The Market Outlook for the Week Ahead, or Is History Repeating Itself?

In 1919, President Woodrow Wilson traveled to Europe to negotiate the end of WWI and the Versailles Treaty. Midway through the talks, he suffered a major stroke and was hustled back to the US in an American battleship, the USS George Washington.

The Spanish Flu pandemic was underway, killing millions, so it was thought best to keep the whole matter secret. The president’s wife essentially ran the country for the last three years of Wilson’s administration, claiming to represent the president’s wishes.

This was the history that flashed through my mind when I learned of President Trump’s Covid-19 infection on Thursday night. The presidential election is now effectively over. All fundraising has ceased. It is now an open question whether Trump can even live until the November 3 election. He is, after all, a high-risk patient. Any remaining public campaign events on which the president thrived is out of the question.

The minute the president got sick, media coverage has been wholly devoted to Covid-19. That was not in the Trump plan. Not at all.

The London betting markets soared from a 60% chance of a Biden win to 90% minutes after the Covid-19 news broke. The only question is the extent of the landslide. This election won’t go anywhere near the courts or the Supreme Court, as the stock market has been pricing in. If there is another big gap down, you should be picking up stocks by the bucket load as fast as you can.

Fund managers who thought Trump had a chance of returning will spend this weekend pouring over Biden’s economic policies. All investment decisions will now be made based on the assumption that these will be the policies in force for the next 4, 8, or 12 years.

Think:

higher taxes

more economic stimulus

big infrastructure spending

more quantitative easing

grants to state and local municipalities

no inflation

low-interest rates

more alternative energy subsidies

the return of the Paris Climate Accord

more regulation of the oil industry

end of the trade wars

rejoining the NATO alliance

Oh, and the huge technological advancements and the burgeoning profit opportunities that have emerged in response to the pandemic? We get to keep those.

That is great news for long-term investors. All of this combined is very pro-investment and pro stock market. It firmly solidifies my own Dow target of 120,000 in a decade and another Roaring Twenties and coming American Golden Age. Now, we even have the trigger.

That explains why the market made back a hefty 500 points in hours, even turning positive on the day for a few fleeting moments. On a six-month view, the upside risks are far greater than the downside ones. An S&P 500 of $3,500-$3,700 by yearend is within range, up 6%-12% from here.

The September Nonfarm Payroll Report bombed, coming in at 661,000, well below expected. The headline Unemployment Rate is at a historically high 7.9%. The U-6 real “discouraged worker” jobless rate is at 12.6%. Leisure & Hospitality was the big winner at 318,888, Healthcare gained 107,000, and Retail posted 142,000. Local Government lost a staggering 232,000 jobs and towns run out of money.

US Q2 GDP came in at a horrific negative 31.4% in the final read, the worst in US history. It’s a tough economic record to run for office on. The first Q3 GDP read will not be released until October 29, five days before the presidential election, and should be up huge.

US Capital Goods hit a six-year high, up 1.8% in August. July was revised upward as well. The boost may be short-lived as stimulus money runs out.

Office Rents won’t recover until 2025, says commercial real estate leader Cushman & Wakefield. Some 215 million square feet of demand has been lost due to the pandemic. Many knowledge-based workers are never coming back to the office.

Pending Homes Sales hit a record high in August, up a mind-blowing 8.8% from July and a staggering 24.5% YOY. Hot housing markets are seeing 11%-20% YOY price increases. The northeast saw the biggest gains. This trend has another decade to run. Buy before they run out of stock.

Case Shiller rose 4.8% in July as its National Home Price Index shows. Phoenix (9.2%), Seattle (7.0%), and Charlotte (6.0%) were the price leaders. A stampede to the suburbs fueled by record-low interest rates is the main driver. Look for these trends to continue for years.

Consumer Confidence soared in September, from 84.8 last month to 101.8. Those who have money are spending it. Those who don’t are waiting in lines at food banks, disappearing from the economy. New York bankruptcies surged 40%. If you haven’t spent the past decade investing in your online presence or yourself, you’re toast.

Disney (DIS) laid off 28,000 to stem hemorrhaging losses at its theme parks, hotels, and cruise line. It will take a year to come back. Clearly, their recent $78.3 billion purchase of 21st Century Fox movie and TV studios last year was poorly timed, just before the pandemic, and they borrowed massively to close it. And they had a major presence in China! It’s one of the biggest mass layoffs since Corona began to decimate the economy.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old.

My Global Trading Dispatch pushed through to a new all-time high last week on the strength of a position that I kept for a single day. All I needed was the 700-point dive in the Dow Average in 24 hours to realize half the maximum profit in my short (SPY) position. When the market offers me a gift like that, I take it, no questions asked. I am back to a rare 100% cash position, waiting for a bigger dump to buy.

The risk/reward in the market now is terrible. I believe we have to test the 200-day moving averages before it’s safe to go back in with the indexes and single stocks.

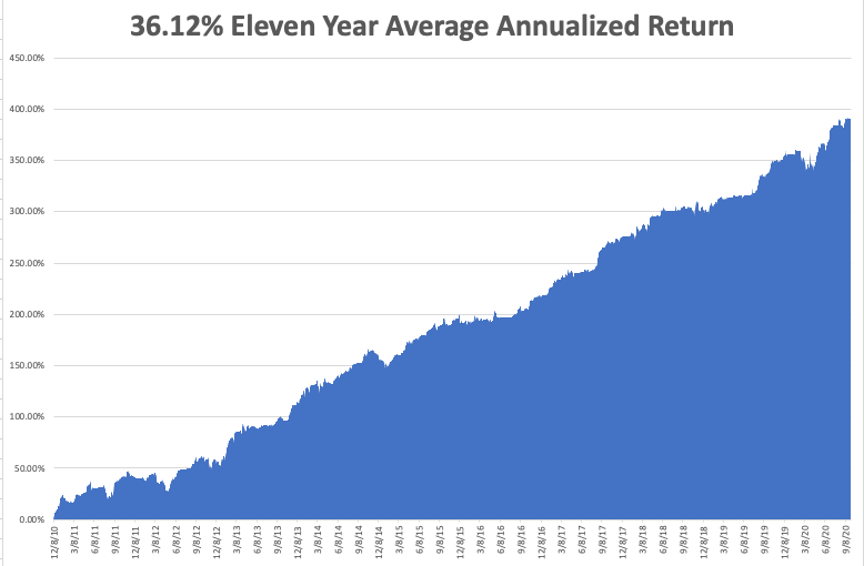

That takes our 2020 year-to-date performance back up to a blistering +35.46%, versus a loss of 2.87% for the Dow Average. October shot out the gate at +0.96%. That takes my 11-year average annualized performance back to +36.12%. My 11-year total return returned to another new all-time high at +391.37%. My trailing one-year return popped back up to +51.82%.

The coming week will be a dull one on the data front. The only numbers that really count for the market are the number of US Coronavirus cases and deaths, now at 210,000, which you can find here.

On Monday, October 5 at 10:00 AM, the ISM Non-Manufacturing PMI Index for September is released.

On Tuesday, October 6 at 9:00 AM EST, the JOLTS Job Openings for August is published.

On Wednesday, October 7 at 10:30 AM EST, the EIA Cushing Crude Oil Stocks are out. At 2:00 PM EST, the Fed Minutes from the last Open Market Committee Meeting six weeks ago are disclosed.

On Thursday, October 8 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, October 9, at 2:00 PM The Bakers Hughes Rig Count is released.

As for me, I’m headed up to Lake Tahoe again to escape the thick clouds of choking smoke in the San Francisco Bay Area. Also, the polls for the presidential election in Nevada open on October 17 and I have to VOTE!

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Is History Repeating Itself?