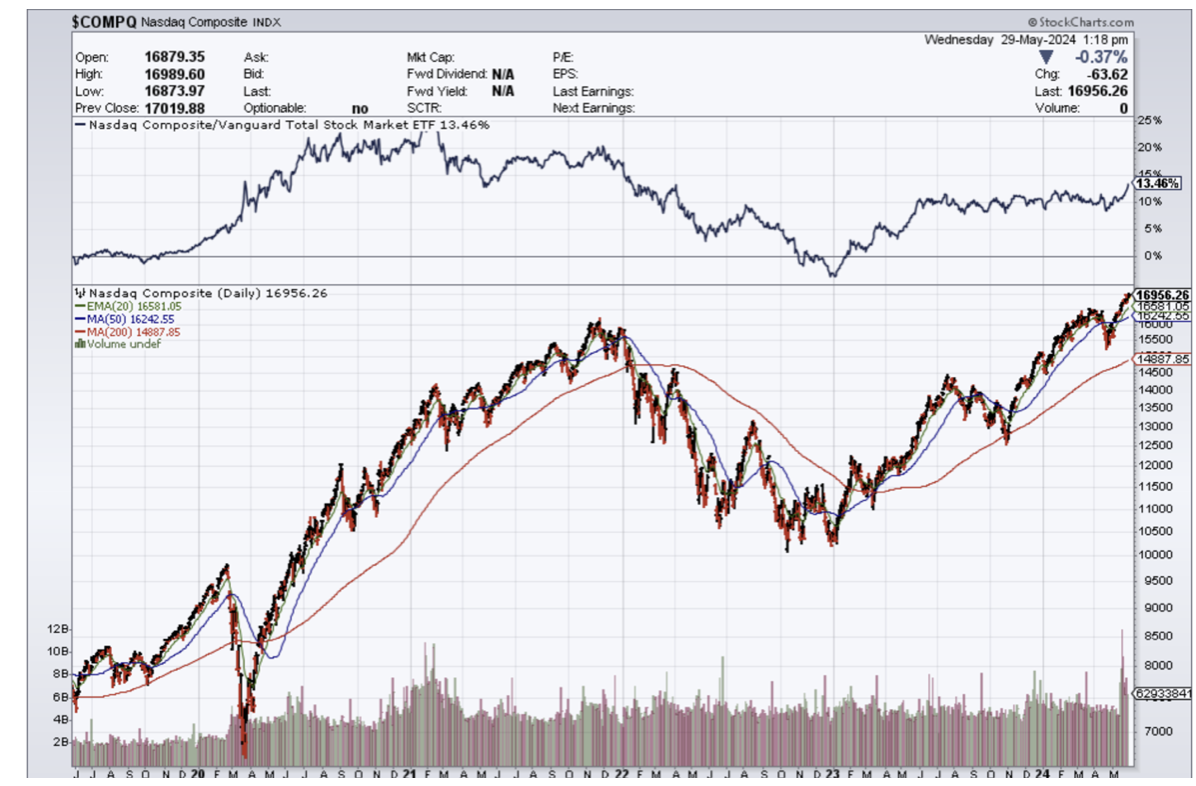

Yet even as central bankers around the world have lifted interest rates back to levels not seen in decades — usually a handbrake on equity markets — stocks have generally churned higher, making it difficult to sustain bearish bets for any length of time.

In an era of 5% interest rates, it is not viable to borrow that capital to bet against skyrocketing AI stocks like Nvidia.

Why not ride the elevator up with Nvidia?

The absence of short sellers has meant “all systems go” for tech stocks and they have been off to the races with almost no pushback.

The bullishness has been so intense that the faster rate hike cycle in the modern financial history has done little to dissuade investors from pouring into tech stocks.

As interest rates lower from 5% to 2 or 3, tech stocks are likely preparing to lift off into another stratosphere.

If lowering rates catalyzes tech stocks to the upside, imagine how demoralizing for the few if any short sellers left shorting tech.

I am bullish on tech stocks in the short-term with the Central Bank telegraphing a drop in Fed Funds rates.

Mad Hedge Technology Letter

June 3, 2024

Fiat Lux

Featured Trade:

(RAISING SUBCRIPTION PRICES MEANS PROFITS FOR SPOTIFY)

(SPOT), (NFLX)

Spotify (SPOT) is raising prices and the underlying stock is up 4% this morning.

Shareholders are happy and there is more to come from this European giant.

Much of the same pricing behavior has been experienced in products like Netflix whom are incentivized to raise prices to get that extra juice out of its stock.

Why not raise prices when customers are happy to pay for it?

Remember, this only works when a company is part of a duopoly, monopoly, or something of that nature where they have a firm grip on pricing power.

Consumers are willing to shell out that little extra bit for Spotify because the competition is so much worse.

This has been going on for quite a while and tech was famous for the “freemium” model built on free services.

After building a significant audience and hooking the audience for free, a subscription-based model was rolled out to monetize the customer base.

Spotify is looking to extract a little more from the premium customer.

The price of Premium Individual will pay more so that SPOT can continue to invest in and innovate the product offerings and features then levy another major price hike.

That’s the game in tech land and we roll with the punches.

The company offers an advertising-supported free service with limited features and a subscription-based paid service that gives access to all its functionality, with premium subscribers accounting for most of its revenue.

The streaming giant could drive further growth by offering tailored subscription plans based on consumer preferences in verticals such as music, audiobooks, and podcasts.

The company's quarterly gross profit topped $1.08 billion for the first time in April after it reined in marketing spending.

Its premium subscribers rose by 14% to 239 million and it forecast monthly active users at 631 million for the second quarter.

The company offers an advertising-supported free service with limited features and a subscription-based paid service that gives access to all its functionality, with premium subscribers accounting for most of its revenue.

I believe the streaming giant could drive further growth by offering tailored subscription plans based on consumer preferences in verticals such as music, audiobooks, and podcasts.

Since we are in the last stage of the economic cycle, expect tech companies to pull out all the bells and whistles to charge extra for the software, hardware, and other tech.

Being that we are late cycle, there is an incredible push for that last incremental dollar before the economy goes into recession and I do believe that tech companies will behave in a somewhat mercantile way to get what they want.

Tech companies, especially the bigger ones, have a massive incentive to stave off a recession for one extra quarter so that much of the management can cash out at all-time high stock prices with vested shares.

Tech will eventually experience a steep pullback in shares and the longer that is staved off, the better for everyone because who knows what the next iteration of tech will look like.

It could become more corporate which would mean higher prices for the consumers and higher shares prices for stocks like SPOT.

Remember that the only thing in tech that is certain is change and that is what we will see. It’s sooner than you think and right around the corner for many tech companies.

In the meantime, expect higher product prices for streaming and software products like Spotify, Netflix, and other lookalikes that will lift corresponding share prices.

Mad Hedge Technology Letter

May 31, 2024

Fiat Lux

Featured Trade:

(ANOTHER AI SERVER STOCK)

(DELL), (SMCI), (NVDA), (ORCL)

Nvidia CEO Jensen Huang complimented Dell by saying it’s a “great partnership” at its GTC conference and said that “nobody is better at building end-to-end systems of very large scale for the enterprise than Dell.”

Words like this go a long way in this industry let alone partnering with the best tech firm in the industry.

To have the best CEO in tech flatter your products means staying power but in the short-term, the stock has come too far too fast.

That’s what this deep selloff is about as Dell shares.

The stock is down 19% today but that doesn’t diminish the 207% gain in the past 365 days.

Dell has reinvented itself as an AI stock and specifically a company specializing in servers that serve AI chips.

The company has done so well lately that they are gearing themselves up for inclusion into the S&P index.

That would honestly be a game-changer for the stock.

Super Micro Computer (SMCI), another play on AI servers, was added in March, despite having a market cap below $50 billion.

Confirmation of improving growth prospects could continue to support a stock that’s at a record high while trading at a discount to other tech favorites.

Dell recently generated excitement by unveiling a line of PCs optimized for AI, adding to hopes that such features could prompt a long-awaited upgrade cycle from customers and businesses. HP even reported the first increase in PC sales in two years.

The firm has become a critical cog in the AI ecosystem.

Both the PC and the server businesses will drive growth in coming years, and that’s supportive of both the stock price and the multiple.

I believe we can now say the company has turned itself into both a growth and a value play since the growth story is still under-appreciated and the multiple is very low relative to other AI plays.

The S&P 500 is rebalanced quarterly, with the next scheduled to occur in June. Becoming a component would open Dell up to a fresh avalanche of investors who use the S&P 500 as their benchmark, as well as flows into passive funds that track the index.

All things considered, I believe this is one of the best tech stocks to play server momentum, sky-rocketing storage demand, and an improving PC market.

Dell is becoming an increasingly strategic vendor in AI, but there’s a lot more appreciation for this than there was a few months ago.

Demand for AI systems remains healthy, but other parts of the business remain cyclical, and if we see a macro downturn, even a growth story as powerful as AI could slow down.

I like that investors are looking through the bad PC numbers and only focusing on Dell's AI server story.

This means that readers should be dissuaded from reach for this tech play even though they have a saturated computer business.

The most important and hardest endeavor in the tech industry is to reinvent when business is slowing down.

Only so many firms can pull it off and now that the pivot is into AI, companies are scrambling like Google and Apple in order to stay relevant.

Dell is a stock that should be bought on dips now and I feel funny saying that because that wasn’t the case not too long ago.

Another stock that has reinvented itself with the AI craze has been Oracle (ORCL).

Mad Hedge Technology Letter

May 29, 2024

Fiat Lux

Featured Trade:

(THE GRIND HIGHER)

(FED FUNDS RATE), ($COMPQ)

Rates will stay higher for longer and the higher income bracket will carry the US economy through any conflict with short-term inflation.

What does that mean for tech stocks?

It will trend higher for longer.

Sure, US rates will stay elevated, but tech stocks have proven they are tough to keep down with elevated inflation.

Most who buy tech stocks have done very well financially in the past 18 months.

There is a high likelihood that higher rates won’t affect their purchasing power to buy more tech stocks.

I do admit a big chunk of Americans are missing out on buying tech stocks at these current prices – I don’t diminish that.

The big spenders have utilized their 3% fixed mortgage to hunker down and continue to spend on devices, software, EVs, and other tech.

This clearly means that 5% isn’t the real neutral rate that the Fed is looking for and I view this rate as a relatively loose fiscal policy that is allowing high-income Americans to splurge on more tech products.

Don’t forget that these are the same stockholders that are reaping increasing tech dividends, higher-tech stocks, and generous shareholder returns.

Further evidence is that the $2 trillion in quantitative tightening along with a 5% Fed Funds rate has resulted in the S&P index rising 37%.

That’s not supposed to happen if rates are high above the neutral rate.

What the Fed gets wrong is that the neutral rate has moved significantly higher when we consider the trillions that were printed for the pandemic programs and stimulus checks.

The additional amount of fiat paper floating around chasing a limited amount of goods results in the neutral rate being somewhere closer to 8-10% and that development gets missed by the Fed.

Therefore, 5% Fed Funds rates are “high” and a lot higher than 0%, but the wealthy have now used this rate as a tailwind to progress their financial goals.

Wealthy households right now can earn upwards of 4.5% in a high-yield savings account, see their tech portfolios go up 20% in a year, and are watching the value of their real estate holdings surge higher.

Given the amount of wealth concentrated among a handful of US households and the skew on the income distribution in the US, just about any change in monetary policy will be regressive, advantaging those with more at the expense of those with less.

Tuesday's consumer confidence reading — while registering a three-month high — was far from a clear-cut judgment from Americans that things are looking up, economically speaking.

If the Fed holds at 5% and fails to erect rates closer to 8%, tech stocks will grind higher.

Rates would need to be at a nominal number that would give pain to higher-income buyers.

My personal view is that the Fed will stand pat at 5% interest rates and the Nasdaq should perform well in this scenario.

If we get talk of 6 or 7%, tech stocks will produce a minor pullback delivering another fabulous opportunity to buy.

The other piece here is Nvidia delivering stellar earnings and that should keep the shine on high-quality tech stocks when the market sets up to make the next move.

My bet is any dip will be bought ferociously and any “dip” could turn out to be more of a sideways time correction before we rip higher.

This is also why Nvidia is close to 81% above its 200-day moving average and boasts a current $2.7T valuation.

Mad Hedge Technology Letter

May 24, 2024

Fiat Lux

Featured Trade:

(CBDC BANNED BY THE HOUSE)

(CBDC), ($COMPQ)