The Market Outlook for the Week Ahead, or Welcome to the Round-Trip Market

If you had followed my advice and taken a cruise around the world in December, you would be getting home about now. A review of your portfolio would review that most of your positions were either unchanged or down slightly.

And if you had chunky positions in bond shorts, as I pleaded, begged, and cajoled you into taking on, you would be sitting pretty. In fact, you could well afford to take yet another cruise around the world.

That could be the best advice I can give right now, for the next quarter, the market will remain trapped in a wide but volatile range. That’s fine if you are backed up with mainframe computers, a programming staff of a dozen strong, and dedicated lightning-fast fiber optic cables, all the resources of a high-frequency trader shooting for pennies per trade.

If instead, you’re trading on your iPhone in between meetings at work, on every other hole at the golf course, or whenever you have free time, as many of you do, you may well want to sit Q2 out. There are not any great trades out there at the moment, the market is still expensive and the challenges ahead are legion.

For a start, stocks are in the process of discounting one of those annoying recessions that aren’t going to happen, as it does about half the time. I know this is important for many of you who run their own businesses remorselessly tied to the economic cycle.

Yes, I know that there is a rising tide of recession calls from the analyst community. But the models that reliably worked in the past are missing two crucial factors.

They never had to account for Medusa’s head of supply chain problems we now face, where perhaps 5% of US GDP is tied up on the West coast docks stacked in containers ten high. Untie this Gordian knot and you get another surprise spurt for the economy.

The other is the coming reconstruction of Ukraine, one of the greatest public works projects of all time, on a scale with the WWII Marshall Plan. Every major engineering company in the world will have to get involved, including Fluor (FLR), Bechtel (private), and those in Europe, Japan, and China. I reckon it could add 1% of global growth per year for the next several years.

How are the impoverished Ukrainians going to pay for all this work? With the $1 trillion in overseas Russian assets already seized, Ukraine easily gets control through proceedings at the World Court.

All Putin really accomplished with his war was to bring forward the end of oil by 20 years, at least for Russia, and to shrink the Russian standard of living by 90% practically overnight. It has been duly kicked out of the global economy. A million Russians have already lost their jobs and the shelves in Moscow are empty.

By the way, you may have noticed that Apple was up every day for 11 days for the first time since 2003. All the war really meant is that you got to buy Apple for a few minutes at $150 instead of $160. This is not what coming recessions are made of. The Volatility Index (VIX) at $19 is screaming as much.

It all confirms my 2022 scenario of a rambunctious H1 followed an H2 zeroing in on new all-time highs. You heard it here first!

Now for last week’s highlights:

Unemployment Plunges to 3.6%, a new cycle low, with the hot 431,000 March nonfarm Payroll. It’s yet another reason for the Fed to raise interest rates and increases the prospects of a 50-basis point rise this month. Leisure and Hospitality gained an eye-popping 118,000, Professional & Business Services 102,000, and Manufacturing 38,000. The U-6 “discouraged worker rate” fell to an incredible 6.9%. The back months saw big upward revisions. Overall, it was a blowout report.

ADP up 455,000 in March, showing the jobs market is still on fire. Services are seeing huge gains. Leisure & Hospitality continues its post covid bounce back. It makes the coming Nonfarm Payroll report on Friday look pretty industry.

JOLTS Comes in Red Hot, showing that there were 11.3 million job openings in February, 5 million more than the number of unemployed. The great labor shortage continues and may be permanent, dashing all recession fears.

Will the Fed Screw Up? That is the biggest risk to the markets according to 46% of all investors. Rising inflation comes in at 33%. If the Fed panics and excessively raises interest rates in a tardy response to higher prices the 46% will be right.

The Five- and 30-Year Bonds Invert, meaning it is cheaper to borrow for 30 years than it is for five. Such a move usually presages a recession. Other than that, Mrs. Lincoln, how was the play?

Oil Plunges 8% on China Lockdown Fears, to $104.50 a barrel, as a new Covid wave hits Shanghai. China is the world's largest importer of oil by a large margin.

Tesla to Split Shares and Pay Dividend, according to SEC filings, sending the shares soaring by $90. (TSLA) has more than doubled since the last split in August 2020. Buy (TSLA) on dips.

S&P Case Shiller Up 19.2% in January, yet another new all-time high. Phoenix (33%), Tampa (31%), and Miami (28%) were the big winners and January is when mortgage interest rates started to rise sharply. This has led to an increase in all cash offers and buyers no longer qualify for loans. Home prices should keep rising for the rest of the decade, although at a slower rate.

Biden to Boost Battery Metal Production, by invoking the Defense Production Act, to hasten the end of our reliance on oil. Permitting and environmental regulation will get eased for the miners of lithium, cobalt, and nickel. The government has figured out that there are nowhere near the materials needed to meet the lofty sales forecasts of EV makers, like Tesla.

The Energy Sector Has Hit a Gusher in Profits, with earnings up an eye-popping 228% YOY. But if you are not in already, you missed it. Topping out risk is beginning, especially if the Ukraine War ends, cratering oil prices.

Biden to release 1 Million Barrels a Day for the SPR, the most in the 47-year history of the facilities, putting a serious dent in the current energy shortage. That’s against daily US consumption of 20 million barrels. The Strategic Petroleum Reserve currently has 714 barrels. It should be emptied and shut down as it is nothing more than a government subsidy for three two red states, Texas and Louisiana. Russia says it will only take rubles for oil and gas sales from Friday.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

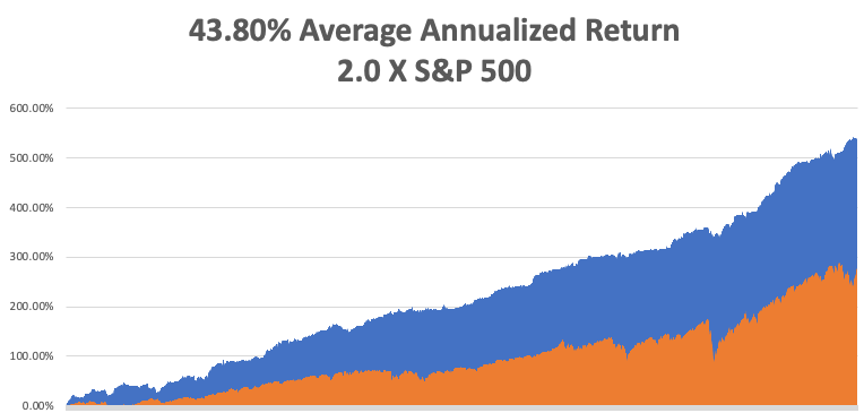

With near-record volatility, my March month-to-date performance retreated to a still blistering 12.26%. My 2022 year-to-date performance ended at a chest beating 26.85%. The Dow Average is down -4.00% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding more long positions in technology.

That brings my 13-year total return to 539.41%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 43.80%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.2 million and rising quickly and deaths topping 983,000 and have only increased by 1,000 in the past week. You can find the data here. The growth of the pandemic has virtually stopped, with new cases down 98% in two months.

On Monday, April 4 at 7:00 AM EST, US Factory Orders for February are published.

On Tuesday, April 5 at 9:00 AM, the ISM Non-Manufacturing Index for February is printed.

On Wednesday, April 6 at 11:00 AM, The minutes from the last Fed meeting are released and will almost certainly lean hawkish.

On Thursday, April 7 at 7:30 AM, the Weekly Jobless Claims are printed.

On Friday, April 8 at 8:30 AM, Wholesale Inventories for February are announced. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when I backpacked around Europe in 1968, I relied heavily on Arthur Frommer’s legendary paperback guide, Europe on $5 a Day, which then boasted a cult-like following among impoverished, but adventurous Americans. The charter airline business was then-booming, and suddenly Europe came within reach for ordinary Americans like me.

Over the following years, he directed me down cobblestoned alleyways, dubious foreign neighborhoods, and sometimes converted WWII air raid shelters, to find those incredible travel deals. When he passed through town some 50 years later, I jumped at the chance to chat with the ever cheerful worshipped travel guru.

Frommer believes there are three sea change trends going on in the travel industry today. Business is moving away from the big three travel websites, Travelocity, Orbitz, and Priceline, who have more preferential lucrative but self-enriching side deals with airlines than can be counted, towards pure aggregator sites that almost always offer cheaper fares, like Kayak.com, Sidestep.com, and Fairchase.com.

There is a move away from traditional 48-person escorted bus tours towards small group adventures, like those offered by Gap Adventures, Intrepid Tours, and Adventure Center, that take parties of 12 or less on culturally eye-opening public transportation.

There has also been a huge surge in programs offered by universities that turn travelers into students for a week to study the liberal arts at Oxford, Cambridge, and UC Berkeley. His favorite was the Great Books programs offered by St. John’s University in Santa Fe, New Mexico.

Frommer says that the Internet has given a huge boost to international travel, but warns against user-generated content, 70% of which is bogus, posted by hotels and restaurants touting themselves.

The 81-year-old Frommer turned an army posting in Berlin in 1952 into a travel empire that publishes 340 books a year or one out of every four travel books on the market. I met him on a swing through the San Francisco Bay Area (his ticket from New York was only $150), and he graciously signed my tattered, dog-eared original 1968 copy of his opus, which I still have.

Which country has changed the most in his 60 years of travel writing? France, where the citizenry has become noticeably more civil since losing WWII. Bali is the only place where you can still actually travel for $5/day, although you can see Honduras for $10/day. Always looking for a deal, Arthur’s next trip is to Chile, the only country in the world he has never visited.

Arthur’s Next Big Play is Bali

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader