The King's Speech

Warren Buffett once said, “Time is the friend of the wonderful company.” If that's true, Abbott Laboratories (ABT) must be Father Time's BFF because this centenarian healthcare heavyweight has been befriending our wallets for longer than most of us have been alive.

First things first: Abbott's not just any dividend stock. It's a bona fide Dividend King, having hiked its payout for over 50 consecutive years. But let's not get too misty-eyed about history.

What's got my attention is Abbott's current form. This isn't your typical sleepy pharma stock. Abbott's been flexing its muscles across multiple segments, showing growth that could very well be a worthy competition against any Silicon Valley startup.

In the first half of this year, Abbott saw positive growth in all but one segment. The laggard? Diagnostics, which took a hit as COVID-19 testing went the way of the dodo. But hey, you can't win 'em all, right?

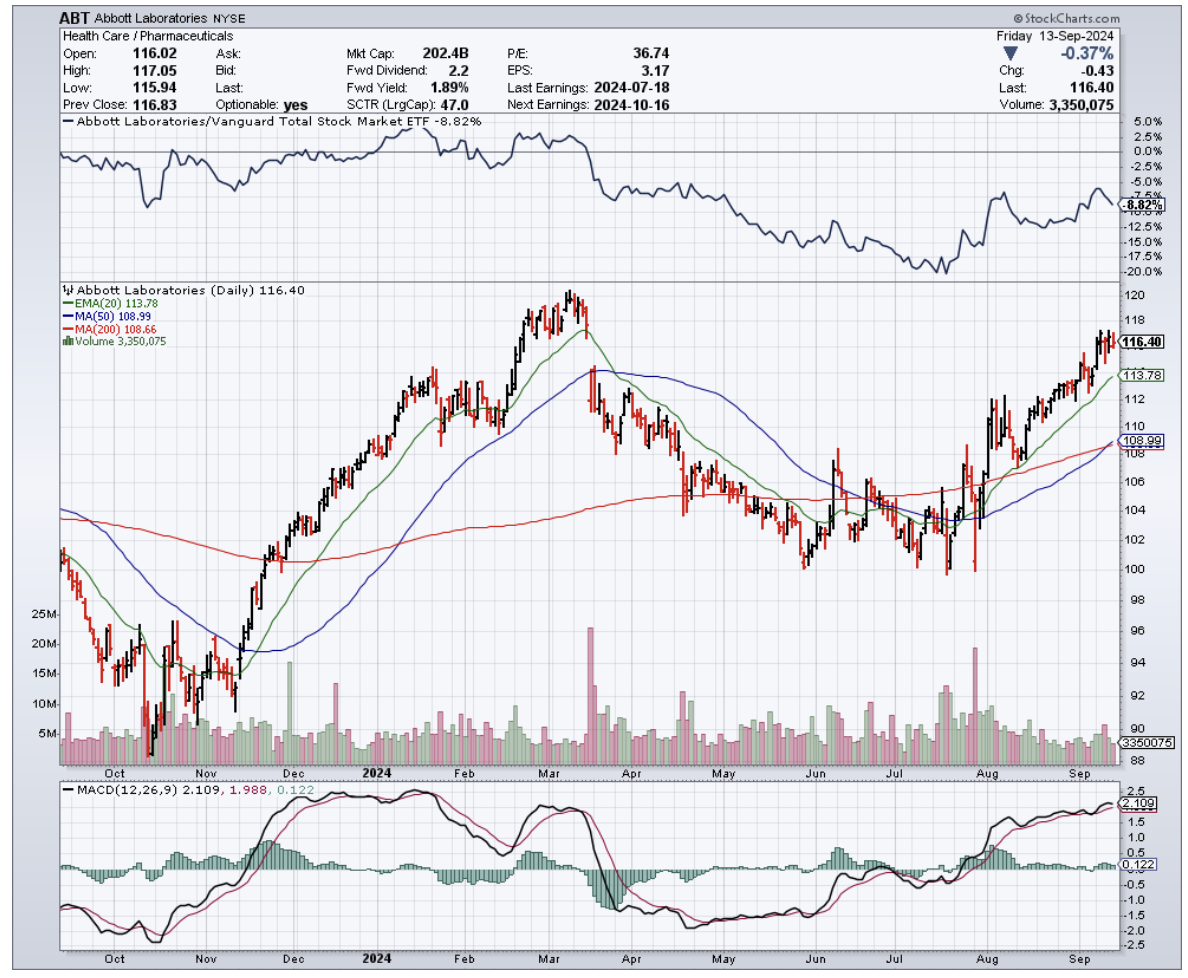

Now, let's talk dividends. Abbott's currently yielding a respectable 1.9%, outpacing the S&P 500's measly 1.3%. With a payout ratio of 67%, there's still room for this dividend to grow.

But where's the real excitement? Two words: diabetes care.

Abbott's continuous glucose monitoring devices are hotter than a two-dollar pistol, driving 19% organic growth in the first two quarters. With diabetes becoming a bigger epidemic than we anticipated, this could be Abbott's golden goose.

Just look at the skyrocketing stocks of diabetes-focused companies like Eli Lilly (LLY) and Novo Nordisk (NVO). Different products, same lucrative market.

Abbott's FreeStyle Libre CGM system isn't just some gadget. It’s actually a genuine life-changer that's raking in $1.6 billion in quarterly sales and growing 20% year-over-year. In a market where DexCom (DXCM) is nipping at their heels, that's no small feat.

But Abbott's not resting on its laurels. They're expanding into over-the-counter CGM systems like Lingo and Libre Rio, leveraging a decade of international experience to capture more U.S. market share. It's like they're aiming to slap a diabetes monitor on every wrist in America.

And here's the kicker: the number of people living with diabetes is projected to hit 643 million by 2030 and a whopping 783 million by 2045. If that’s not the definition of a growing market, then I don’t know what is.

But Abbott isn't a one-trick pony. While they're busy trying to corner the diabetes market, they're also cooking up a storm in other areas.

Take their cardiac care lineup, for instance. Abbott's dabbling in electrophysiology with their EnSite X EP System, equipped with something called Omnipolar Technology. Sounds like something out of a sci-fi flick, right? Well, it's making cardiac mapping more precise than a Swiss watchmaker, giving arrhythmia patients a fighting chance.

But that’s not where it ends. Abbott's TriClip system is tackling tricuspid valve repair like a pro wrestler pinning an opponent. And don't get me started on their Esprit dissolvable stent. It's like the James Bond of the vascular world - it does its job and then disappears without a trace.

So, while diabetes care might be Abbott's current chart-topper right now, they've got a whole album of potential hits in the works. From glucose monitors to heart repair, Abbott's making moves that could have investors' portfolios beating as steadily as a healthy heart.

And as for you nervous nellies out there, Abbott's beta value of 0.7 suggests it's more stable than a three-legged stool. Perfect for those of you who break out in hives at the mere mention of volatility.

Now, it hasn't all been smooth sailing. Abbott recently faced a trial over claims its preterm infant formula caused a dangerous disease. But don't start panic-selling just yet.

JPMorgan and Barclays reckon the liability is likely to be smaller than a gnat's appetite. Abbott's management is confident, too, probably because the product in question accounts for a whopping... wait for it... $9 million in revenue. That's pocket change for a company like Abbott.

Looking ahead, Abbott's firing on all cylinders. They're seeing 9.3% organic revenue growth (excluding their COVID products), and they're so confident they've raised their full-year guidance.

Meanwhile, valuation-wise, Abbott's looking pretty good. With double-digit earnings growth expected and an AA-credit rating (better than some countries I could name), this stock could easily outperform the market.

So, what's the bottom line? Abbott's got the stability of a Dividend King, the growth potential of a tech startup, and more irons in the fire than a blacksmith's shop.

It's trading at a fair price, and with its track record of innovation and dividend growth, this could be your ticket to a healthier portfolio. After all, in the race for returns, slow and steady often wins more than just participation trophies. I suggest you buy the dip.