Mad Hedge Technology Letter

March 11, 2024

Fiat Lux

Featured Trade:

(MICROSTRATEGY STRATEGIZES TO PROFITS)

(MSTR), ($BTC)

Mad Hedge Technology Letter

March 11, 2024

Fiat Lux

Featured Trade:

(MICROSTRATEGY STRATEGIZES TO PROFITS)

(MSTR), ($BTC)

There has been one tech company that has tied its fortunes directly to the price of Bitcoin ($BTC) and that is MicroStrategy (MSTR).

Gutsy is a word that would describe this direction, and some would even say it’s full out irresponsible.

The daring company has had to deal with fallout when bitcoin crashes and it was brutal in the PR world.

Yet as Bitcoin soars in price today, the co-founder of MSTR Michael Saylor should take a victory lap.

Saylor was on the receiving end of a great deal of scorn and criticism as Bitcoin tanked to $15,000 per coin.

Now the company is levering up some more to go bigger.

MSTR bought another 12,000 Bitcoin for $821.7 million, the second-largest purchase by the enterprise software maker since it began acquiring the cryptocurrency almost four years ago.

The fresh hoard raised MicroStrategy’s total Bitcoin holdings to around 205,000 tokens, or to more than $14 billion.

Saylor started buying Bitcoin in 2020 as an inflation hedge and alternative to holding cash. MicroStrategy has already spent more than $1 billion in Bitcoin in the first three months of 2024, more than half of last year’s total buying. The cryptocurrency is up around 675% since Saylor began buying.

The shift into Bitcoin has led to a revival in the share price of MicroStrategy, which has surged more than 1,000% since Saylor’s pivot.

The company’s market capitalization has increased to around $25.7 billion, topping the level that it previously peaked at in March 2000. MicroStrategy reached a settlement in December 2000 with the SEC over accounting fraud allegations.

The average price for the total holding is $33,706, according to the filing. Bitcoin reached a record high of more than $72,000.

The company also presides over a real software business and they believe that the combination of an operating structure including a bitcoin strategy will succeed.

MSTR’s focus on technology innovation provides a unique opportunity for value creation.

Being an operating company, MSTR’s software business remains a core revenue and cash flow generator.

In addition, it also enables them to acquire bitcoin through the use of excess cash or proceeds from equity capital raises or corporate debt capital raises and to pursue software innovations that leverage the bitcoin blockchain.

They’ve deployed these levers to increase bitcoin holdings in a manner that has created shareholder value.

Bitcoin development includes its Bitcoin acquisition strategy and Bitcoin advocacy initiatives.

MSTR’s software development includes BI, AI, Cloud, or Bitcoin and Lightning-related software development.

In 2024, they are hell-bent to shift focus to grow in AI plus BI, while accelerating a sharp transition to a cloud-centric operating model.

Key strategic goals are to grow cloud, innovate with AI, and increase profitability.

In December, they successfully deployed Google Cloud platform integration, furthering multi-cloud capabilities, and providing greater optionality to their customers.

I won’t say that MSTR’s software and cloud business will compete with the Silicon Valley Magnificent 7, but its existence is to support a risky Bitcoin strategy which is actually working effectively as we speak.

Sometimes risky bets pay off well.

Shares in this company will either skyrocket or go to zero depending on what Bitcoin does.

Mad Hedge Technology Letter

March 8, 2024

Fiat Lux

Featured Trade:

(APPLE NEEDS TO UP ITS GAME)

(CRWD), (PANW)

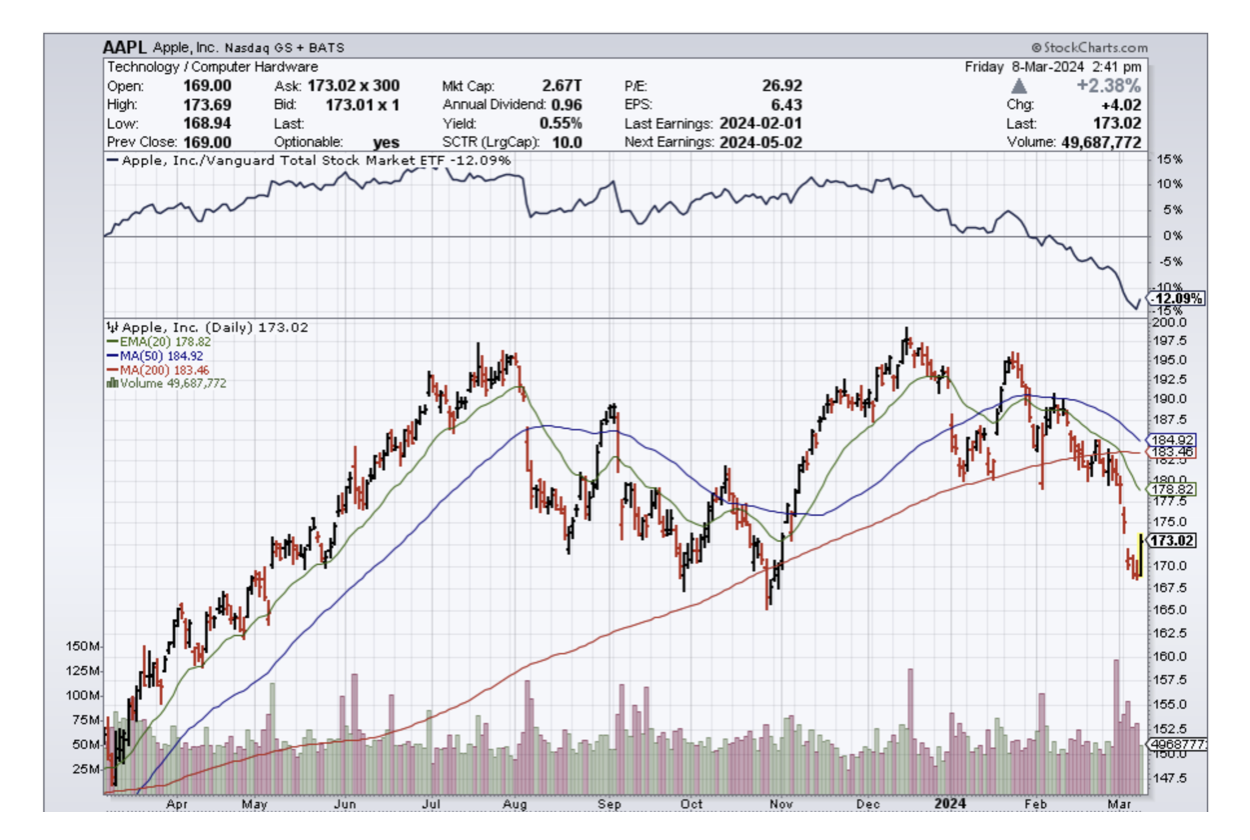

It’s no longer Apple’s world.

Times have changed.

Management at Apple including CEO Tim Cook need to get with the times or else they risk being left behind.

Large existential risks aren’t only felt by Apple, most of the tech sector risk being left behind by the AI bandwagon.

If there was any inkling that I might be wrong about this then explain the latest data point about Apple’s lackluster sales in Asia.

Sales of Apple’s iPhone plunged in China by 24% year over year as Apple faced stiff competition from local smartphone firms like Huawei, Oppo, Vivo and Xiaomi.

Apple came under particular pressure from Chinese tech giant Huawei, whose consumer business is experiencing a resurgence in China after the launch of its Mate 60 smartphone.

Several rival Chinese smartphone companies also logged drops in their unit sales in the six-week period, but the declines were less pronounced than that of Apple.

The best-performing smartphone brands for the first six weeks were Huawei and its spinoff Honor, which branched out of the tech giant in 2020 as a result of U.S. sanctions.

Huawei smartphone unit shipments rose 64% year over year in the first six weeks of 2024.

Apple is facing a backbreaking environment in its cash cow China.

Local Chinese smartphone makers have caught up and make a pretty nice version of a smartphone comparable to the iPhone including a reinvigorated Huawei.

Customers flocked to iPhones, once Huawei’s phones lost their competitiveness due to the lack of 5G and no cutting-edge semiconductors.

Losing the China market is a big blow to Apple’s management as deglobalization picks up speed.

Even more worrying is why isn’t Apple hopping on the AI bandwagon?

They risk being left behind as the “iPhone company.”

It’s not emerging as one of the largest risk to Apple’s strategic future.

They did well with last generation’s technology, but they look gradually misplaced for the next round of technological modernizations.

I haven’t heard much of what they are doing in AI, and they had to fire their team that worked on the Apple car.

No doubt that Apple shareholders are starting to question what management has up its sleeves and before it was ok to return to the well with iPhone sales growing.

However, we have clearly entered a paradigm shift where the iPhone well has run dry and shareholders are expecting more.

If Tim Cook can’t figure it out then large investors like Warren Buffett could start to unload shares in batches which could demoralize the stock in the short-term.

For now, I do believe Apple is worth a trade to the upside because it’s so beaten down.

It shocking that we have gotten to this point with Apple, but tech companies are all at risk of extinction unless they evolve with the times.

For the first time in a long time, it’s right to question whether to hold Apple shares for the long haul.

“Technology is nothing. What's important is that you have a faith in people, that they're basically good and smart, and if you give them tools, they'll do wonderful things with them.” – Said Steve Jobs

Mad Hedge Technology Letter

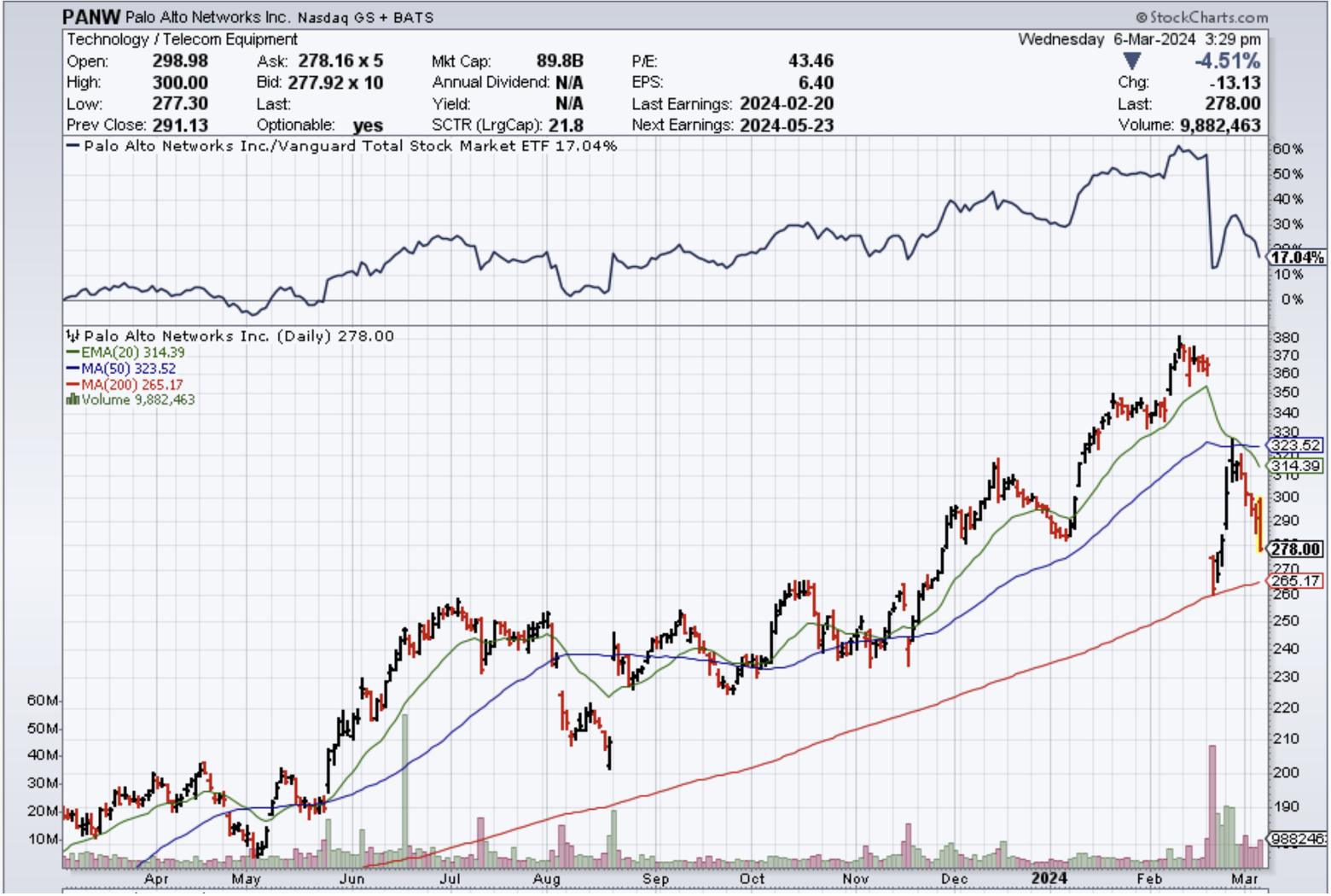

March 6, 2024

Fiat Lux

Featured Trade:

(CYBER SECURITY IS STILL GROWTH)

(CRWD), (PANW)

Since starting the company, CrowdStrike (CRWD) has brought cybersecurity to the cloud.

They have pioneered AI for cybersecurity, and quickly become the de-facto security platform that disrupts, displaces, and consolidates other vendors.

This stock has been really good to Mad Hedge Tech Letter followers, and we recently took profits in a successful in-the-money bull call spread in CRWD.

Money will flow into enterprise protection as the stakes get higher with hackers looking to strike gold.

When talking about the threat landscape, CrowdStrike pioneered commercial threat intelligence that governments and companies of all sizes depend on.

It's CrowdStrike that delivers billions of new threat detections every month to stop breaches.

It's CrowdStrike that is the search bar of security, where security analysts complete millions of queries daily.

What took hackers hours, has shrunk to minutes and seconds. Attack speeds will only accelerate.

The cloud is increasingly under attack and CRWD exists to protect businesses against these attacks.

CRWD tracked a 75% year-over-year increase in cloud intrusion attempts.

The cloud is today's battleground for cyberattacks.

Generative AI is an adversary force multiplier and the last few years have seen the onboarding of this new force multiplier.

Gen AI puts advanced cybercrime tradecraft in the hands of attackers of all skill levels. Gen AI will dramatically grow the adversary population.

CRWD collects trillions of threat signals daily, creating one of the world's largest and fastest-growing cyberthreat datasets.

From day one, CRWD has been an AI company, training the industry's most effective and accurate AI models to prevent attacks based on data mode.

Embedded in the Falcon platform is a virtuous data cycle where CRWD collects cybersecurity's very best threat intelligence data, builds, and trains robust preventative and generative models, and protects CRWD customers with community immunity.

In today's environment of heightened cyberattacks, the latest SEC breach disclosure regulation only increases the pressure on companies and their boards.

One of the best of breeds and its superior performance are a critical reason to why the share price has moved up in the last few years.

Let’s look at the numbers behind the business model.

Moving to the P&L, total revenue grew 33% year over year to reach $845.3 million.

Subscription revenue grew 33% over Q4 of last year to reach $795.9 million. Professional services revenue was $49.4 million, representing 26% year-over-year growth.

Subscription customers were five or more, six or more, and seven or more modules growing to 64%, 43%, and 27% of subscription customers, respectively.

CRWD is landing bigger with new customers on average adopting 4.9 modules out of the gate, an increase over last year. CRWD’s gross retention rate remained high at 98%.

CRWD is knocking it out of the park.

It’s hard to maintain growth company status in the head of major macro headwinds.

Many enterprise businesses are pulling back spend, but cybersecurity hasn’t been curtailed as of yet.

Tech companies are becoming more efficient and cybercrime hasn’t felt the pain of leaner software budgets.

This bodes well for the future of cyber security and the main players in the industry.

Mad Hedge Technology Letter

March 4, 2024

Fiat Lux

Featured Trade:

(MIDDLE MANAGERS ON THE CHOPPING BLOCK)

(NVDA), (SMCI)

Sure, the narrative out there is that generative AI will transform the technology sector and the companies that coalesce around it.

That doesn’t always mean it will be great for everyone.

Many jobs can be mundane and boring.

AI is supposed to solve all that by unlocking time for these workers to do other tasks.

However, one trend that is picking up speed that could turn into a runaway freight train is the evolution of AI destroying most of the human job market.

It’s happening faster than people think.

If everyone loses their jobs except for a handful of CEOs running a company with AI, who will pay rent to small or corporate landlords?

Who will partake in a trip to a sports bar when these patrons lack salaries that are replaced by AI.

The next battleground of AI job removal is now reaching up to the middle manager echelon.

Confidence among middle-managers dropped to its worst-ever reading in February, pushing a broader index of US employee sentiment down to a record low.

The group’s confidence is now similar to that of entry-level workers, which fell last month to the lowest in seven years.

Decades after automation began taking and transforming manufacturing jobs, artificial intelligence is coming for the corporate management.

The list of white-collar layoffs is growing almost daily and includes jobs cuts at Google, Duolingo and UPS in recent weeks.

While the total number of jobs directly lost to generative AI remains low, some of these companies and others have linked cuts to new productivity-boosting technologies such as machine learning and other AI applications.

Generative AI could soon upend a much bigger share of white-collar jobs, including middle and high-level managers,

Generative AI speeds up routine tasks or make predictions by recognizing data patterns.

It has the power to create content and synthesize ideas—in essence, the kind of knowledge work millions of people now do behind computers.

Across all ranks, employee confidence fell to 45.1%, the lowest in data back to 2016.

Middle managers have to both direct more junior employees and answer to the senior ranks, making the position uniquely prone to burnout in the corporate ladder.

Tech firms like Meta and Google zoned in on those positions for cuts last year.

In announcing the job cuts, the companies cited similar themes around productivity and efficiency.

At some big tech firms, that can be gauged by how many people work under you, providing an incentive to overdo the staffing levels.

Companies that did just that are increasingly reducing staff and driving confidence down with it.

Although highly positive for revenue estimates, human workers will need to adjust to a modern cutthroat working environment where they need to do more and get paid less in technology.

The ironic thing about this is that the very technology they lusted over is the same technology putting the same workers out of a job.

Better be careful what you wish!

At a stock market level, this is highly positive and will lead to higher shares in tech companies like Nvidia and Super Micro computers.

Remember that wages are usually the highest expense and reducing them will almost always result in higher share prices.

It’s good that low confidence doesn’t affect the execution or existence of AI.

This is significantly bullish tech stocks short and long term and I expect every quarterly earnings transcript to talk about reducing staffing levels and higher efficiency.

“The way to build billion dollar companies is to first build something people love.” – Said CEO of OpenAI Sam Altman