Mad Hedge Technology Letter

April 1, 2024

Fiat Lux

Featured Trade:

(THE STREAMING WARS WIND DOWN)

(NFLX, (PARA), (WBD)

Mad Hedge Technology Letter

April 1, 2024

Fiat Lux

Featured Trade:

(THE STREAMING WARS WIND DOWN)

(NFLX, (PARA), (WBD)

For certain segments of the technology sector, it sure does feel like they are fully saturated.

I am not referring to AI, because that is in the early innings of a seismic movement.

However, let’s take a look at streaming.

This category was invented by Netflix (NFLX) and now the whole country pays for streaming.

Netflix had the first-mover advantage and took the initiative.

For the leftovers, the pain and struggle with creating a profitable streaming business is real.

Is the year 2024 the year when streaming management has that Aha moment?

Many have instructed us to stay on board the ship while losses bleed uncontrollably.

Everyone is fighting to be one of the three or four streaming services people can’t live without.

Paramount Global (PARA) is under pressure to abandon its namesake streaming service, and Warner Bros. Discovery (WBD) is desperate for partners that offer Max a better chance to compete with the likes of Netflix.

Let’s look at Disney right now.

Streaming grew quickly from launch in 2019 — we’re talking now about Disney+, ESPN+, and Hulu — but even with strong sales, they are sitting on big losses.

Disney board member Nelson Peltz is unhappy, as outlined in a 133-page manifesto published March 4, that Disney “belatedly” entered the streaming game and has a “poorly planned" strategy to catch up with the likes of Netflix.

He takes issue with Disney trying to achieve scale in streaming by buying Fox’s entertainment assets for $71 billion in 2019 because he thinks it exposed the company more to the dying linear TV business.

He also can’t believe that a company reporting more than $22 billion of run-rate streaming revenue annually is still losing money.

Peltz wants a digital strategy for the ESPN sports assets..

Peltz wants a succession plan put in place for current CEO Bob Iger, who extended his contract with Disney last year after a coming-out-of-retirement return to the company in 2022.

In February, Disney teamed up with Fox and Warner Bros. Discovery to create a streaming service for college and pro sports that you can currently only find on TV.

That seems like what Peltz was asking for. Disney also invested $1.5 billion in Epic Games and gave access to the Fortnite maker for gaming portrayals of Star Wars, Marvel, and Avatar.

The bottom line here is that streaming is not nearly as profitable as many insiders first thought.

Streamers thought they could scale up and acquire subscribers at a loss and then raise prices.

That business model was only for Netflix to accomplish because they started so much earlier than anyone else.

The best of the rest are now saddled with loss-making companies and the cost of content post-covid has never been pricier.

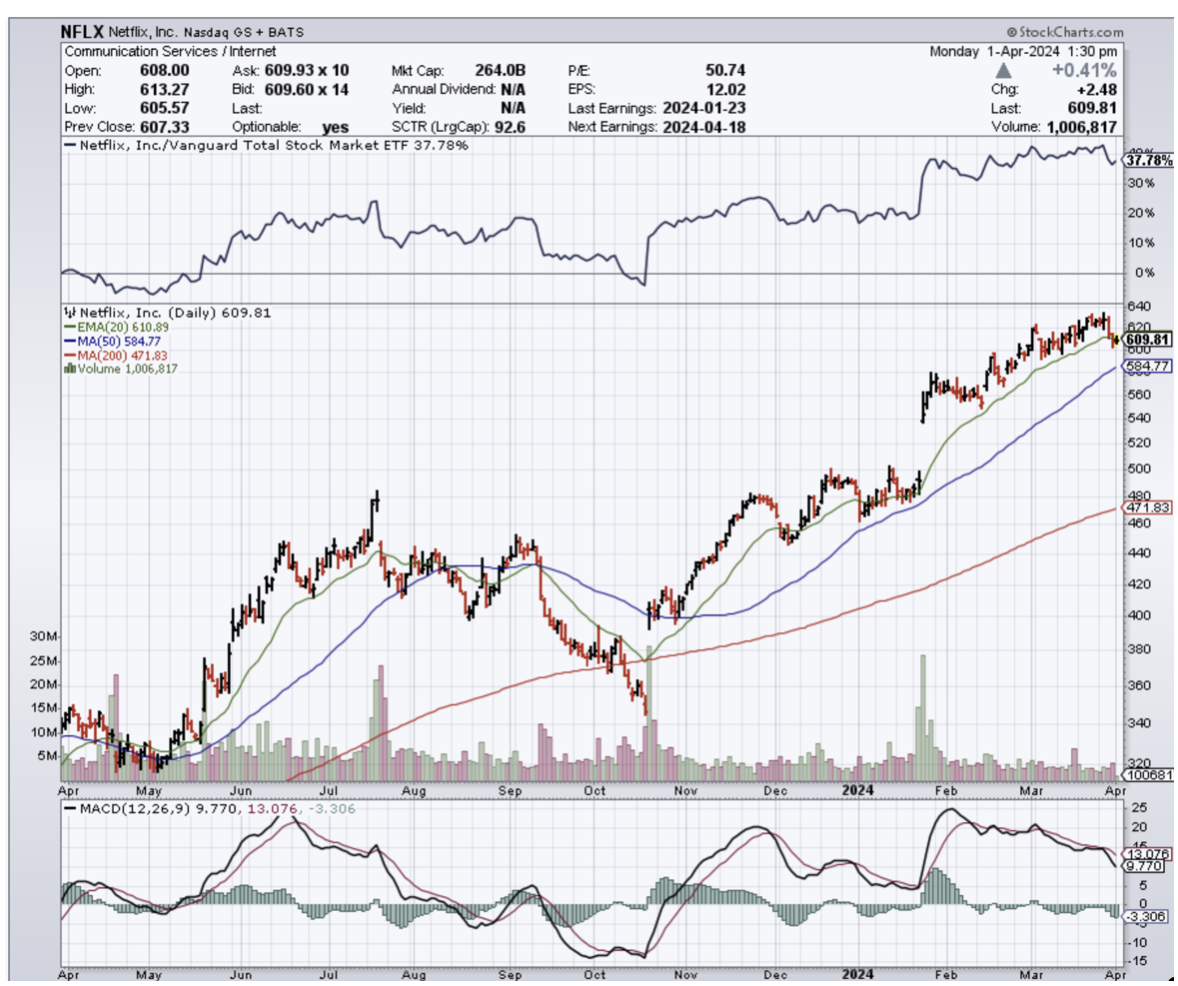

Netflix shares have had a nice run in the last 365 days going from $180 per share to over $600 per share.

A lot of that price movement was an acknowledgement that they are dominating streaming compared to the other legacy corporations that have tried their hand in this game.

Instead of jumping into the legacy TV players turned streamers, I would tell readers to wait for Netflix on the dip.

It’s been tried and tested over time and any big dip should and will be bought by investors.

There is not a lot of room for stocks other than Netflix in a sub-sector of rather scarce any AI.

“In the business world, the rearview mirror is always clearer than the windshield.” – Said American Investor Warren Buffett

Mad Hedge Technology Letter

March 27, 2024

Fiat Lux

Featured Trade:

(TAIWAN IS ON THE MAP)

(AAPL), (TSM)

I know it’s not the sexiest choice but there is a chip company in Taiwan that readers need to look at.

This company has investments all over the world and is the leader in what they do.

They are also involved in AI which lately has been the ticket to riches.

Taiwan Semiconductor Manufacturing Company (TSM) may not seem like a glamorous AI stock, but it's as critical to the AI future.

To understand TSMC's role in AI, you need to understand how we get to end consumer-facing products like ChatGPT, Bard, and other generative AI applications.

For AI to be effective, it must be trained using lots of data -- quantities that must be stored in specialized data centers.

Data centers rely on graphic processing units (GPUs), which are essentially the brains of AI computing systems.

TSMC and the semiconductors it manufactures for its client companies are crucial in this process. These GPUs rely heavily on TSMC's best-in-class manufacturing processes.

This AI knock-on effect hasn't impacted TSMC's financials yet, but management said they expect sales of its AI-related semiconductors to grow at a compound annual rate of 50% for at least the next few years.

By 2027, AI-related semiconductors are expected to be responsible for a large part of the company's revenue.

TSMC will absolutely be additive to the AI ecosystem.

Let’s talk about their products.

TSMC's 3nm fabrication process accounted for 15% of the company's revenue in 2023.

Only one of TSMC's customers used it at the time:

Apple (AAPL).

The three-nanometer product is where it’s at.

Wasn’t it just a year or 2 ago we were at 7 nanometers?

As more customers adopt the manufacturing process, 3nm process nodes will account for a considerably larger share of TSMC's revenue.

This year TSMC's N3-series nodes — including N3B and N3E — will account for over 20% of the foundry's revenue in 2024.

Apple currently exclusively uses TSMC's N3B to make its A17 Pro system-on-chip (SoC) for smartphones, as well as the M3-series processors for iMac desktops and MacBook laptops.

AMD is preparing to launch its new Zen 5-based processors made on 3nm- and 4nm-class process technologies later this year.

Apple's new iPhone 16 series will be equipped with the A18-series processor, and the upcoming M4-series processors for Mac PCs will also be produced using TSMC's 3nm technology.

This marks the first time Intel has entrusted TSMC with the full range of chips for its mainstream consumer platform, the report notes.

This collaboration highlights TSMC's expanding role in serving Intel, which also happens to be the company's rival in the foundry market.

With three major customers using TSMC's 3nm family of process technologies, this company needs to be on readers’ radar.

More companies are expected to adopt TSMC's N3 nodes in 2025, including performance-enhanced N3P, and the report suggests 3nm will account for over 30% of TSMC earnings in 2025.

It’s easy to see with the mushrooming of business for TSMC, how they are a highly sought-after stock.

It also explains why the stock has been on a tear.

It was only just last May they were trading at $82 per share and fast forward to today at the stock sits at $136 per share.

Holding this stock long term has borne fruit and every big should be bought.

They will continue to be the best at what they do.

Mad Hedge Technology Letter

March 25, 2024

Fiat Lux

Featured Trade:

(REGULATIONS REGULATE TECH)

(AAPL), (GOOGL), (META)

I’m not saying the time is up for big tech.

The Magnificent 7 are still by and far great companies who print money.

They dominate in a way that was unfathomable just a generation ago.

Trillion-dollar companies are now commonplace in tech and we have pushed into valuations of over 2 and pushing towards $3 trillion.

Success like this easily could make them easy targets and that is what has become of them in Europe as Apple (AAPL), Google (GOOGL), and Meta (META) are in the firing line under the sweeping new Digital Markets Act tech legislation.

Apple has already been slapped on the wrist quite hard with a $2 billion fee after the European Commission said it found that Apple had applied restrictions on app developers that prevented them from informing iOS users about alternative and cheaper music subscription services available outside of the app.

In a third inquiry, the commission said it is investigating whether Apple has complied with its DMA obligations to ensure that users can easily uninstall apps on iOS and change default settings. The probe also focuses on whether Apple is actively prompting users with choices to allow them to change default services on iOS, such as for the web browser or search engine.

The fourth probe targets Alphabet, as the European Commission looks into whether the firm’s display of Google search results to choosing its own products over other services.

The fifth and final investigation focuses on Meta and its so-called pay and consent model. Last year, Meta introduced an ad-free subscription model for Facebook and Instagram in Europe. The commission is looking into whether offering the subscription model without ads or making users consent to terms and conditions for the free service is in violation of the DMA.

If any company is found to have infringed the DMA, the commission can impose fines of up to 10% of the tech firms’ total worldwide turnover. These penalties can increase to 20% in case of repeated infringement.

Preferring one’s own product from companies like Apple, Amazon, and Google is not a shocking phenomenon. Business can be a dirty game and self-selecting ones products because they own the platform they are sold on is almost common knowledge to the average consumers.

Organizational bodies like the European Commission have an incentive to fine American tech companies that do business in Europe.

Europe has no alternative apps and aren’t competitive in the tech space.

The desperate reach of European bureaucracy has decided to just steal the money in the form of tech fines instead.

One big takeaway that sticks out like a sore thumb is the clear trend to the low-hanging fruit being plucked.

The incremental dollar will be harder to earn for big tech as regulatory commissions around the world zone in on their anti-competitive practices.

I doubt that fines will get so big to the point that these tech firms will go bankrupt, but this could set the stage for a slew of earnings misses which could knock down the share prices.

I still believe these stocks are buys, but only after they are beaten down and repriced.

I wouldn’t go chasing here with regulatory issues rearing its ugly head and revenue forecasts disappointing.

If I had to choose one to avoid then it would be Apple.

“Great achievers are driven, not so much by the pursuit of success, but by the fear of failure.” – Said Co-Founder of Oracle Larry Ellison

Mad Hedge Technology Letter

March 22, 2024

Fiat Lux

Featured Trade:

(REDDIT HAS SOME JUICE)

(RDDT), (META)

Readers who missed out on stocks like social media platforms like Facebook (META) now have a chance to grab a pillar of social media in American society.

Reddit (RDDT) went public yesterday and jumped 48% by the end of the trading day cementing its place as a top player of social media stocks in Silicon Valley.

The valuation now is $8 billion and we are just getting started as tech IPOs reverse from its recent dormant activity.

The strong showing by Reddit, along with AI-focused semiconductor connectivity company Astera Labs whose shares have gained 78% since its IPO Tuesday, provides a promising backdrop for other IPO candidates such as Microsoft-backed data security startup Rubrik and health-care payments company Waystar Technologies.

Reddit’s most loyal users were able to buy 8% of the shares at the IPO price, an opportunity typically reserved for institutional investors, and saw a total return in the aggregate of about $29 million by day’s end.

Reddit’s more than two-year slog to listing reflects the ups and downs of the market, beginning with its initial confidential filing in 2021 when IPOs on US exchanges set an all-time record of $339 billion.

Reddit’s listing pushes the total raised by IPOs via US exchanges this year to about $8.8 billion. That’s an increase of around 152% at this point in 2023.

One benefit of Reddit’s slow route to the public market is that enthusiasm for the AI revolution has continued to mount.

The potential of AI was at the center of Reddit’s proposed value proposition to investors, as companies eye the record-setting rallies in stocks like chipmaker Nvidia Corp.

Pay for growth, and for Reddit, which accelerated growth in the past six months, it just makes a strong case that it should be at a premium multiple.

Reddit said it’s in the early stages of allowing third parties to license access to data on the platform, including to coach up artificial intelligence models.

The company said that in January it entered into data licensing arrangements with an aggregate contract value of $203 million and terms ranging from two to three years. It expects a minimum of $66.4 million of revenue from those agreements this year, according to the filings.

Reddit also has announced a deal with Google, allowing Google’s AI products to use Reddit data to improve their technology. Large language models often need vast troves of human-generated content to improve.

Founded in 2005, Reddit averaged 73.1 million daily active unique visitors in the fourth quarter, according to its filings. The company reported a net loss of $91 million on revenue of $804 million in 2023, compared with a net loss of about $159 million on revenue of $667 million a year earlier.

It’s clear to me that there is a solid road map to monetizing Reddit’s platform whether it is licensing in-house data for AI large language models.

Reddit is an extremely rich and diverse social platform in which contributors discuss many topics.

As long as the over 73 million subscribers maintain their engagement, it’s easy to see how the tech company maintains its growth trajectory.

I do believe that subscriber growth will continue and the low-hanging fruit is that 100 million subscriber numbers.

Over time, this platform is a gold mine for AI algorithms to integrate with and that shouldn’t be diminished.

I would invest long-term only on big dips.