The United States of Debt

With ten-year US Treasury yields hitting 4.00% yesterday, it’s time to pay the piper for the last 15 years of the borrowing rampage of epic proportions.

This is not a new thing.

We are, in fact, becoming the United States of Debt.

That Washington is taking the lead in this frenzy of borrowing is undeniable. The last administration took the national debt from $23 trillion to $28 trillion during four years of prosperity that was entirely borrowed from the future.

The Biden administration will eventually take that figure up to an eye-popping $38 trillion. That will be the final bill for ending the pandemic, putting 25 million people back to work, and bringing the second Great Depression to a close.

The National Debt exceeded US GDP in 2016, taking the debt to GDP ratio to the highest point since WWII.

Treasury Secretary Janet Yellen recently confided to me that, “It’s the kind of thing that should keep you awake at night.”

It gets worse.

According to the Federal Reserve Bank of New York, total personal debt topped $19 trillion by the end of 2020. An overwhelming share of personal consumption is now funded by credit card borrowing.

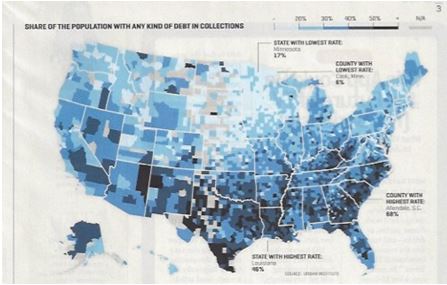

Some 33% of Americans now have debts in some form a collection, and that figure reaches an astonishing 50% in many southern states (see map below). Call it the Confederate States of Debt.

Corporations have also been visiting the money trough with increasing frequency, taking their debt to $6.1 trillion, up by 39% in five years, and by 85% in a decade.

The debt to capital ratio of the top 1,000 companies has ballooned from 35% to 54% and is now the highest in 20 years.

Another foreboding indicator is that corporate debt is rising faster than sales, with debt rising by a breakneck 8.5% annualized compared to 4.6% for sales over the past decade.

Automobile debt now tops $1 trillion and with lax standards has become the new subprime market.

And remember that other 800-pound gorilla in the room?

Student debt now exceeds $1.6 trillion and is rising, as is the default rate. Provisions in the last tax bill eliminate the deductibility of the interest on student debt, making lives increasingly miserable for young borrowers. And you wonder why the US birth rate is so low.

Of course, you can blame the low interest rates that have prevailed for the past decade. Who doesn’t want to borrow when the inflation adjusted long-term cost of money is FREE?

That explains why Apple (AAPL), with $270 billion in cash reserves held overseas, borrowed last year via ultra-low coupon 30-year bond issues, even though it doesn’t need the money. Many other major corporations have done the same.

And while everything looks fine on paper now, what happens if interest rates ever rise and stay high?

The Feds will be in dire straight very quickly. Raise short term rates to the 6% seen at the peak of the last cycle, and the nation’s debt service rockets from 4% to over 10% of the total budget. That’s when the sushi really hits the fan.

You can expect the same kind of vicious math to strike across the entire spectrum of heavily leveraged borrowers going forward, including big borrowers like cruise line, airlines, you, and me.

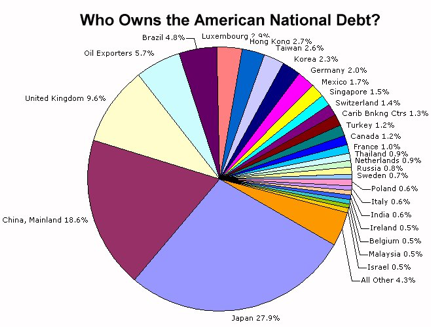

We are also witnessing the withdrawal of the Chinese as major Treasury bond buyers, who along with other sovereign buyers historically took as much as 50% of every issue. Threaten a war on your largest lender and it plays hell with you cash flow.

Rising supply against fewer buyers sounds like a recipe for eventually much higher interest rates to me.

Just watch this space for the next Trade Alert regarding when to get back in for the umpteenth time.