Mad Hedge Biotech and Healthcare Letter

May 6, 2022

Fiat Lux

Featured Trade:

(A PANDEMIC CONQUEROR READY FOR MORE)

(PFE), (BNTX), (AMGN), (JNJ), (BIIB), (RHHBY), (SGMO), (BMRN)

Mad Hedge Biotech and Healthcare Letter

May 6, 2022

Fiat Lux

Featured Trade:

(A PANDEMIC CONQUEROR READY FOR MORE)

(PFE), (BNTX), (AMGN), (JNJ), (BIIB), (RHHBY), (SGMO), (BMRN)

The past 50 years have been excellent for investors as stocks have climbed by over 100% within a five-year span ending last December 2021.

Sadly, this story has taken a different course in 2022 as investors became more cautious primarily due to inflationary fears.

However, a handful of businesses are strong and promising enough to survive and even thrive in a high inflation environment.

One company that met this challenge head-on in the healthcare and biotechnology sector is Pfizer (PFE).

In fact, Pfizer didn’t simply meet the estimates of Wall Street in its 2022 first-quarter earnings report. It blew past their expectations.

Pfizer recorded $25.7 billion in revenue for the first quarter, well above the consensus estimate of $23.9 billion. This represented a 77% surge year-over-year.

Meanwhile, its earnings per share of $1.62 was notably higher than the average $1.47.

As anticipated, these gains were mainly driven by the staggering revenues from its COVID-19 vaccine and antiviral medication.

Comirnaty continued its winning ways, with Pfizer generating a jaw-dropping $13.2 billion in sales from the vaccine it co-created with BioNTech (BNTX).

The company's market share in the developed world currently stands at 67%, while it holds 62% of the global market.

As for its Paxlovid antiviral treatment, this drug raked in $1.5 billion in the first quarter and claimed approximately 90% of the US market.

Evidently, Pfizer continues to receive massive boosts from its COVID-19 treatments.

Now, the real question moving forward hinges on whether these financial results can be normalized as part of Pfizer’s future regardless of the pandemic’s effects.

After all, the vaccine sales comprised almost 60% of the company’s total revenue. With this in mind, Pfizer remains firm in its projections that it could rake in $98 billion to $102 billion in annual revenue for 2022.

While this still indicates a strong belief in the pandemic-related treatments, it’s also indicative of a deeper and more diverse pipeline.

Although not as high-flying as the COVID-19 vaccines, a number of other categories notched notable gains year-over-year, like its rare disease segment, which saw a 23% increase.

The growth of its oncology sector, which recorded a 6% climb, was mainly attributed to the 35% rise and expansion of Pfizer’s biosimilar arm.

So far, the top-selling treatments in this segment are Retactrit, a biosimilar of Amgen’s (AMGN) Epogen and Johnson & Johnson’s (JNJ) Procrit, Zirabev, a biosimilar of Roche’s (RHHBY) Avastin, and Rixience, a biosimilar of Biogen’s (BIIB) Rituxan.

Even Pfizer’s pneumonia vaccines showed off a 22% growth this quarter with $1.57 billion in sales.

Apart from these, the FDA has recently lifted the hold on the Hemophilia A gene therapy clinical trials of Pfizer and Sangamo (SGMO).

Without this limitation, the two companies may already have the opportunity to catch up to the leading biotech in this sector, BioMarin (BMRN). If everything works out, Pfizer and Sangamo are slated to release a readout from this program by the second half of 2023.

Another venture that’s expected to pay off soon is Pfizer’s $6.7 billion acquisition of Arena Pharmaceuticals, which was seen as a decisive move to bolster its inflammation and immunology segment.

The company is expected to file for a regulatory for Etrasimod, Arena’s lead program on ulcerative colitis and Crohn’s disease, by the second half of 2022.

This means that the recent acquisition is already expected to add to the near-term growth of Pfizer, which could be as early as 2023.

Moreover, Etrasimod represents an incredible market opportunity, with the treatment projected to reach $28 billion in annual sales by 2025.

Aside from the promising potential of Arena’s pipeline, Pfizer’s move also shows how the company is leveraging the capital influx from its COVID sales and its strategy on a more aggressive growth investment cycle.

On top of that, Pfizer’s partnership with BioNTech highlighted the benefits and competitive advantage in terms of how the biopharmaceutical titan works and collaborates with smaller biotechnology firms.

Hence, Pfizer has made itself the first and obvious choice among budding companies with groundbreaking innovations.

Overall, Pfizer has proven itself more than capable of handling any economic and health crisis. Not only has it come up with a solution that ultimately saved humanity from a deadly virus, but it also emerged victorious and stronger amid a global meltdown.

Given its history and trajectory, it looks like it has nowhere else to go but up. Hence, it would be best if you bought the dip.

Mad Hedge Biotech and Healthcare Letter

February 15, 2022

Fiat Lux

Featured Trade:

(AN EMERGING LEADER IN THE HEALTHCARE REVOLUTION)

(CRSP), (VRTX), (EDIT), (NTLA), (PFE), (NVS), (GILD), (RHHBY), (BMRN), (QURE), (SGMO), (CLLS), (ALLO), (BEAM)

Mankind has always imagined a future filled to the brim with technological advancements serving as the panacea to all our ills.

One of the prevailing ideas focuses on the developments found in the healthcare sector.

Movies, television shows, graphic novels, and books have all pictured a world with such revolutionary technologies capable of not only diagnosing but also curing any and all types of diseases.

Since the introduction of these ideas, many have believed that these would remain in the fictional universe. However, these “ideas” have slowly transformed into reality.

One of the biggest indicators that we’re heading in that direction is the 2020 Nobel Prize in Chemistry by Jennifer Doudna and Emmanuelle Charpentier. The two were recognized for their pioneering work in CRISPR-Cas9.

Basically, Crispr-Cas9 functions like molecular scissors.

What makes this technology incredible is that Crispr-Cas9 can classify a single address out of 3 billion letters within the genome by using only a particular sequence. With this, we can repair thousands of genetic conditions and even offer more potent ways to battle cancer.

This Nobel Prize led to commercializing the 2012 discovery, Crispr-Cas9, at breakneck speed, with gene-editing companies like CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), and Intellia Therapeutics (NTLA) gaining a considerable boost in their values.

Surprisingly, the trajectory of these gene-editing stocks took a tragic turn in 2021.

In fact, the once-upon-a-time-market-darling CRISPR Therapeutics saw its market capitalization brutally shaved off from $8.7 billion to $4.55 billion in the past months.

No matter how we look at it, there’s genuinely no way to sugarcoat the reality: the market has been second-guessing CRISPR Therapeutics’ ability to truly deliver on its promise.

That is, investors have started to wonder whether the company’s early stage success would amount to anything commercially.

CRISPR Therapeutics is currently working on a treatment that would implant tumor-targeting immune cells on cancer patients. The company is also prioritizing therapies that could edit cells to treat diabetes.

So far, it has made significant progress in developing treatments for a genetic disorder called sickle cell.

In the US alone, at least 100,000 people suffer from sickle cell disease, with 4,000 more born every year. Conservatively, we can estimate at least 3,000 patients availing of this one-time treatment at over $1.6 million a pop.

To date, CRISPR Therapeutics has five candidates under clinical trials for diseases like B-thalassemia, sickle cell disease, and other regenerative conditions.

It has four more queued, which target diabetes, cystic fibrosis, and Duchenne muscular dystrophy.

Compared to its rivals in the space, it’s clear that CRISPR Therapeutics is ahead when it comes to product development and trials.

Two of its candidates, transfusion-dependent beta thalassemia treatment CTX001 and sickle cell disease therapy CTX110, have already been submitted for clinical tests for safety and efficacy.

Recently, Vertex (VRTX) boosted its 2015 agreement with CRISPR Therapeutics by 10%, with the deal reaching $900 million upfront to push for quicker results in developing CTX001.

This is a crucial move for Vertex, but more so for CRISPR Therapeutics as CTX001 holds a highly lucrative addressable market.

The additional funding significantly widened the gap between the Vertex-CRISPR team and bluebird bio (BLUE) in the race to launch a new gene-editing therapy targeting sickle cell disease and beta thalassemia.

To sustain its growth, CRISPR Therapeutics’ strategy is to develop drugs that only require mid-level complexity but can rake in generous financial rewards.

This is a similar tactic used by bigger and more established biotechnology companies like Pfizer (PFE), Novartis (NVS), and Gilead Sciences (GILD).

Evidently, this strategy is a great way to ensure cash flow.

Aside from its earnings from the commercialization of these products, CRISPR Therapeutics can also attract larger companies to buy the intellectual property of their breakthrough treatments.

After all, startups generally get 100% premiums in contracts with Big Pharma.

Good examples of this are Novartis that bought AveXis and Roche’s (RHHBY) purchase of Spark Therapeutics.

The Roche-Spark agreement led to the first ever FDA-approved treatment since gene therapy trials started in the 1990s. It was for the genetic blindness therapy Luxturna, which received the green light in 2017.

The second approved treatment was a muscle-wasting disease therapy Zolgensma, which was the fruit of the Novartis-Avexis acquisition.

Both conditions are rare, but the financial rewards are impressive.

At $2 million for each treatment, Zolgensma sales reached $1.2 billion annually. At the rate the therapy is selling, Novartis estimates that Zolgensma will surpass the $2 billion mark in 2021.

Novartis and Roche aren’t the only ones partnering with smaller gene editing companies.

Pfizer has been working with biotechnology companies BioMarin Pharmaceutics (BMRN) and UniQure (QURE) to develop a treatment for blood-clotting disorder hemophilia.

The COVID-19 frontrunner is also collaborating with Sarepta Therapeutics (SRPT) to come up with a treatment for Duchenne muscular dystrophy.

Gene editing has also served as the foundation for several biotechnology companies out there today like Sangamo Therapeutics (SGMO), Cellectis (CLLS), and Allogene Therapeutics (ALLO).

The market size for gene editing treatments is estimated to be worth $11.2 billion by 2025, with the number rising between $15.79 billion to $18.1 billion by 2027.

This puts the compounded annual growth rate of this sector to be at least roughly 17%.

While this is already groundbreaking with only a handful of companies knowing how to utilize the technology, the gene-editing world has come up with a more advanced technique than Crispr-Cas9.

The technology is founded on the “base editing” or “prime editing” technique, which is the simplest type of gene editing that alters only one DNA letter.

So far, one company holds exclusive rights to this technology: Beam Therapeutics (BEAM).

When the technology became public, Beam stock has increased sixfold since its IPO in February 2020.

This latest development can resolve thousands of genetic diseases. However, it still requires further trials since “base editing” can also trigger damaging responses from the body.

Overall, I think CRISPR Therapeutics is the most promising among these high-risk stocks.

The data from two of its candidates, CTX001 and CTX110, are promising. The added funding from Vertex boosts the confidence of investors that a regulatory approval is well on its way.

The company is also sitting on a massive cash pile and investing aggressively across different rare disease programs.

While the company has yet to be considered a major force in the biotechnology world, the potential multiple successes of its products could generate a company worth hundreds of billions.

This potential alone offers an investing opportunity with a substantial asymmetric advantage for its current share price.

However, bear in mind that the stock is not for conservative investors considering risks.

More importantly, its pipeline requires patience. Hence, CRISPR Therapeutics should be played as a long-term investment.

Mad Hedge Biotech & Healthcare Letter

April 27, 2021

Fiat Lux

FEATURED TRADE:

(THE FUTURE OF MEDICINE)

(CRSP), (VRTX), (EDIT), (NTLA), (PFE), (NVS), (GILD), (RHHBY),

(BMRN), (QURE), (SGMO), (CLLS), (ALLO), (BEAM)

Winning the Nobel Prize in 2020 provided biotechnology companies more traction on Wall Street.

The victory led to commercializing the 2012 discovery, Crispr-Cas9, at breakneck speed, with gene editing companies like CRISPR Therapeutics (CRSP), Editas Medicine (EDIT), and Intellia Therapeutics (NTLA) gaining considerable boost in their values.

Since then, the total market value for the products of these three has more than doubled in recent months to reach $23 billion.

Basically, Crispr-Cas9 functions like molecular scissors.

What makes this technology incredible is that Crispr-Cas9 can classify a single address out of 3 billion letters within the genome by using only a particular sequence. With this, we can repair thousands of genetic conditions and even offer more potent ways to battle cancer.

The market favorite among the gene editing companies so far is CRISPR Therapeutics, with $8.72 billion in market capitalization.

In comparison, Editas has $2.76 billion while Intellia Therapeutics has $4.15 billion.

CRISPR Therapeutics is currently working on a treatment that would implant tumor-targeting immune cells in cancer patients. The company is also prioritizing therapies that could edit cells to treat diabetes.

So far, it has made significant progress in developing treatments for a genetic disorder called sickle cell.

In the US alone, at least 100,000 people suffer from sickle cell disease, with 4,000 more born every year. Conservatively, we can estimate at least 3,000 patients availing of this one-time treatment at over $1.6 million a pop.

To date, CRISPR Therapeutics has five candidates under clinical trials for diseases like B-thalassemia, sickle cell disease, and other regenerative conditions.

It has four more queued, which target diabetes, cystic fibrosis, and Duchenne muscular dystrophy.

Compared to its rivals in the space, it’s clear that CRISPR Therapeutics is ahead when it comes to product development and trials.

Two of its candidates, transfusion-dependent beta thalassemia treatment CTX001 and sickle cell disease therapy CTX110, have already been submitted for clinical tests for safety and efficacy.

Recently, Vertex (VRTX) boosted its 2015 agreement with CRISPR Therapeutics by 10%, with the deal reaching $900 million upfront to push for quicker results in developing CTX001.

This is a crucial move for Vertex, but more so for CRISPR Therapeutics as CTX001 holds a highly lucrative addressable market.

The additional funding significantly widened the gap between the Vertex-CRISPR team and bluebird bio (BLUE) in the race to launch a new gene editing therapy targeting sickle cell disease and beta thalassemia.

To sustain its growth, CRISPR Therapeutics’ strategy is to develop drugs that only require mid-level complexity but can rake in generous financial rewards.

This is a similar tactic used by bigger and more established biotechnology companies like Pfizer (PFE), Novartis (NVS), and Gilead Sciences (GILD).

Evidently, this strategy is a great way to ensure cash flow.

Aside from its earning from the commercialization of these products, CRISPR Therapeutics can also attract larger companies to buy the intellectual property of their breakthrough treatments.

After all, startups generally get 100% premiums in contracts with Big Pharma.

Good examples of this are Novartis that bought AveXis and Roche’s (RHHBY) purchase of Spark Therapeutics.

The Roche-Spark agreement led to the first-ever FDA-approved treatment since gene therapy trials started in the 1990s. It was for the genetic blindness therapy Luxturna, which received the green light in 2017.

The second approved treatment was a muscle-wasting disease therapy Zolgensma, which was the fruit of the Novartis-Avexis acquisition.

Both conditions are rare, but the financial rewards are impressive.

At $2 million for each treatment, Zolgensma sales reached $1.2 billion annually. At the rate the therapy is selling, Novartis estimates that Zolgensma will surpass the $2 billion mark in 2021.

Novartis and Roche aren’t the only ones partnering with smaller gene editing companies.

Pfizer has been working with biotechnology companies BioMarin Pharmaceutics (BMRN) and UniQure (QURE) to develop a treatment for blood-clotting disorder hemophilia.

The COVID-19 frontrunner is also collaborating with Sarepta Therapeutics (SRPT) to come up with a treatment for Duchenne muscular dystrophy.

Gene editing has also served as the foundation for several biotechnology companies out there today like Sangamo Therapeutics (SGMO), Cellectis (CLLS), and Allogene Therapeutics (ALLO).

The market size for gene editing treatments is estimated to be worth $11.2 billion by 2025, with the number rising between $15.79 billion to $18.1 billion by 2027.

This puts the compounded annual growth rate of this sector to be at least roughly 17%.

While this is already groundbreaking with only a handful of companies knowing how to utilize the technology, the gene editing world has come up with a more advanced technique than Crispr-Cas9.

The technology is founded on the “base editing” or “prime editing” technique, which is the simplest type of gene editing that alters only one DNA letter.

So far, one company holds exclusive rights to this technology: Beam Therapeutics (BEAM).

When the technology became public, Beam stock has increased sixfold since its IPO in February 2020.

This latest development can resolve thousands of genetic diseases. However, it still requires further trials since “base editing” can also trigger damaging responses from the body.

Overall, I think CRISPR Therapeutics is the safest among these high-risk stocks.

The data from two of its candidates, CTX001 and CTX110, are incredibly promising. Plus, the added funding from Vertex boosts the confidence of investors that regulatory approval is well on its way.

The company is also capitalizing on the surging price of its stock and investing aggressively across different rare disease programs.

While the company has yet to be considered a major force in the biotechnology world, the potential multiple successes of its products could generate a company worth hundreds of billions.

This potential alone offers an investing opportunity with a substantial asymmetric advantage for its current share price.

However, bear in mind that the stock is still a risk and should be played as a long-term investment. Hence, you should buy on dips.

Mad Hedge Biotech & Healthcare Letter

July 9, 2020

Fiat Lux

Featured Trade:

(DOUBLING UP AGAIN ON BIOTECH),

(BMRN), (VRTX), (GILD), (MRNA), (CRSP)

If the volatility of the stock market lately has been making you sick, then it might be time to add more biotechnology and healthcare stocks to your portfolio. They’re all having the effect of dragging each other up in this superheated environment.

Investors looking for these businesses can find a safe haven in rare diseases big player BioMarin Pharmaceutical (BMRN), which has $16.5 billion in market capitalization.

While most businesses languished since the pandemic broke this 2020, this biotechnology company’s shares rose by 12% this year. That’s not where it ends, though.

BioMarin could still pick up even more momentum despite the second wave of COVID-19.

The company currently has an extensive pipeline aimed at rare genetic diseases, with seven already approved and marketed in over 75 countries across the globe.

Looking at BioMarin’s first quarter earnings report for 2020, the company recorded a revenue of $502.1 million. This shows a 25% increase from the $400.7 million it raked in during the same period in 2019. It also handily beat the analysts’ estimate of $468.8 million.

Among BioMarin’s products, genetic metabolic disorder infusion Naglazyme is considered the top-selling treatment.

Sales of this product climbed 32% year over year in the first quarter to hit $27.4 million, with the jump primarily attributed to an increase in sales in Russia and Brazil.

However, the rising stars of BioMarin are two enzyme replacement treatments.

One is genetic blood disorder treatment Palynziq, which skyrocketed by 181% year over year to reach $22.3 million.

The other is Batten disease treatment Brineura, which soared by a whopping 97% to rake in $24 million.

Three of BioMarin’s drugs also performed well during this quarter.

Phenylketonuria drug Kuvan recorded $15.1 million in sales, up by 14% from the same period in 2019.

Meanwhile, Morquio A syndrome medication Vimizim generated $11.4 million in sales, showing off a 9% year over year jump as well. As for Aldurazyme, this Hurler syndrome drug’s sales rose by 23% to reach 10.4 million.

Now, the company is looking into another rare-disease treatment, which could cover Hemophilia A therapies via its experimental gene therapy Roctavian. This can open up a huge market for BioMarin, with over 20,000 Americans suffering from this disease.

Roctavian is expected to receive the FDA green light earlier than its August 21 decision date, possibly marking another blockbuster drug added to BioMarin’s pipeline.

Needless to say, the steady sales growth of these products served as the major driver of the company’s improving bottom line.

Over the past 10 years, the annual revenue of BioMarin has consistently climbed and beat analysts’ expectations -- a trend that’s likely to go on in the next decade as well.

Another company that built its name on rare diseases treatments is Vertex Pharmaceuticals (VRTX).

While most stocks struggle to deal with black swan situations like the COVID-19 pandemic, Vertex is poised to enter the $100 billion market cap club soon.

In fact, the company recently updated its 2020 guidance, increasing its initial estimate from $5.1 billion and $5.3 billion to $5.3 billion to $5.6 billion.

In sum, Vertex is poised to continue its upward trajectory despite the current economic landscape.

The confidence in its growth is bolstered by its recent earnings report for the first quarter of 2020, which indicated an impressive 77% year over year to reach a net revenue of $1.5 billion.

At the moment, Vertex has $61.7 billion in market capitalization, with the company transforming into the most dominant player in the cystic fibrosis (CF) space. Actually, Vertex holds the monopoly on the approved drugs used to treat CF, namely, Kalydeco, Orkambi, and Symdeko.

Apart from its efforts to continuously dominate the CF sector, Vertex also has several moonshots that can eventually turn into major catalysts.

Among those is its partnership with CRISPR Therapeutics (CRSP).

The two biotechnology companies are developing a gene therapy called CTX001 which can cure rare genetic blood diseases. Specifically, CTX001 is designed to cure beta-thalassemia and sickle cell disease.

Apart from its partnership with CRISPR Therapeutics, Vertex also acquired Semma Therapeutics in 2019 with the goal of coming up with a cure for Type 1 diabetes. If things go as planned, a gene therapy for this genetic disease will advance to clinical testing by early 2021.

While the world is mired in crisis, the biotechnology sector has been fueled with excitement particularly because of the potential COVID-19 vaccines and cures from companies like Gilead Sciences (GILD) and Moderna (MRNA).

With insistent whispers that a second wave of the deadly COVID-19 is well on its way, opportunistic investors are actively seeking defensive stocks with businesses that can withstand the second wave of infections.

Both BioMarin and Vertex offer safe bets in this increasingly unpredictable world. Aside from proving their capacity to expand, both also have incredible room for growth.

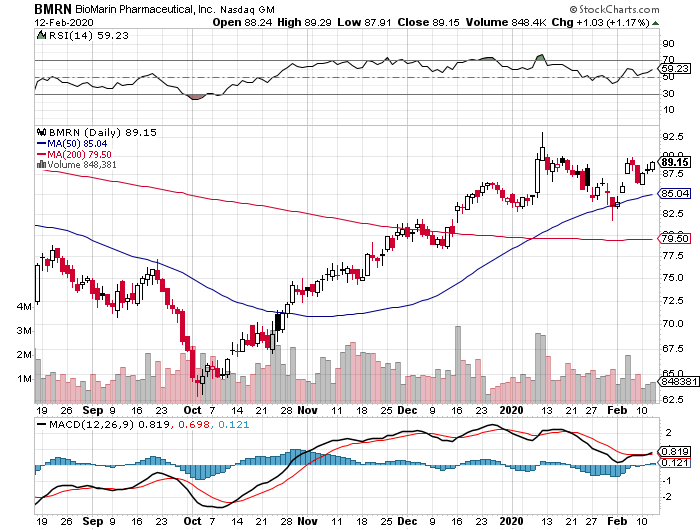

Mad Hedge Biotech & Healthcare Letter

February 13, 2020

Fiat Lux

Featured Trade:

(THE REDEMPTION OF BIOMARIN PHARMACEUTICAL)

(BMRN)

BioMarin Pharmaceutical (BMRN) has been in the doghouse in the past years, but the company is heralding 2020 as its redemption year.

This California-based biotechnology innovator has been watching its stock plummet since 2014, with the downward trend starting with BioMarin’s grand plan to find the cure for Duchenne muscular dystrophy.

This vision led to a $680 million gamble on an experimental treatment, Kydrisa. Even before the deal was finalized, however, industry experts opposed the idea like bats out of hell but BioMarin decided to go through with the ill-fated deal.

Unfortunately, the naysayers were proven right all along when the FDA rejected Kydria in 2016.

Four years after, BioMarin has come back swinging.

At the center of its redemption story are two high-value clinical assets: hemophilia gene therapy Valrox and dwarfism treatment Vosoritide.

Valrox is expected to become the most expensive drug in existence with a price tag somewhere between $2 million and $3 million. In comparison, Roche Holdings’ (RHHBY) own hemophilia A treatment, Hemlibra, costs roughly $500,000 annually.

If it receives the go-ahead from the FDA, BioMarin’s treatment will be the first-ever gene therapy available in the United States, with the company planning to target the most common types of hemophilia.

Based on the clinical trials, the patients exhibited significant improvements after the treatment. In fact, some patients had reported zero bleeding incidents for years following their first Valrox injection.

Hemophilia, which hinders a patient’s blood from clotting and causes nonstop bleeding, is known as one of the most expensive diseases to manage. At the moment, the average annual cost of hemophilia medications is $270,000 per patient. If approved, Valrox will actually be able to cut down the costs in the long run.

Barring any unforeseen roadblock, BioMarin’s hemophilia gene therapy will get the FDA green light by the third quarter of 2020.

Meanwhile, dwarfism treatment Vosoritide is now in Phase 3.

This drug is intended for children suffering from achondroplasia, which is the most widely known form of dwarfism and affects 1 in 25,000 infants. Basically, this condition is caused by an error in the patient’s gene that’s supposed to regulate bone growth, particularly in the arms and legs.

So far, BioMarin’s Vosoritide has induced faster bone growth in the patient’s bones compared to a placebo after a year of treatment.

The company plans to discuss the marketing strategy for Vosoritide in early 2021, which means the treatment will be launched in the same year.

Vosoritide is expected to rake in $700 million in peak sales.

If this also gains an FDA nod, Vosoritide will be the first-ever therapy focused on treating the underlying cause of this type of dwarfism.

In and of itself, Valrox is estimated to generate over $1.4 billion in peak sales. Vosoritide has the potential to achieve that level of blockbuster status as well simply because it will be the only approved therapy available in the market for this particular type of disease.

Taken together, both Valrox and Vosoritide have the capacity to more than double the annual revenue of BioMarin as early as 2024.

Given these expectations, the success of both drugs would catapult BioMarin to the top of the biotechnology industry and transform it into the most sought-after stock over the next decade.

So, although the company’s shares don’t exactly come cheap, this rare-disease biotech stock can still post substantial gains in 2020. After all, the primary force behind BioMarin’s growth this year is the company’s decision to create a pipeline focused on finding cures for rare, genetic conditions.

If you carefully think about it, BioMarin is actually undervalued when you consider the progress achieved by its direct competitors and the company’s near-term growth prospects.

Needless to say, BioMarin stock will be one of the red-hot commodities in a few short years.