Trade Alert - (SPY) March 2, 2016

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price.

Trade Alert - (SPY)- STOP LOSS

SELL the S&P 500 SPDR?s (SPY) March, 2016 $200-$205 in-the-money vertical bear put spread at $4.05 or best

Closing Trade-NOT FOR NEW SUBSCRIBERS

3-2-2016

expiration date: March 18, 2016

Portfolio weighting: 10%

Number of Contracts = 24 contracts

I am going to exercise some risk control here and come out of my S&P 500 SPDR?s (SPY) March, 2016 $200-$205 in-the-money vertical bear put spread at cost.

The pennies we lost on this position was more than offset by the big profit we took yesterday on the S&P 500 SPDR?s (SPY) March, 2016 $170-$175 in-the-money vertical bull call spread.

When the market is bouncing around like a Duncan yoyo with a very long strong string, it is not time to be greedy.

I think the Friday nonfarm payroll will be strong, possibly giving us one more leg up on this short covering rally.

It really has been a year of unbelievable moves everywhere, and we are still well up on the year.

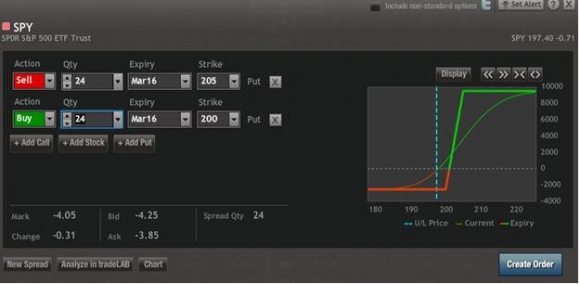

To see how to enter this trade in your online platform, please look at the order ticket below, which I pulled off of optionshouse.

If you are uncertain on how to execute an options spread, please watch my training video on ?How to Execute a Vertical Bear Put Debit Spread? by clicking here at http://www.madhedgefundtrader.com/ltt-executetradealerts/. You must me logged into your account to view the video.

The best execution can be had by placing your bid for the entire spread in the middle market and waiting for the market to come to you. The difference between the bid and the offer on these deep in-the-money spread trades can be enormous.

Don?t execute the legs individually or you will end up losing much of your profit. Spread pricing can be very volatile on expiration months farther out.

Here are the specific trades you need to execute this position:

Sell 24 March, 2016 (SPY) $205 puts at????.?.??$8.30

Buy to cover short 24 March, 2016 (SPY) $200 puts at.?..$4.25

Net Cost:???????????????????......$4.05

Loss: $4.08 = $4.05 = -$.03

(24 X 100 X -$0.03) = -$72 or -0.07% loss for the notional $100,000 portfolio