Will Investors Pay the High Premium for Zillow?

In a typical year, spring begins the traditional home-buying season. But we know that this past year was anything but ordinary.

An internal Zillow (Z) report indicated that the pandemic has indeed caused people to rethink where they live and concludes that approximately 8 million existing homeowner households that have been on the sidelines may enter a real estate market already beset by unrelenting demand.

Also, 8.9% of consumers plan to purchase a home in the next six months near a 20-year high per the conference board's April consumer confidence survey.

The housing market is underpinned by demographic and economic tailwinds that will persist for the foreseeable future.

Millennials are moving up.

Baby Boomers are downsizing and in between, people of all generations are rethinking their lives.

Zillow (Z) is the most popular real estate portal in the country with hundreds of millions of consumers visiting the platform.

It’s easy to put up an advertisement on Zillow, while other competitors need to spend tens of millions of dollars to generate those leads.

It’s a sustainable competitive advantage which is one of the main factors for the stock going from $20 to $200 last year.

This effectively makes Zillow’s customer acquisition cost zero!

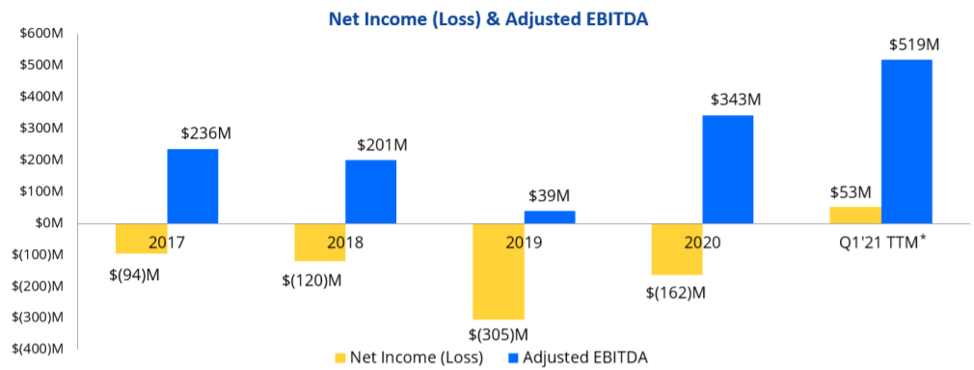

And because of that, it’s disappointing that they aren’t more profitable.

The PE ratio is currently 517 and as we look forward, we need to ask ourselves, will investors continue to bid up this high growth real estate tech stock?

This past quarter’s revenue growth was strong with Zillow reporting Q1 revenue of $1.2 billion, exceeding the high end of the forecast.

Q1 Internet, media, and technology (IMT) segment revenue was $446 million, grew 35% year-over-year, as this company continues to see accelerated growth in Premier Agent and strong growth in rentals.

This is Zillow’s bread and butter and represented over 37% of their total revenue.

Premier Agent revenue that connects realtors to consumers grew 38% year-over-year in Q1, the accelerated growth was primarily driven by connections growing faster than traffic, as well as focus on providing outstanding service and optimizing to connect high intent customers with high performing partner agents.

The inherent strength of the company lies in being the Uber of real estate and matching up ad-paying agents to customers.

However, I do believe we are hitting the high-water mark in the short-term as housing inventory levels hit generational lows and sellers stop putting their homes up for sale.

Therefore, it’s easy to argue that Zillow and its revenue growth will have a hard time pushing incremental growth now, and like many other tech firms, are facing tough metrics to beat year-over-year in for next earnings’ season.

Cratering interest rates of 2020 was the catalyst that drove the incremental buyer into the market, and I believe that harvest has mostly been collected.

Prospective buyers simply are at the extreme upper limit of affordability, now that the median house for sale in the U.S. is around $400,000.

Growth in Zillow Offers which is direct purchase and sale of homes continued to reaccelerate in Q1.

Zillow reported home segment revenue of $704 million, which exceeded the high-end outlook with 1,965 home sales.

Purchases increased to 1,856 homes in the quarter from 1,789 homes purchased in Q4, but not quite at the rapid pace planned as Zillow continued to work on retooling algorithm models to catch up with the rapid acceleration in home price appreciation.

The flipping game is just becoming too expensive, even for a subsidized tech corporation like Zillow and the algorithms are having a hard time competing with properties selling for $50,000 over the asking price!

Zillow is now competing with Qatar Sheikhs, sovereign wealth funds, and family offices of the elite who are piling into U.S. residential real estate at the same time.

Management has said they “buy homes at the median”, but wait, I thought technology would find the market inefficiencies in the pricing and Zillow would be able to find discounts.

Apparently not and that goes out of the window in an era of ultra-liquidity.

Management also claims they avoid buying houses in “really wealthy or really unique neighborhoods because they’re harder to resell and harder to price.”

The problem I have with Zillow Offers is that this division would be sucker-punched by a devastating blow from a property market pullback and be stuck with the carrying costs of thousands of mortgages and homeowner association fees per month.

That’s most likely the real reason for avoiding pricey areas.

Also, there is the conundrum that in market downdrafts, pricing power in the neighborhoods that Zillow targets fall fastest in terms of velocity of price and quality of buyer.

Even more worrying, Zillow charges the seller a fee of about 7.5% on average, which is notably higher than the traditional 6% commission a seller pays to realtors.

I thought technology was supposed to incite a deflationary effect?

Apparently not.

Mortgages segment revenue increased 169% year-over-year in Q1 to $68 million and was primarily driven by mortgage loan origination volume, which was up more than 8x year-over-year.

Sure, the 8x growth looks great on paper, but this division is still only 5% of total revenue and is a recipient of the law of small numbers looking better than they are.

In Q1, refinance loan origination volume comprised 90% of total origination volume.

There will be no refi boom in 2021.

Zillow really missed a gold mine in the mortgage division last year when they couldn’t even turn a profit in this division.

For the IMT segment, Zillow is forecasting 66% year-over-year revenue growth in Q2.

This is Zillow’s strength and you can expect Premier Agent revenue to be between $342 million to $350 million up 80% year-over-year.

On a sour note, they expect mortgage segment revenue to be down from Q1 and with respect to margins, Zillow’s Q2 IMT margin is expected to be 41% down sequentially from the 47% in Q1.

It’s clear that on the horizon, margins will shrink and nascent businesses will stall, and that’s a poor recipe for short-term price action in shares.

I don’t think investors will pay the current high premium for Zillow at these inflated levels, and yes, it’s a great buy and hold long term company, with a superior ad business that connects agents, but I do not see the case for the next leg up in the next few months.

This year will be remembered as a consolidation year as a few years of revenue were brought forward because of a once-in-a-lifetime interest rate collapse and pandemic tailwind.

Unfortunately, this year might just be too boring to 10X Zillow’s stock.