The Danish Dilemma

I was having dinner with a group of Mad Hedge Fund Trader readers in Salt Lake City the other week.

One, a successful financial advisor who's been following my market calls for years, posed a question that got the whole table talking: "Between Eli Lilly (LLY) and Novo Nordisk (NVO), which horse should I bet on in this weight loss drug race?"

It's the kind of direct question I appreciate. No beating around the bush, just cut straight to the investment thesis.

And the question couldn't have come at a better time—I'd spent the previous months analyzing the shifting dynamics between these two pharmaceutical powerhouses.

For those who haven't been following the battle between Eli Lilly and Novo Nordisk closely, you've been missing one of the most fascinating corporate duels in recent memory.

The American challenger has been steadily gaining ground against the Danish heavyweight in the GLP-1 market—drugs that were originally developed for diabetes but have become blockbusters for weight loss.

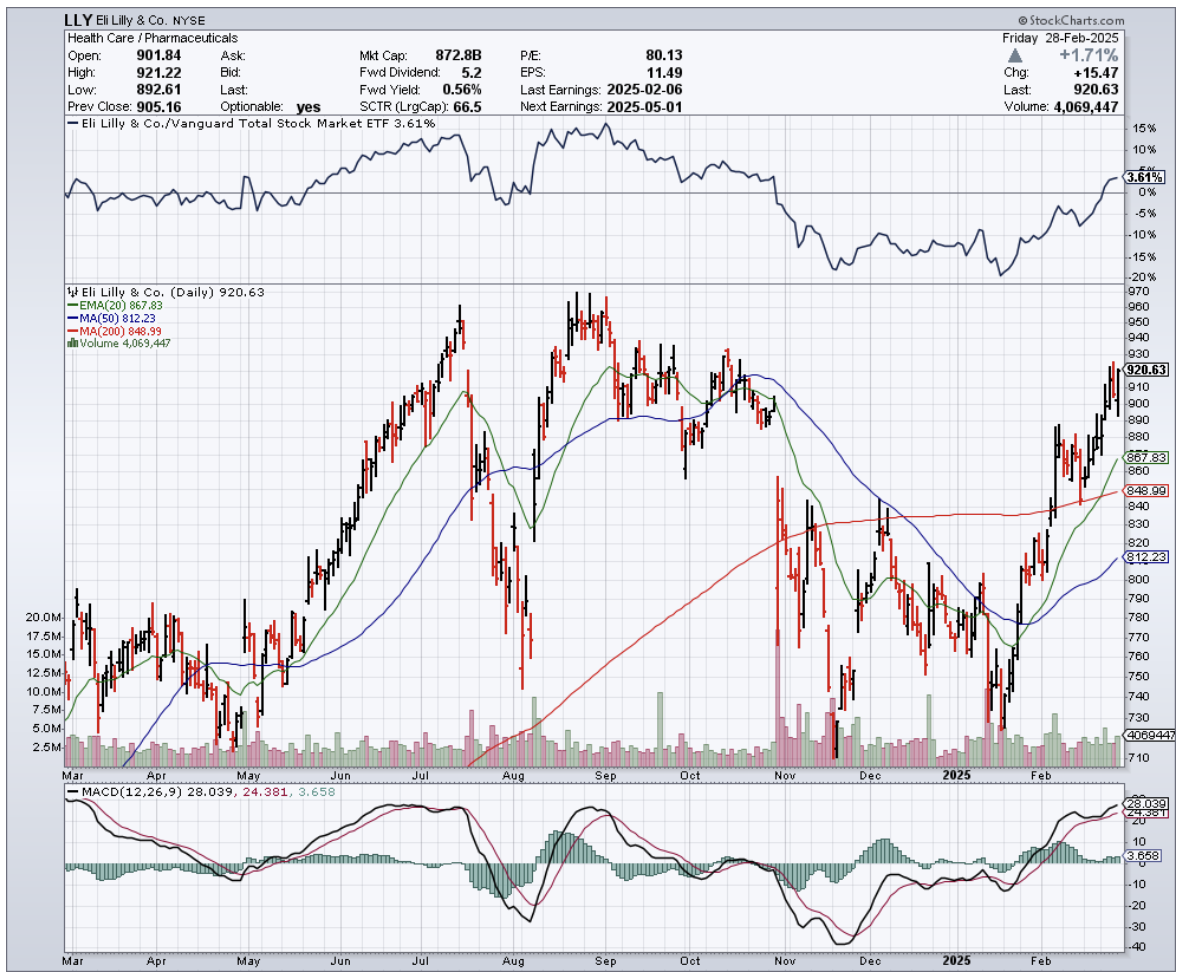

What's particularly interesting is the momentum shift that began in May 2024, with Lilly's upward trajectory continuing through February while Novo Nordisk's stock halted its precipitous decline at a critical juncture.

While bargain hunters are picking through NVO's wreckage, I'm skeptical we'll see a mass migration back to the Danish giant. Here's why.

First, there's the Trump factor. Our newly reinstalled president hasn't been subtle about demanding pharma companies shift production capacity back to American soil or face potential tariffs.

This presents a much bigger problem for Novo Nordisk than for Lilly.

The Indiana-based Lilly has a well-diversified manufacturing footprint, including substantial domestic capacity, while NVO relies heavily on non-U.S. production.

Years spent covering the White House taught me one thing: when a president threatens tariffs, smart investors listen—even if those threats haven't materialized yet.

Trump's policy shifts can come suddenly and dramatically. I've seen enough administration policy pivots over decades to know that being caught flat-footed when the music stops is a recipe for portfolio pain.

Beyond geopolitical considerations, Lilly's Zepbound (their branded weight loss medication) has been steadily gaining share in new prescriptions, showing more robust efficacy than Novo's offerings, and—in a savvy competitive move—is priced at a relative discount. It's a triple threat that's steadily eroding Novo's first-mover advantage.

But what's really impressive about Lilly's position is that they aren't putting all their eggs in the weight loss basket.

They've made solid advances in immunology and oncology, with a diverse pipeline that doesn't rely solely on incretin-based growth drivers.

This brings to mind a conversation I had with a pharmaceutical executive while flying my Ercoupe to an industry conference last weekend.

"The companies that survive long-term in this industry," he told me, "never let themselves become dependent on a single breakthrough, no matter how big."

Meanwhile, Wall Street has been revising upward its estimates for the total addressable market for weight loss drugs, anticipating expanded indications, sustained consumer adoption, and penetration into markets outside the U.S.

This strengthens the bull case for Lilly while simultaneously raising concerns about Novo Nordisk's ability to maintain its market leadership.

Speaking of market leadership, Lilly's oral GLP-1 receptor agonist Orforglipron could be submitted for regulatory approval in late 2025, potentially beating Novo's next-generation product to market.

If commercialized in 2026 as anticipated, it could further disrupt Wegovy's (Novo's weight loss drug) market position.

Some might argue that Lilly's outperformance against Novo since mid-2024 has already priced in these advantages.

But a closer look at Lilly's valuation suggests the market still isn't fully convinced of the company's growth potential.

Is this caution warranted? Perhaps. Wall Street doesn't expect Lilly's current surge in revenue growth to continue through 2027.

Lilly's management has indicated pricing will likely remain stable, but the broader expectation is that medium-term pricing may remain muted or even decline, especially as Novo's products face pricing negotiations by 2027.

This could pressure Lilly's market position, particularly given the relatively high prices in U.S. markets.

We should anticipate a more competitive landscape after 2027 as other competitors enter the weight loss drug market, though market share dynamics should remain relatively stable through 2030.

Let's talk valuation. Lilly is trading at a forward non-GAAP P/E of 37.8x, almost double its sector peers. That sounds expensive until you realize it's more than 10% below its five-year average.

More tellingly, when accounting for earnings growth prospects, Lilly's PEG ratio of 1.13 is almost 40% below the sector median.

Translation? The market hasn't gone full FOMO on Lilly yet, despite its recent outperformance of the S&P 500. In fact, price action suggests growing conviction that the stock is poised to retest its all-time highs.

Lilly weathered two setbacks in 2024 as the market questioned whether it could credibly challenge Novo's dominance.

Yet the stock found firm support above the $700 level in August, November, and again in January, confirming my belief that this support zone is rock-solid, attracting value-conscious buyers who recognize Lilly's growth potential relative to its valuation.

The breakout above the $840 zone (December highs) marks a decisive move that validates the bull case.

And while the outlook beyond 2027 remains murky, the market's restraint in valuing Lilly gives investors who've been watching from the sidelines another opportunity to board this train before it leaves the station.

"So what's your call?" pressed the advisor, who like many in his field has been forced to dump expensive research analysts while still needing solid investment ideas for his growing client base.

The rest of the table, a mix of successful entrepreneurs and self-taught traders, leaned in to hear my response.

"If you're picking between the two for a long position, Lilly is the clear choice," I replied. "They've got the edge on domestic production, they're better insulated from potential tariffs, they have a more diverse pipeline, and the market momentum is clearly in their favor."

As the waiter cleared our plates, one of the younger traders at the table asked about price targets. I tapped my wineglass thoughtfully with my pen—a habit that drives my wife crazy.

"The breakout above $840 was significant," I said. "If the fundamentals hold, which I believe they will, we could see a return to all-time highs before the bears even realize what hit them."

This led to a spirited debate about pharmaceutical valuations that lasted well past dessert.

It's these impromptu investment summits that remind me why I still travel the country meeting readers, despite having technically "retired" years ago.

The collective wisdom and diverse perspectives always sharpen my own thinking.

When the check arrived, someone joked that talking about weight loss drugs had made them lose their appetite.

“Not Lilly,” I quipped. “They're happily eating Novo's lunch”