Why Amazon is Taking Over the World

Amazon, being the best publicly traded company in America, has more than one way to skin a cat.

That is what I took away during the mixed bag of an earnings call.

The road forward for most companies are defined by one maybe two unforgiving directions that the company has no choice but to migrate down through no fault of their own due to market forces.

Amazon operates in a different universe and the breadth of optionality for Amazon is breathtaking.

They have chosen to try to spike their future core business which has traditionally proven to pay dividends within three years or less.

Investors have always allowed Amazon to revert back to the reinvestment blueprint for added profitability - profits should reaccelerate once more in 2020.

Take into consideration that 2018 was a “light” year in Amazon’s reinvestment cycle in which Amazon only grew its fulfillment and shipping square footage by 15% and its headcount by 14%.

Amazon has used this playbook before. The warehouse efficiencies that benefited margins in 2018 was a direct result of massive capital expenditures into robot technology in the preceding years before that.

Amazon guided weakly on top line growth because of several regulation quagmires in India.

The Indian government began banning foreign online retailers from selling products from marketplace vendors that they have an equity stake in, leading Amazon to shelf items from its Indian site including its popular Echo speakers.

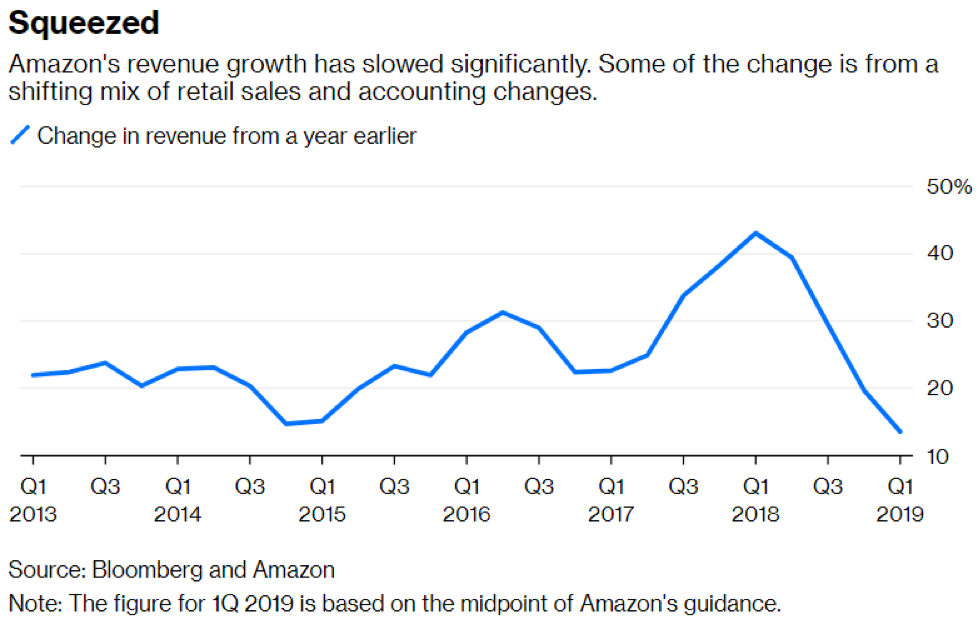

The $72.38 billion translating into 20% YOY fourth quarter revenue growth was its weakest since 2015.

They still have some work to do with physical stores, mostly Whole Foods, which saw a dip of 3% YOY in revenue.

Investors shouldn’t worry too much about this because Amazon can quickly switch back and ramp up revenue expansion when need be.

India is what China was 15 years ago and will morph into its own consumer supergiant with a population to service Amazon sales in the future.

Even with these headwinds that could frustrate operating margins and top-line revenue, Amazon still has some robust drivers in its portfolio in the form of cloud division Amazon Web Services (AWS) that grew 45% YOY and its advertising business which will perpetuate 50% YOY growth trajectory going forward.

Some other highlights were outperformance in voice tech with Amazon CEO Jeff Bezos gloating that “Echo Dot was the best-selling item across all products on Amazon globally, and customers purchased millions more devices from the Echo family compared to last year.”

In hindsight, the report wasn’t bad considering Q4 is the quarter Amazon usually diverges the most with expectations because of the sky-high expectations of the Christmas season.

Digital advertising is already a $12 billion-plus annual business and earned Amazon over $3 billion last quarter.

These lucrative businesses give Amazon more leeway into combatting headwinds that slow down its e-commerce engine.

The e-commerce side of business changes rapidly causing capital to be earmarked for reinvestment as others catch up to its latest iteration of Amazon.com.

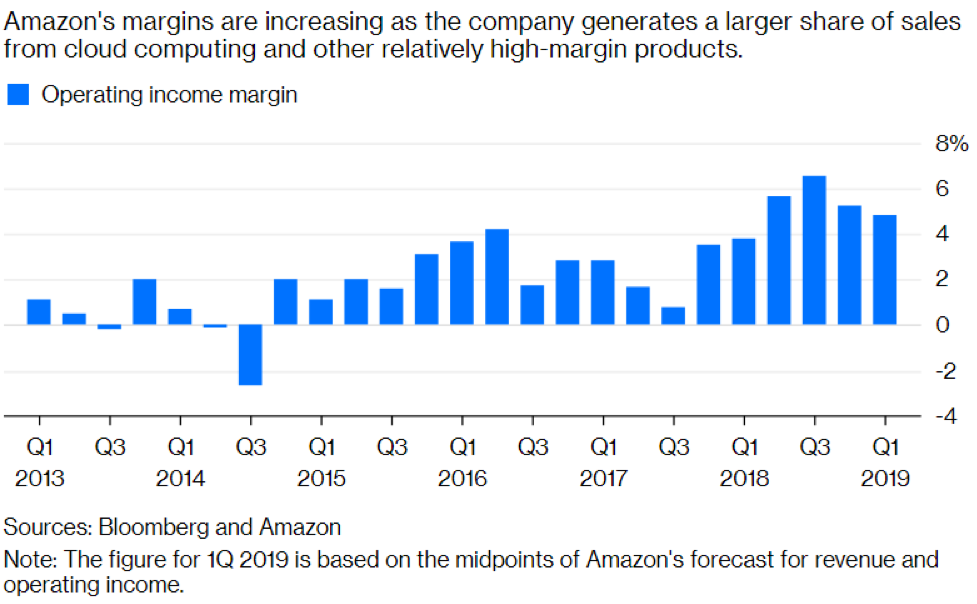

That being said, operating income margins are still over 4% and for the business model Amazon is trotting out, it is still a healthy number.

Not only that, AWS’ margins still remain intact at a robust 29%.

Consumers will agree with you admitting they can visibly notice the e-commerce platform improving over time.

The mixed results dinged shares 4% and I would classify this as a positive down day considering that from peak to trough, Amazon gained 35% after the December sell-off.

If these earnings came out in December, I would not have been shocked with a 15% haircut, but this speaks volumes to how tech shares have been resilient.

And tech earnings, for the most part, have been encouraging relative to expectations.

The change in rules has bred uncertainty in its Indian operation and management will wait for the dust to settle to carve out a plan ahead, but this is small potatoes in the larger picture because of the cash cow that is rich western countries.

To sum things up, Amazon’s services and e-commerce platform is still humming along, but growth is tapering off just a tad.

Amazon plans to juice up their business model by reinvesting into their model extracting the bounty in the years ahead.

The lead up to this will be a broad-based harvest resulting in stock price acceleration.

Do not forget we just went through a global growth scare, and I still believe that if the overall market will rise, the tech sector will need to participate with the bigger names carrying a substantial load.

An even more positive signal are the likes of Facebook, Apple, and Netflix buoying nicely, boding well for short-term price action.

This all means that Amazon should be a buy on the dip company with its long-term growth story more attractive than any other tech name, and by a wide margin.

Margins could come down temporarily in the spring and summer offering weakness for investors to buy into.

Amazon is truly a multi-dimensional beast that uses its capital wisely to create red hot businesses that never existed before.

Such is the magnitude of innovation at Amazon to the point that I would argue that Amazon is the most innovative American company today, period.

I sit on the edge of my seat to see what Amazon does next and you should too.

The easiest way to play this is to buy and hold shares for the long term on any major ephemeral stock offloading because they dominate like any other company in their field in relative terms.

Amazon will be back above 2,000 later in 2019 or early 2020.