The Market Outlook for the Week Ahead, or The Inmates are Running the Asylum

I have decided to run for president next year. If you wondered why my content has been slacking off lately, it’s because I’ve been hard at work writing the Mueller Report. Oh, and the Dow Average will reach 100,000 by December.

Ha! Gotcha! April fool.

Still, looking at the market action last week, you really have to wonder if the inmates have seized control of the asylum when the average rose four of five days. These are people who are buying stocks at a decade high, with collapsing earnings, and the rest of the world falling into recession.

However, there is a method to their madness. Interest rates across every maturity in Europe and Japan turned negative last week. Suddenly both US stocks AND bonds looked like the bargain of the century, but only if you were foreign. An avalanche of cash into the US followed triggering an explosive move up in the bond market. For the first time in three years, I was not short.

And here’s the interesting part. It could continue for months.

In the meantime, investors have been grappling with a number that will be the most important print of the year. The first look at Q1 2019 GDP will be published on April 23, and it is widely expected to be awful, at less than a 1% annual rate. It will include the effects of the record 34-day government shutdown as well as the horrendous weather and flooding of last winter.

So, on the one hand, you have a stock market that is simultaneously being propped up by enormous cash flows and held back by a weakening economy and earnings and profit-taking from the best quarterly start in ten years. It all adds up to a market that could go absolutely nowhere.

And I just so happen to have the perfect portfolio for such a market. These are the precise conditions where deep in-the-money call and put option spreads absolutely prosper. When everything is going nowhere, spreads always expire at their maximum profit points.

The global easing trend is accelerating as central banks rush to head off the next global recession. Expect interest rates to drop to levels you once thought impossible.

The global bond short covering panic continues, with ten-year US Treasury yields dropping to an eye-popping 2.33%. Slowing global growth is to blame. Did I hear the word “refi”?

Foreign investors poured into the US bond market, driving ten-year US Treasury yields down to 2.33%. When everyone else in the world has negative yields, our bonds become the best paying in the world.

Q4 GDP final report came in at 2.2% as expected, down a third from Q3. Expect that figure to more than halve in Q1 2019. Put on your hard hat.

The Mueller Report gave Trump a clean bill of health, at least on the collusion issue. But it opened up a dozen other lines of investigation that will continue for years. It’s definitely a “RISK ON” development.

US Existing Home sales jumped 11.8% in January. Low mortgage interest rates are finally kicking in with the 30-year fixed at 4.23%. This is a one hit wonder, not the beginning of a new trend. But interest rates are going lower.

New Home Sales were up 4.9% to 667,000 units in February in a rare positive data point. Could low interest rates finally be kicking in? Still, avoid homebuilders.

Apple (AAPL) announced its new streaming service, Apple TV Plus, and the stock fell on a “sell the news” drop. Roku is included in the package so buy (ROKU). The Apple offering is weak enough to allow plenty of room for Disney to launch its own streaming service Disney Plus at the end of this year. Prepare for an onslaught of princesses. Buy (DIS) too.

Home price appreciation hit a four-year low with the S&P Case Shiller National Home Price Index growing only 4.2% YOY in January, down from 4.6% the previous month. Las Vegas, Phoenix, and Minneapolis are still showing the biggest gains while San Francisco and Seattle are seeing the biggest price drops. Avoid homebuilders (ITB).

Lyft (LYFT) priced at $72 a share, the top end of expectations, valuing the company at an eye popping $25 billion at the end of the day. Never mind that the company is losing money hand over fist, it’s all about potential. The tech IPO bubble top has started!

The Mad Hedge Fund Trader was up on the week with time decay in our combed 13 positions our best friend. The quarter end window dressing was kind to us.

March turned positive in a final burst, up 1.78%. My 2019 year to date return retreated to +15.49%, boosting my trailing one-year return back up to +35.16%.

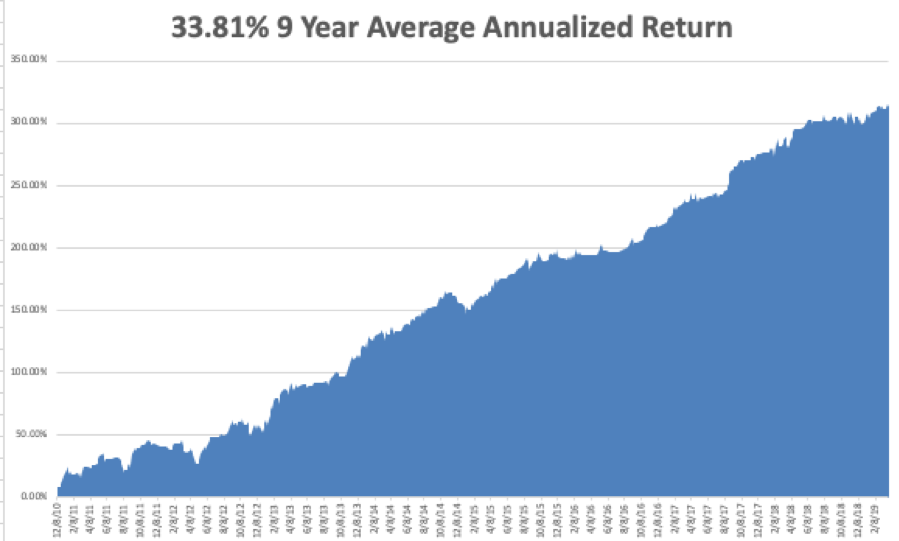

My nine-year return recovered to +315.56%, a new all-time high. The average annualized return appreciated to +33.81%. I am now 45% in cash, 30% long and 25% short, and my entire portfolio expires at the April 18 option expiration day in 9 trading days. I took generous profits on my positions in copper miner Freeport McMoRan (FCX) right when it bounced off the 200-day moving average.

The Mad Hedge Technology Letter maintained long positions in Microsoft (MSFT), Alphabet (GOOGL), and PayPal (PYPL), and Amazon (AMZN), which are clearly going to new highs.

It’s jobs week again with the usual trifecta of employment reports. Last month was a disaster, so this month will be interesting.

On Monday, April 1 at 8:30 AM, February Retail Sales are published.

On Tuesday, April 2, 8:30 AM EST, we learn February Durable Goods.

On Wednesday, April 3 at 8:15 AM, the ADP Employment Report comes out for private hiring.

On Thursday, April 4 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, April 5 at 8:30 AM, we obtain the big number of the week, the February Nonfarm Payroll Report.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’m going to use a rare spell of good weather to drive up to Lake Tahoe and start the planning work on my October 25-26 Mad Hedge Lake Tahoe Conference. Half the dinner tickets sold out on the first day, so you better get moving now.

Maybe it’s something I said? To learn more about the conference, please click here. I’ll see you there.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader