The Incredible Bulk

Well, slap me silly and call me a contrarian. A few years back, when Eli Lilly's (LLY) market cap was under $500 billion, everyone thought it was just another faceless pharma giant on the Street.

But holy molecule, Batman! Today, Lilly isn't just knocking on the door of the trillion-dollar club—it's about to blow it off its hinges. Let's dive into Lilly's Q2 2024 earnings, shall we?

Revenue? Up 36% year-on-year to $11.3 billion. Operating income? Nearly doubled to $3.72 billion. Net income? $2.97 billion, up 86%. EPS? $3.28 on a GAAP basis, or $3.92 if you like your numbers massaged.

Now, I've seen more bubbles pop than a kid with a roll of bubble wrap, but this isn't froth - this is rocket fuel.

Lilly's guidance for 2024 is now $45.4 billion - $46.6 billion in revenue. That's $3 billion more than they were projecting a few months ago. Talk about sandbagging.

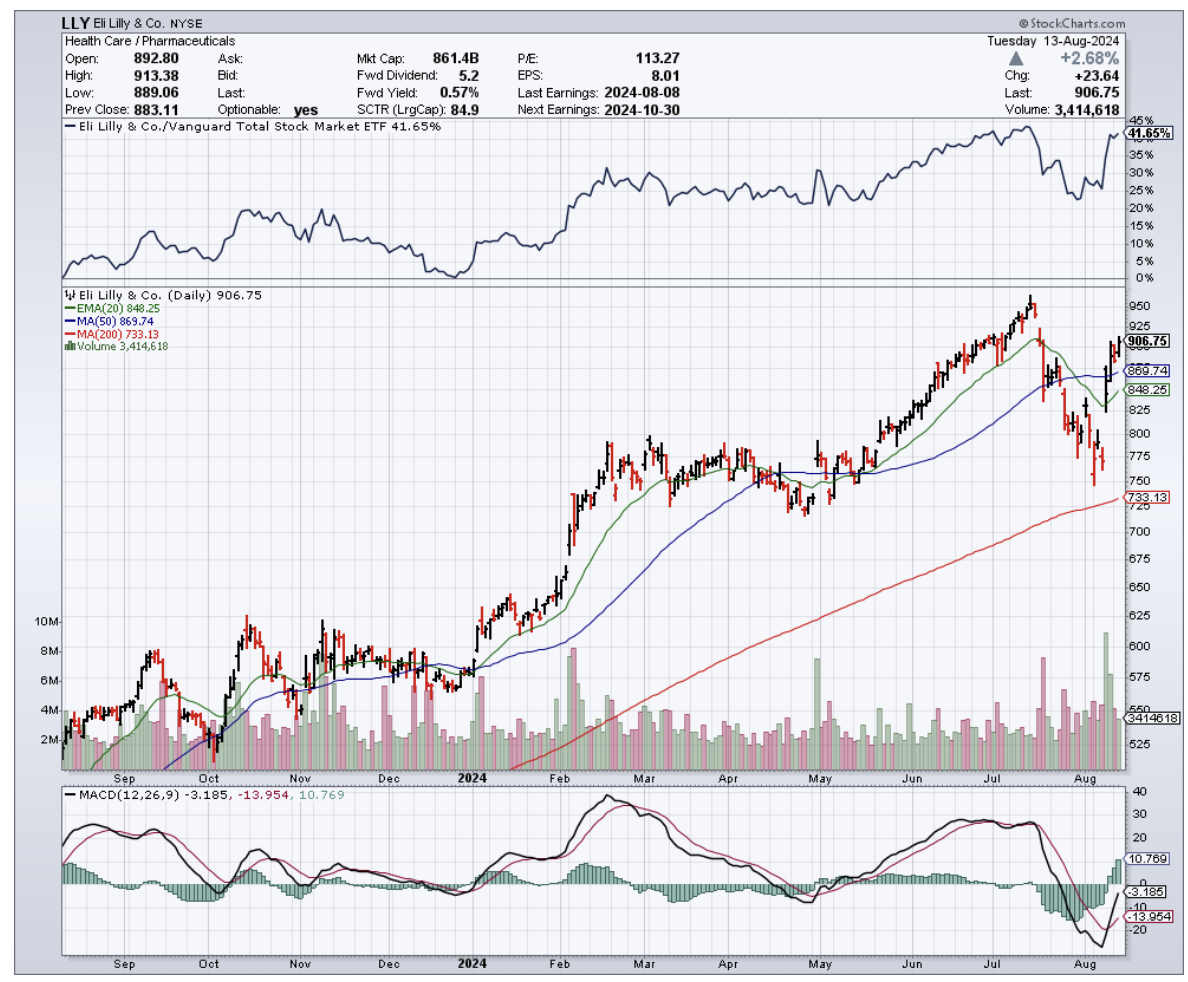

No wonder Lilly's share price has shot up 18% in the past few days.

Next, let's take a look at what’s driving this growth: tirzepatide, which is marketed as Mounjaro for diabetes and Zepbound for obesity.

In Q2, Mounjaro raked in $3.1 billion, up from $1.8 billion in Q1. Zepbound, which only hit the market in November, brought in $1.24 billion, more than doubling its Q1 performance.

Combined, that's $4.34 billion in a single quarter from one molecule. To put that in perspective, that's more than some entire countries' GDPs.

But Lilly isn't a one-trick pony. Let's take a quick tour of their other divisions.

Oncology grew to $2.16 billion, up from $1.67 billion last year, largely thanks to breast cancer therapy Verzenio.

This drug could hit $5 billion in sales this year, putting it firmly in blockbuster territory. Not bad for a drug that doesn't even cure baldness.

Immunology saw Taltz and Olumiant bring in $825 million and $228 million, respectively.

With mirikizumab finally approved last October and lebrikizumab likely to overcome its manufacturing hiccups, this division could double in size by decade's end.

It's like watching a caterpillar turn into a butterfly, if butterflies were worth billions of dollars.

Even neuroscience, which saw a dip to $339.5 million from $387.2 million last year, has a potential game-changer up its sleeve.

Donanemab, now approved as Kisunla for Alzheimer's, could bring in $5 billion annually.

Add in remternetug, another Alzheimer's therapy in the pipeline, and we could be looking at a $10 billion per year business by 2030.

That's a lot of people remembering where they left their keys.

Now, I know what you're thinking. "So, what’s the catch?" Well, you're not wrong to be skeptical. This is pharma, after all, and things can go south faster than a New Yorker fleeing to Florida for tax reasons.

The main risk? Competition. Every pharma company worth its salt is working on GLP-1 agonists.

Novo Nordisk (NVO) is already in the game with semaglutide (Wegovy and Ozempic), and others like Roche (RHHBY), Amgen (AMGN), and Pfizer (PFE) are nipping at Lilly's heels.

There's also the possibility of long-term side effects we haven't seen yet, or the risk that the healthcare system buckles under the weight of demand for these pricey drugs.

After all, we're talking about drugs that cost more per year than a decent used car.

But here's the thing: Lilly has a massive head start. They're not just leading the race – they're lapping the competition.

And they're not resting on their laurels either.

They've got orforglipron, an oral GLP-1 agonist, in Phase 3 trials. Then there's retatrutide, nicknamed "triple-G," which has shown even more impressive weight loss results than tirzepatide.

So, where does this leave us? Well, I expect Lilly to become the first trillion-dollar pharma company. Yes, you read that right. A trillion dollars.

Is their valuation justified? Based on current numbers, probably not.

But we're not betting on current numbers, we're betting on the future. And let me tell you, Lilly's future is dazzling.

Remember, just a few years ago, a $20 billion-a-year drug was considered the pinnacle of pharma success.

Tirzepatide could blow past that mark before the decade's out. And that's just one drug in Lilly's impressive arsenal.

Of course, there's always the risk that another company could swoop in with an even better GLP-1 agonist. My money's on Roche, Pfizer, or Viking (VKTX) if anyone's going to pull it off.

For now, though, Lilly's the thoroughbred in this race, and I wouldn't bet against them unless I suddenly developed a burning desire to live in a cardboard box.

That being said, predicting where this wild market is heading? That's like trying to catch lightning in a bottle while blindfolded and riding a unicycle.

But in the case of Lilly, I think even a blind squirrel could see this nut coming.

So, strap in because it’s going to be one hell of a ride, and this particular acorn might just grow into the mightiest oak on Wall Street. You wouldn’t want to miss out on the shade it'll provide in the years to come.