The Big Play in Autonomous Driving with Aptiv

The conventional wisdom on Electric Vehicles (EVs) is that they are here to stay.

The secular trends of harsher government environmental policy, a healthy global economic backdrop, rapid-fire technological development, and broad-based mainstream acceptance are the catalysts that will place EVs at the apex of the digital transportation movement for the rest of this century.

EVs are set to eventually capture more than 60% of market share, forcing legacy automotive and niche start-ups to reinvest into their operations in a fiercely competitive industry.

The EV industry still has a mountain to climb as it only represented less than 1% of total global auto unit sales in 2016. That percentage has gradually risen to 1.25% at the end of 2017.

The transition to 60% EV share of total units will organically occur in a slow and steady manner giving automakers ample time to shed legacy technology.

Cost is a major obstacle for widespread EV adoption. Many consumers cannot afford one, but price efficiencies are slowly dropping the cost of owning an EV, appealing to the masses with sleeker models possessing price tags similar to normal cookie-cutter sedans such as the Tesla Model 3.

EV makers have coped with the arduous task of constructing a car within truncated cost limitations. They make up the difference by offering a proliferation of premium add-ons such as souped-up engines and glitzy interiors that extract additional marginal revenue from well-off individuals.

EV technology advancement paired together with higher emission standards will narrow the gap between electric vehicles and the legacy internal combustion engine within the next decade.

Modern EVs new to market such as the Tesla Model 3 could serve as a springboard for able consumers to dive head in to EV revolution.

The disruption time horizon will take around 15 years and affect 80% of the market.

EV mania is destined to integrate with the traditional concept of a car to give transportation breakthrough A.I. functionality, user-friendly connectivity, and self-driving capabilities.

Let's face it, it's easier to install computer systems and software in an electrified platform, and the technologies complement each other.

About 60% of autonomous, light vehicle retrofits are constructed over an electric powertrain, and an additional 21% go with a hybrid powertrain.

Thus, owning the best autonomous vehicle (AV) technology stocks positions investors for the next leg of hyper-accelerating tech.

Waymo's leadership in the AV space is frightening for Tesla, which trails the Alphabet subsidiary that smoothly rolled out its for-profit service in Arizona in early 2018.

Aptiv PLC made a massive splash in the deep-end by acquiring the second best AV technology company NuTonomy. The Cambridge, MA-based tech firm spun off from MIT in 2013, for $450 million late last year and was spun out again in 2017.

Delphi Technologies spun out its legacy and tech business into two separate companies. The legacy part of the company is now the ticker symbol (DLPH), and the AV company became Aptiv PLC (APTV).

Spin-offs give organizations the opportunity to streamline operations and allow the market to value the company on an independent basis instead of the sum of the parts. This can lead to uncorking additional shareholder value.

Aptiv is the closest thing on the market you will find for an unfettered play on self-driving technology.

Management declined against merging its legacy and AV technology, which is a smart move considering legacy technology gets the wrong rub of the green by investors.

NuTonomy lags Alphabet's Waymo but has been operating robo-taxis in Singapore since 2016. Delphi has gifted additional engineers, reinforcing its fantastic technical talent.

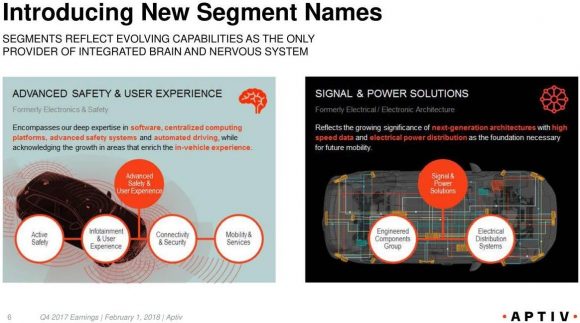

Aptiv has split its business into two new different segments in the new company.

The Advanced Safety and User experience segment will act as the brain in the vehicle, emphasizing software know-how to guarantee user security while a centralized system maintains connectivity.

The new Signal and Power Solutions segment will act as the nervous system in the vehicle by enabling high-speed data fluidity within the next-gen architecture. This segment includes the cable management and connector products that contribute a further $1 billion of revenue to the top line.

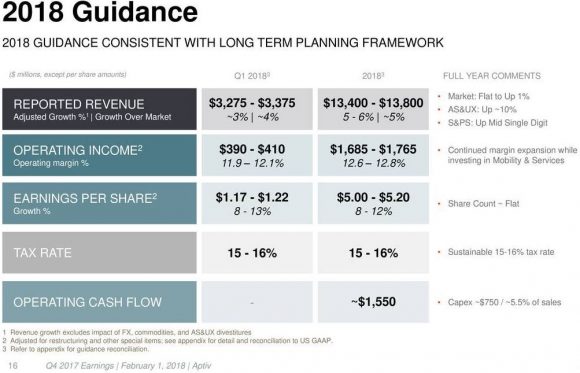

In total, Aptiv procured $12.9 billion in annual revenue in 2017, which was a boost of 4.9% from 2016. Earnings per share growth was up 10.5% YOY.

Investors cannot reasonably expect AV companies to annually grow top line by 20% to 30% as cloud companies, and the margins are unfortunately less savory. The dynamics of the business are different, and the revenue guidance of $13.4 to $13.8 billion should keep investors happy.

The pipeline is in fine fettle with $19.3 billion in bookings, which represent the lifetime gross revenue for consummated contracts.

Some of the outsized awards came in the form of an active safety contract with an OEM alliance, a high-voltage mobile charger contract from a leading North American EV producer, and an architectural contract for BYD's SUV platform in China.

It's no wonder both of the newly crafted segments expect a 10% boost in revenue for 2018.

NuTonomy is such a gem of a company that it is shocking that a large-cap tech firm declined to swoop in.

Half a billion is peanuts for such valuable and innovative technology.

Level 4 and Level 5 grade technologies are already starting to mature.

Other minor acquisitions of analytics firms Control-Tec and Movimento will initiate data monetization opportunities that effectively analyze their aggregated data then translate data into actionable profit-making opportunities.

Big data analytics are needed to decipher the path forward after compiling millions of miles of auto-robo data. And algorithms needing refinement are starving for the data, too.

A fully connected user experience will become standard in these robo-cars, and an integrated, optimized architecture is the secret sauce to commercialization of Level 4 and Level 5 automated vehicles.

Aptiv and Waymo are the only end-to-end system providers of the integrated brain and nervous system in a vehicle.

By late 2018, NuTonomy will have more than 150 Level 4 vehicles in live action.

Aptiv forecasts about $300 million in revenue from Level 4 or Level 5 AV systems by 2025.

Level 4 is practically autonomous - ready with a driver waiting to take control if need be.

Level 1, 2 and 3 revenues will mushroom to $1.8 billion per year, more than tripling from $500 million today.

Ottomatika, a Carnegie Mellon University spin-off founded in 2013, which provides software for self-driving cars, and NuTonomy are the in-house duo entirely focused on complex Level 4 and Level 5 solutions.

The shared access to the system has been set up to allow multiple teams access to the algorithms and technology that feeds through to other parts of the business.

Aptiv PLC is the perfect company to place in a buy and forget portfolio because AV monetization is still in its incubation phase.

Just as investors of pure cloud plays recently have been rewarded in spades, pure AV technology companies will be rewarded as mass rollouts of for-profit services become commonplace.

__________________________________________________________________________________________________

Quote of the Day

"The only constant in the technology industry is change." - said CEO of Salesforce Marc Benioff