Man is not free unless government is limited.” – Said Former US President Ronald Reagan

Man is not free unless government is limited.” – Said Former US President Ronald Reagan

Mad Hedge Technology Letter

May 3, 2024

Fiat Lux

Featured Trade:

(ARE 8% RATES GOOD FOR TECH?)

(GOOGL), (AAPL), (JPM)

Although much of the mass media ignores some of these dire reports issued by some prominent finance guys, I have taken notice.

I’m not here to scare you.

Everything will work out fine.

It was only just lately that one of the most public-facing US bankers, Jamie Dimon, delivered us a future warning that could mean bad results for many tech companies.

I won’t say that every tech company will be ripped to shreds, there are still a few that are head and shoulders above the rest and could withstand heavy shelling.

But 8% rates is a world that could spook tech investors.

It just goes to show that some numbers floating around are starting to come into the realm of possibility even if the probabilities are quite low.

Dimon’s thesis centered on “persistent inflationary pressures” and unless you’re an ostrich with your head in the ground, prices haven’t come down for most stuff that we buy including software and tech gadgets.

Rates close to 10% would kill many golden gooses in various industries and I do believe a world of rates that high would really put the sword to the throat of many tech companies.

If that happened, kiss the tech IPO market goodbye and just be happy that we squeezed into Reddit this year.

More often than not, American tech companies are gut-punched when there is a global growth slowdown because many of these companies extract revenue from everywhere.

They are so big that they have to unearth every stone in far-flung places to keep the growth narrative chugging along.

The unemployment rate remains below 4% and businesses, but a world of 8% interest rates would mean another 50% downsizing of tech staff and a rockier path to profits.

Amidst heightened global uncertainty, what has the technology sector delivered to us lately?

Shareholder returns.

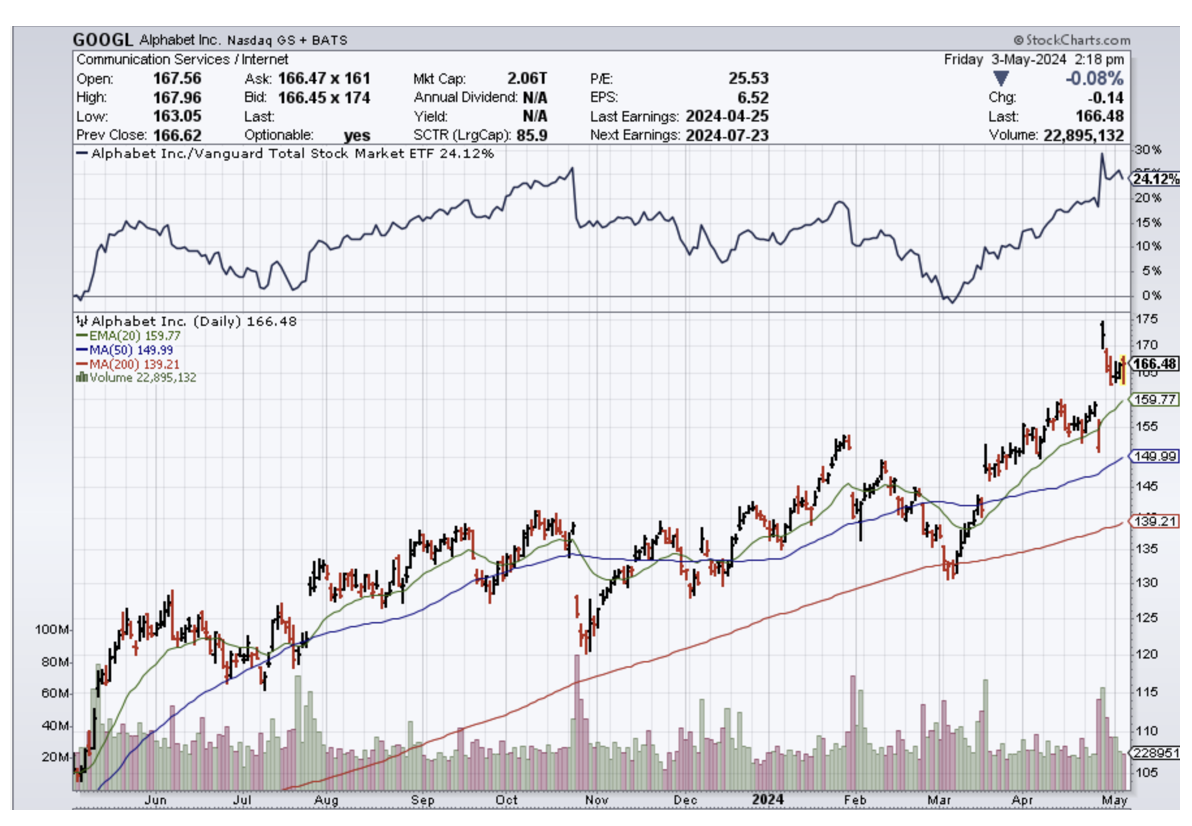

Google rolled out the carpet for its first-ever dividend.

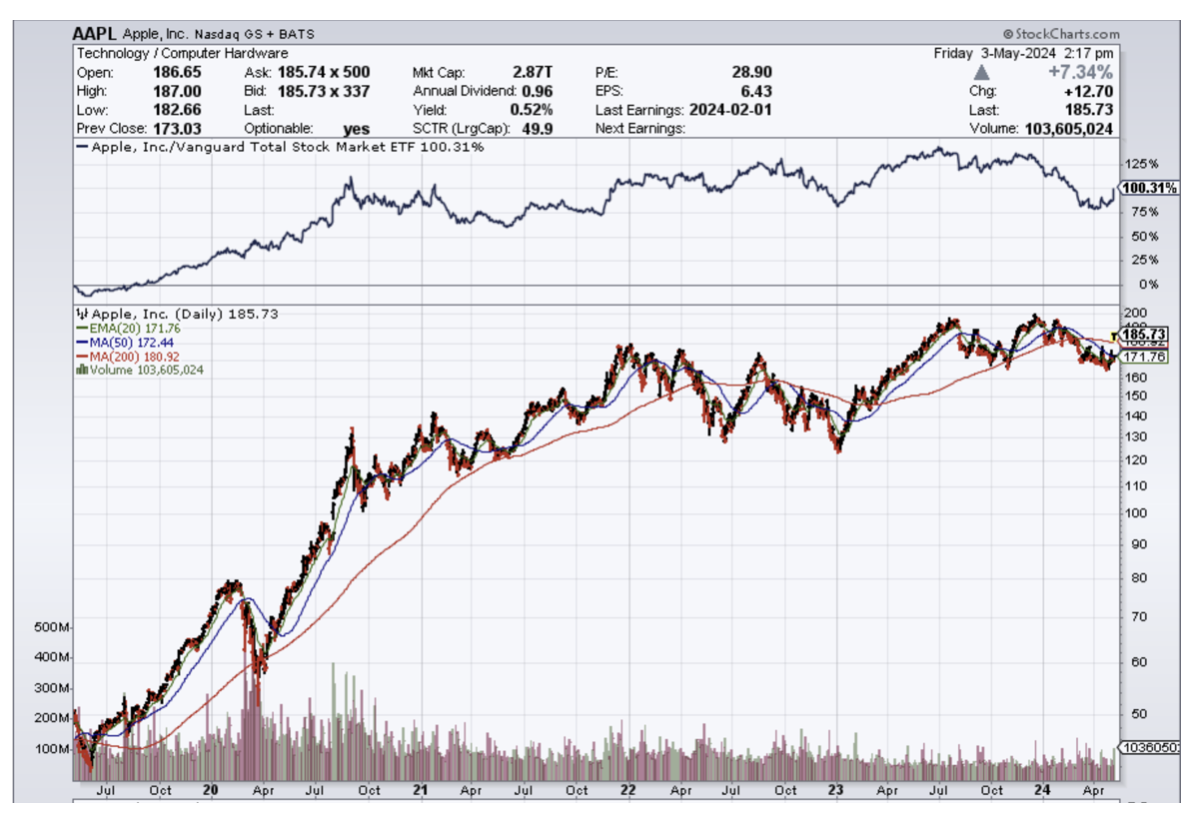

Apple increased its dividend by announcing a new $110 billion share repurchase plan.

What is my takeaway here?

Has Apple run out of bullets here so much so that a share buyback is better to do than give its clients a new product?

They do this also because they can afford to and many tech companies would view this as a luxury.

However, there will come a time where the market will demand a new killer product and that day is inching forward.

How do I know that?

iPhone sales are down 10% in the first 3 months of 2024 and that is absolutely awful.

Even if the market looks through these terrible numbers, the day of reckoning inches up, and when it comes, not even a shareholder buyback will massage the stock higher.

Like a magician, this earnings season was a great escape for tech, and I question how many more earnings seasons will they get a pass for.

In a scenario of 8% interest rates, 95% of tech stocks would drop and a few heavyweights would be forced to carry the load. Psychologically, it would scare off the incremental tech investor and that is the bigger problem.

There is only so far the can is able to get kicked down the road.

In the short term, I would be inclined to buy on the dip after we can digest this mediocre earnings season, but at some point, this “bad news is good news” will disappear with the wind.

Man is not free unless government is limited.” – Said Former US President Ronald Reagan

Mad Hedge Technology Letter

May 1, 2024

Fiat Lux

Featured Trade:

(THE BIG RETAILER DIVING INTO FINTECH)

(WMT), (PYPL)

The takeaway I get from Walmart’s (WMT) push into fintech is that fintech is becoming mighty crowded in the short-term and this trend most likely won’t change anytime soon.

Walmart has been one of the big companies trying to beef up online commerce so it’s no surprise that wants to marry up this initiative with an in-house digital payment mode.

It could be that sometime in the near future that the likes of PayPal, Klarna, and Affirm who don’t have their e-commerce platform will be muscled out of this digital payment space.

Walmart’s in-house fintech startup One has begun offering buy now, pay later loans for big-ticket items at some of the retailer’s more than 4,600 U.S. stores.

The move puts One raises the question of whether major retailers need the help of outside payment apps.

Right now, Affirm, the BNPL leader has been the exclusive provider of installment loans for Walmart customers since 2019.

One is a mobile one-stop shop for saving, spending, and borrowing money.

Affirm helped the WMT generate $648 billion in revenue last year.

Ironically enough, offerings from both One and Affirm are available at checkout, and loans from either provider are available for purchases starting at around $100 and costing as much as several thousand dollars at an annual interest rate of between 10% to 36%.

Electronics, jewelry, power tools, and automotive accessories are eligible for the loans, while groceries, alcohol, and weapons are not.

One’s no-fee approach is especially relevant to low- and middle-income Americans who are “underserved” financially.

One could generate roughly $1.6 billion in annual revenue from debit cards and lending in the near term, and more than $4 billion if it expands into investing and other areas, according to Morgan Stanley

Walmart can use its scale to grow One in other ways. It is the largest private employer in the U.S. with about 1.6 million employees, and it already offers its workers early access to wages if they sign up for a corporate version of One.

Fintech players including Block’s Cash App, PayPal, and Chime dominate account growth among people who switch bank accounts and have made inroads with Walmart’s core demographic.

The three services made up 60% of digital player signups last year.

One has the great advantage of being majority-owned by a company whose customers make more than 200 million visits a week.

It can offer them enticements including 3% cashback on Walmart purchases and a savings account that pays 5% interest annually, far higher than most banks, according to customer emails from One.

One has access to Walmart’s sizable and sticky customer base, the largest in retail and that is worth a lot right there.

It’s entirely feasible that Walmart keeps growing its digital platform and in-house fintech app to somewhat look like a tech company in a few years.

I’ve written a few times about how Walmart is mimicking many of the best practices from the great tech companies and who knows, they might even employ a cloud division to take care of its own data and warehouse operations.

The day where outsourcing much of the data to software companies is very much over for big companies like WMT who are making deep inroads and investment into their tech prowess.

WMT’s stock has always been given that non-tech premium and I believe that will slowly change around as the growth rates start to pick up.

WMT is one of those American companies that are strongly positioned to do well in inflationary times and picking up all the $100,000 per year white collar professionals is a massive victory as they figure out ways to monetize this higher spend base.

This is a great company to buy on any dip and hold long term.

“The most terrifying words in the English language are: I'm from the government and I'm here to help.” – Said Former US President Ronald Reagan

Mad Hedge Technology Letter

April 29, 2024

Fiat Lux

Featured Trade:

(JUST GOOD ENOUGH)

(META), (F), (IBM), (MSFT)

This earnings season is chugging along exactly like I thought it would play out.

The haves are covering for the have-nots.

Sadly, the pixie dust isn’t encompassing all tech stocks, but just enough sprinkles so investors don’t start selling.

That is what matters most and sure, investors can knit-pick all they want, but there have been just enough positive numbers to be repackaged as a win for AI and the advancement of tech even if the proverbial goalposts are widening.

Competition has reared its ugly head as tech services fight for the extra consumer and enterprise dollar in a global economy where demand is being squeezed by sticky inflation.

That’s not good news for many of the smaller companies that are unproven and tap debt by delivering a promising story to prospective investors.

Remember that Mr. Market is undefeated and price will always find its natural equilibrium.

The question is how long will it take to find that natural equilibrium?

Since 2020, many would say that the irresponsible monetary policy in many areas of the world has contributed to markets unable to match up buyers and sellers at a reasonable price.

There is some truth to that but let’s see who that benefits.

My belief is that strong tech companies have overly benefited from this type of fiscal backdrop because they can always fall back on a strong balance sheet like in Google’s case where it suddenly issued a dividend.

View it as a rainy day fund if you will where they can wield when need be.

The extra buffer zone of safety has allowed a company like Microsoft to focus on Azure growth, of which 7% was related to AI, up from 6% of impact in the previous quarter.

Microsoft provides cloud services for the ChatGPT chatbot from startup OpenAI, and companies have been increasingly adopting Azure AI services to develop their capabilities for summarizing information and writing documents.

It’s a good problem to have when capacity bottleneck cuts into the AI portion of Azure growth.

Companies tapping that AI story are the only tech companies in 2024 that Mr. Market is keeping safe and that must scare or enthrall you depending on who you are.

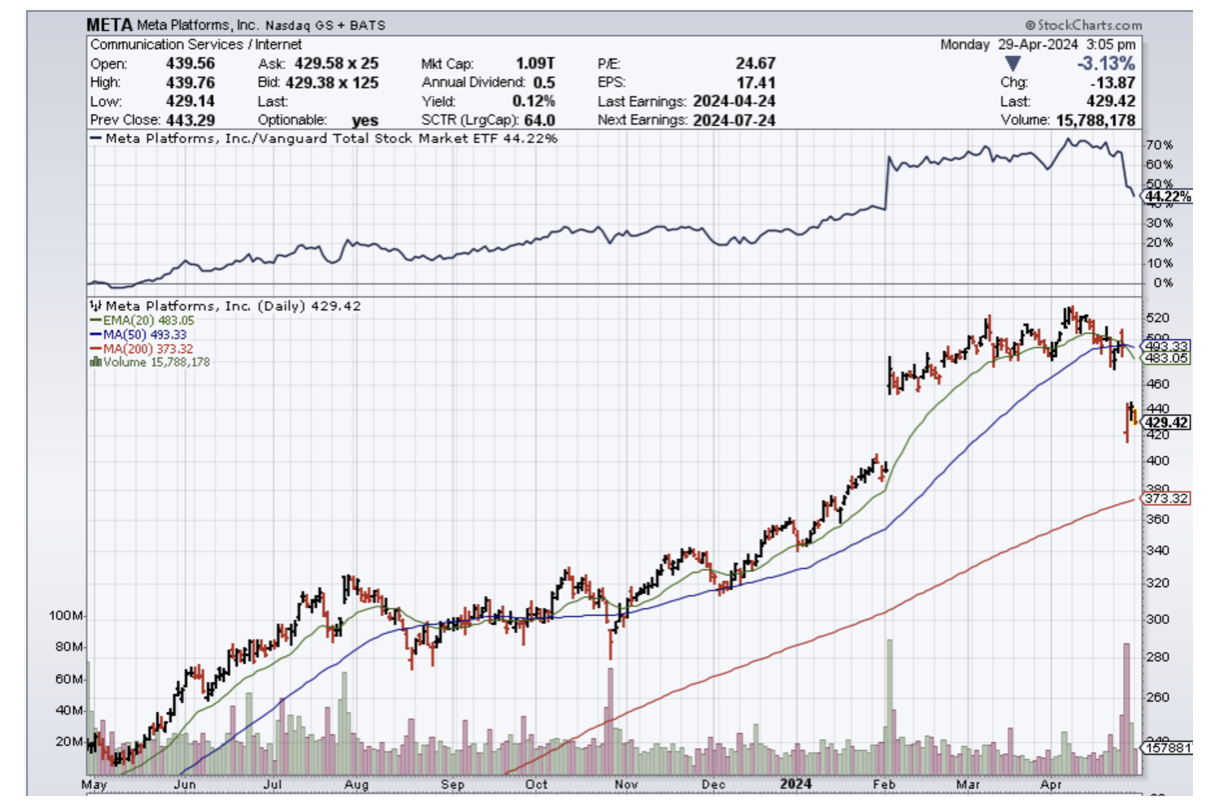

Meta (META) materially lifted its full-year capital expenditures guidance and signaled even bigger spending in 2025 — all because of unknown AI projects. Running tech businesses isn’t getting cheaper so imagine how small companies feel about that.

It’s Ford (F) losing lots of money on EVs because of higher-than-expected costs.

Meanwhile, IBM (IBM) CFO Jim Kavanaugh struck a more cautious note when asked about soft sales at its lucrative consulting business blaming the macroeconomic backdrop.

It’s not all smooth sailing in tech land and readers need to be vigilant.

It’s not the time to take some speculative Hail Mary on some far reach.

Don’t draft a 7th-round prospect in the 1st round.

Price action has been unkind to tech firms with poor balance sheets in 2024 and I believe that trend to continue until the Fed can finally tamper inflation back to reasonable levels.

“The future doesn't belong to the fainthearted; it belongs to the brave.” – Said Former US President Ronald Reagan