Mad Hedge Technology Letter

February 12, 2024

Fiat Lux

Featured Trade:

(THE AI WAR STOCK)

(PLTR), (SMCI), (NVDA)

Mad Hedge Technology Letter

February 12, 2024

Fiat Lux

Featured Trade:

(THE AI WAR STOCK)

(PLTR), (SMCI), (NVDA)

Palantir’s (PLTR) performance in the US is nothing short of extraordinary, and some would even say scintillating.

I’ll tell you why.

The numbers on the screen make you giggle like the 70% year-on-year growth in Q4.

It’s almost inconceivable to do what they did and I am referring to signing that many contracts given the way the product is.

We are witnessing a convergence of Palantir’s software products becoming easier to use which is leading to an augmentation of its capabilities, both driven by developments in AI, and large language models.

The heightened demand and ability to meet that demand is something Palantir’s management calls “with a pilot.”

This new piloting approach is what they call boot camp.

They did over 500 boot camps last year.

Palantir’s management travels around the country now convincing CEOs, CTOs, CFOs, and really, whoever has $1 million to buy the software and transform their enterprise by harnessing everything achieved in AI since inception and putting the best people on it.

Palantir then coaches these best employees on how to run data at a boot camp for 10 hours per day until they know it like the back of their hand.

One unique part of Palantir’s business model is their principle of making it known that they are proud of their work on the war front. They are proud to support the US.

Specifically, they are proud to support the US military.

However, this has rubbed some the wrong way like the Europeans who refuse to do much business with PLTR.

PLTR has been unable to make inroads across the Atlantic.

Yet PLTR is proud to have carved out a pivotally crucial role not only in Ukraine, but management is proud that after October 7, within weeks, Palantir is on the ground, and is involved in operationally crucial roles on the software side in Israel.

I know of no other software company in the world that is at the focal point of Ukraine and Israel and it is important for investors to know this before they decide to invest in the company.

This tech company boards the most talented, interesting, and performance-based people in the world.

Some of the numbers that can’t just be ignored are the 55% growth in customer count year-over-year.

This is the early days of generative AI in software products and for Palantir to describe the rocket fuel growth they are experiencing backs up the AI narrative.

For better or worse, the sector is relying on the AI pixie dust to carry the rest of the tech market.

As soon as the market gets wind that AI-based growth isn’t supercharging balance sheets, the tech sector will pull back.

Therefore, it’s highly positive for technology momentum to see stocks like PLTR and chip stocks like Super Micro Computer (SMCI) hit a home run in earnings.

Sadly, Nvidia (NVDA) can’t just carry the load for the entire sector and there needs to be some alternative leadership from other tech stocks connected to the AI story.

PLTR has tripled in the past 365 days and I don’t believe that type of stock performance can continue in the short-term.

The last earnings beat was met with yet another impressive 20% rise in the stock price.

Investors will need to be patient and wait for the stock to pull back otherwise chasing usually ends in tears.

I would advise readers to not chase and wait for big drops in individuals' names to put money to work.

“Stock market bubbles don't grow out of thin air. They have a solid basis in reality, but the reality is distorted by a misconception.” – Said George Soros

Mad Hedge Technology Letter

February 9, 2024

Fiat Lux

Featured Trade:

(THE NEW HOT A.I. STOCK)

(SMCI), (NVDA)

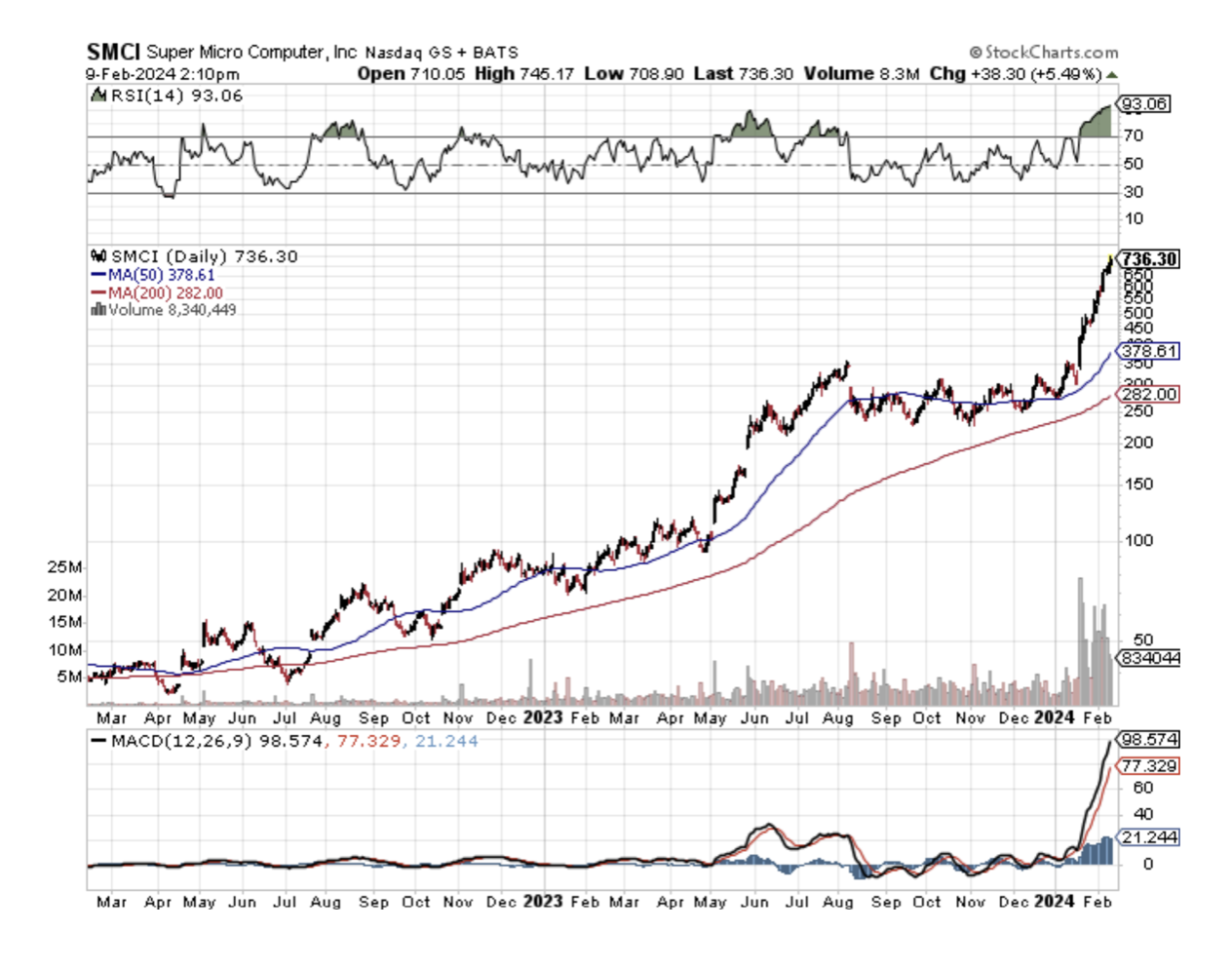

Super Micro Computers (SMCI) could be a legitimate dark horse in this race to AI supremacy.

They are the meat of the whole operation.

This is an upstart company from California who really knows their stuff about computer infrastructure.

Although they are no Nvidia, they do pack a punch and its share price has exploded higher as the company has been buoyed by both excellent quarterly results and an even better forecast for the full year.

Institutional interest is also gaining steam as the stock continues to be bid up to higher highs.

It’s proving itself, along with Nvidia, to be one of the cleanest stock plays on the AI theme.

Shares of SMCI were languishing lower than $20 per share in 2019.

Fast forward to today and underlying shares are sitting pretty at $750 per share.

Nvidia and Supermicro are somewhat correlated.

Nvidia’s high-performance chips are essential for the AI revolution, they need cutting-edge data infrastructure and that’s how Supermicro’s slots in nicely.

SMCI takes an innovative, customized, and flexible approach to meet customers’ computing needs – which has made it the choice of heavyweight clients like Meta and Amazon. SMCI supplies in rapid time, and the uber-complicated tech behind these centers, which needs servers, networks, and cloud storage solutions to function.

The company also uses a liquid cooling technique to manage the temperature of its multi-rack servers in a more energy-efficient way.

By the end of September, research firm IDC estimated that Supermicro had become the fourth-biggest server provider in the world, ahead of Lenovo.

And, sure, Dell and Hewlett Packard Enterprise are the leaders, but their revenue growth has been falling while Supermicro’s is muscling up at a double-digit pace, making it a leader in the higher-priced and higher-margin AI server market.

In its latest earnings report, SMCI announced revenues of $3.66 billion, a 133% increase from the year-earlier period, and predicted sales of at least $14.3 billion in 2024.

Supermicro’s leadership will not stay inert.

They are partnering with Nvidia, AMD, and Intel – the three biggest AI chip suppliers – on next-generation AI designs. So its customers will likely include all the big AI spenders like Meta, Amazon, Apple, and Tesla.

SMCI is forecasted to bust out an EPS growth rate of 31% moving forward.

The key risk ahead is that Dell and maybe even Hewlett Packard Enterprise might compete again with Supermicro’s capability in data centers and put its operating margins under pressure.

That could undermine the company’s profit outlook, especially if overall demand growth for data centers wavers.

The stock is expensive even to the point where short-term technical indicators have shown the stock to be overbought for the past 3 weeks.

In fact, the stock was sitting at $300 per share on January 18th and the parabolic trajectory has meant that the stock has more than doubled in the past few weeks.

Readers need to let this stock drop and any medium-sized pullback just be bought with two hands.

These types of premium AI stocks are hard to find optimal entry points which could mean a long wait time.

“What's dangerous is not to evolve.” – Said Founder of Amazon Jeff Bezos

Mad Hedge Technology Letter

February 7, 2024

Fiat Lux

Featured Trade:

(IS BABA WORTH A TRADE?)

(BABA), (PDD)

Remember when Chinese tech was supposed to topple Silicon Valley?

That was just a few years ago and it is mind-boggling how the situation has had a sudden about-face.

Chinese tech has been left twisting in the wind of mediocrity while American tech has forged through and seized the opportunity to become the best tech industry on the planet.

Some of the weaknesses are quite glaring and the most obvious one comes in the form of Chinese e-commerce company Alibaba’s 75% nosedive from a 2020 record high.

The crash has flattened its valuation to an all-time low and put its market capitalization on a par with upstart rival PDD Holdings (PDD).

Alibaba’s revenue for the three months through December only rose 5.6% from a year ago, the slowest growth in three quarters amid difficult economic conditions and steep discounting.

Forward earnings estimates for the company have fallen about 4% over the past month.

China’s online retail market is saturated and the backdrop is getting worse.

Alibaba and JD.com are the old men in the nightclub club while fresh faces like Douyin Mall, run by TikTok owner ByteDance are chomping at the bit.

At the same time, persistent deflationary pressure and declining wages have driven a price war that is being won by discounters like Pinduoduo, the local equivalent of PDD’s Temu.

Alibaba is forecasted to cede market share as they face fierce competition from rivals like Douyin and PDD.

Another focus would be whether they are able to import new drivers to maintain their overall growth.

Alibaba spent $9.5 billion on share buybacks last year, a record high.

Revamp efforts led by the company’s new management include scaling down non-core business while stepping up investment in global expansion and artificial intelligence.

It’s focusing on improving core operations, including moving resources from its Tmall site to Taobao in order to better meet demand for cheaper products, though it may take time to see results.

This focus on lower prices will lead to weaker revenue growth, which is certainly negative to near-term sentiment and share price. The company’s core business growth will likely “remain lackluster in the next four quarters.

With many things in China, this is a race to the bottom and BABA is getting a proper taste of that Chinese medicine.

Lower prices are met with even lower prices and it becomes a war of attrition.

Investors don’t like to hear that.

In the most recent earnings report, net profit declined by 77%.

Overall sales growth last quarter rose by just 3%.

This company used to be a supercharged growth company and in just a few years, they have almost been swept into the dustbin of history.

BABA stock is down today over 5% from the poor earnings report as the stage is set for BABA to hardly grow at all in the foreseeable future.

Many from Gen Z have remarked how discount e-tailers like PDD’s Temu have flooded American social media platforms with ads.

This trend has resulted in negative impacts to BABA’s staying power in e-commerce and the profit margins are in the firing line as we speak.

At $73 per share, the stock might be in for a dead cat bounce for a trade.

Long term, the stock has lost its luster and lost its mojo.

BABA shouldn’t be touched with a 10-foot pole as the entire Chinese economy goes through the motion of a slowly forming zombie corporate structure.

Mad Hedge Technology Letter

February 5, 2024

Fiat Lux

Featured Trade:

(THE NEW TECH DARLING META)

(META), (GOOGL)

Meta (META) is no joke.

They put any sense of concern to bed with its brilliant performance this past quarter.

They are the new poster child of tech as they blew away every meaningful metric that so-called analysts grade tech on.

They are even the newest dividend stock which might be the most absurd part of their performance.

Growth is their new forte and the $200 billion rise in market valuation in one day is the stuff of legends.

How did they make this happen?

Revenue jumped 25% in the quarter from $32.2 billion a year earlier, as the online ad market continued to rebound.

Meanwhile, the company’s expenses decreased 8% year over year to $23.73 billion, and its operating margin more than doubled to 41%, a clear sign that cost-cutting measures are bolstering profitability.

Net income more than tripled to $14 billion, or $5.33 per share, from $4.65 billion, or $1.76 per share, a year earlier.

Meta said it will pay investors a dividend of 50 cents a share on March 26. That comes after cash and equivalents swelled to $65.4 billion at the end of 2023 from $40.7 billion a year earlier. The company also announced a $50 billion share buyback.

Sales in Meta’s Reality Labs unit passed $1 billion in the quarter, though the virtual reality unit recorded $4.65 billion in losses.

I found it highly positive that Meta took getting lean very seriously as they really gutted staff numbers to the delight of the balance sheet.

Talking to many people in the know, META has been overstaffed for quite some time so much so that many at Meta had nothing to do all day.

The 22% year-over-year decrease in staff levels is a sign of things to come and this is just the start.

In the next few years, I do believe that Meta will shave down staff levels to what would amount to 85% less than COVID levels.

Part of Meta’s financial recovery over the past year was driven by Chinese retailers, which have increased spending to reach users across the globe.

Management said advances in artificial intelligence have helped reinvigorate the ad business, which is growing faster than rival Google’s. In Alphabet

’s earnings report Tuesday, the company said Google ad revenue increased 11% from a year earlier, a slower expansion than analysts were expecting.

Meta will continue to invest in AI and in building up its computing infrastructure.

This is the new META and they finally got all their ducks in a row.

Emphasizing what matters is what the stock wanted and they delivered in droves.

They get a green check mark for cutting costs, reducing headcount, spiking operating leverage, tripling profits, improving ad business, moving along the AI business, and delivering a new dividend.

That was just one quarter and if they can keep hammering away on these selective items, then META stock will be one of the best buy-the-dip stocks in the entire equity market.

Meta has been a stock I have wanted to get into for a while and entry points are few and far between.

The individual performance suggests that tech is stronger than first believed and might I say even cheap with all this untapped growth on the horizon.