Mad Hedge Biotech and Healthcare Letter

July 5, 2022

Fiat Lux

Featured Trade:

(AN AAA-RATED STOCK POISED TO DELIVER MARKET-BEATING RETURNS)

(JNJ), (AAPL), (GOOGL), (AMZN), (MSFT), (TSLA), (META), (BRK.A)

Mad Hedge Biotech and Healthcare Letter

July 5, 2022

Fiat Lux

Featured Trade:

(AN AAA-RATED STOCK POISED TO DELIVER MARKET-BEATING RETURNS)

(JNJ), (AAPL), (GOOGL), (AMZN), (MSFT), (TSLA), (META), (BRK.A)

More than six months after what appeared to be a never-ending assault on the biotechnology and healthcare industries, the sector seems to be slowly reviving.

While it is still too early to declare the pullback over, there are a few companies that provide a ray of hope for investors.

In the US, only four stocks have recorded a market capitalization of $1 trillion or higher: Apple (APPL), Alphabet (GOOGL), Amazon (AMZN), and Microsoft (MSFT). This year's market crash saw Tesla (TSLA) and Meta Platforms (META) departure from this elite group.

The market-wide selloff also made it more difficult for stocks to reach the $1 trillion mark. However, this does not necessarily preclude them from achieving this goal in the future.

Companies are rapidly expanding and equipped with the right tools and strategies to capitalize on growth opportunities, making them prime candidates to make the $1 trillion cut in a couple of years.

One of them is Johnson & Johnson (JNJ).

Almost everyone is familiar with JNJ's century-old brands, such as Band-Aids and Listerine. What many people probably do not realize is that the company's med-tech and pharmaceutical segments account for the vast majority of its total revenue.

In 2021, its pharmaceuticals segment alone comprised 55% of JNJ sales, while its medical devices unit contributed 29% to the company’s top line.

So far, the most promising drug in JNJ’s pharmaceutical segment is Tremfya. First-quarter sales for this psoriasis treatment jumped to a whopping 41% year over year to record an annualized $2.4 billion.

Meanwhile, JNJ's med-tech segment is poised for massive growth as a result of the strong demand for its electrophysiology products. These devices, used to keep hearts beating normally, have been identified as lucrative revenue streams and growth drivers in the long run.

The company has been working on spinning off its consumer segment into a separate publicly traded entity in the following months. This means that investors with JNJ stock will eventually end up owning shares of two different companies by 2023.

The decision to spin off its consumer health segment is part of the company's effort to shed a cyclical segment and become a health pure play focused on pharmaceuticals and medical devices.

Hence, now is an excellent time to buy JNJ shares.

While JNJ isn’t known as a high-growth stock, the company’s strategies have the potential to spur exponential growth and send shares soaring.

The next decade will be crucial for the company's success as it transforms. If the company executes its plans successfully, its current market capitalization of $467 billion could slowly but steadily increase to approximately $1 trillion.

J&J will be able to invest and concentrate its resources on segments with high sales and margins, which should increase the company's income and cash flows at a faster rate than at present.

Furthermore, JNJ's plan is expected to increase shareholder returns through higher dividends and share repurchases because of its growing cash flow. With these factors combined, JNJ's stock price will undoubtedly rise, as will its market cap.

On top of these, JNJ offers a 2.6% dividend yield. Admittedly, this isn’t remarkably high. However, investors can rely on its steady rise. Moreover, JNJ is a Dividend King. In fact, it recently raised its payout for the 60th year in a row.

If these aren’t enough to cement the company’s reputation as a solid investment, consider the fact that JNJ is one of the largest holdings in Warren Buffett’s (BRK.A) portfolio.

It’s also one of the only two publicly traded companies with the coveted AAA credit rating from S&P. For context, the US government only has an AA rating. Needless to say, this makes JNJ one of the safest—if not the safest—income stock to date.

Overall, JNJ has been diligent in getting all of its ducks in a row and is poised to provide market-beating returns to patient investors.

Mad Hedge Biotech and Healthcare Letter

February 3, 2022

Fiat Lux

Featured Trade:

(A ‘BORING’ BUSINESS RESISTING THE ‘AMAZON EFFECT’)

(CVS), (UNH), (ANTM), (TDOC), (AMZN), (BRK.A), (BRK.B), (JPM)

The healthcare market is under attack.

Amazon (AMZN) is invading the healthcare sector, wielding its far-reaching online presence and countless distribution warehouses to dominate the market.

Leveraging its ability to offer quick shipping to practically all locations, Amazon has transformed into a grab-anything-and-everything-possible business.

Now, it has set its sights on the healthcare and prescription sector. In fact, it has been attempting to infiltrate this segment since 2018 when it acquired PillPack.

The only limitation of that deal was that customers still had to get prescriptions from their doctors to avail of the PillPack service.

However, Amazon’s not the only one seeing the potential of this sector.

Following the difficulties it encountered in cornering the market, the e-commerce giant collaborated with fellow Wall Street titans Berkshire Hathaway (BRK.A) (BRK.B) and JPMorgan (JPM). Together, the three companies launched a service they called “Haven.”

Unfortunately, the venture eventually fell apart, and they canceled the deal altogether.

Despite that unfortunate end, Amazon refuses to back down on its vision. Recently, it decided to take another stab at the venture with a rebranding, giving birth to AmazonCare.

The goal is to offer assistance to customers in booking doctor appointments and receiving prescriptions online.

Undeniably, any business endeavor with Amazon’s backing will make waves in any industry. Nonetheless, this new venture could still be a tough sell.

For now, the company's strength is hoping to use the “Amazon effect” to sway members into signing up and using AmazonCare as well.

Surprisingly, Amazon finds itself facing an unlikely challenger in this pursuit: CVS (CVS).

Like Amazon, Berkshire, and JPMorgan, CVS has also recognized the potential of this market.

Unlike Amazon’s partners, CVS has decided to invest to become a frontrunner in terms of dominating the same sector and eventually taking advantage of this rapidly expanding total addressable market.

Instead of following the track of its fellow healthcare providers, such as UnitedHealth (UNH) and Anthem (ANTM), CVS has opted to change its angle of attack in the hopes of gaining more market share and reaping higher profits.

CVS is putting to good use its over 9,900 stores and distributions as means to establish better connections and rapport with customers.

After all, statistics indicate that approximately 80% of American citizens live less than 10 miles from a CVS branch.

This offers CVS a competitive advantage in terms of proximity to its customers. That is, it offers a unique convenience as it serves as the ever-present “corner stores” in practically every city.

Leveraging the locations, CVS has set up about 1,500 branches into “HealthHubs” by the end of 2021.

Basically, HealthHubs serve as emergency care clinics found inside CVS stores, providing customers with easy access to convenient and even cheaper after-hours health checkups.

Aside from this feature, a growing number of CVS stores are starting to get set up to be able to ship medicines or any other products ordered online, while other branches are being eyed as potential UPS drop-off points.

This setup will transform several branches into convenient “mini” distribution centers.

CVS has broken out of its “boring corner drugstore” image following its decision to target a more lucrative and massive healthcare sector.

It started the ball rolling when it acquired Aetna for $69 billion—a decision that so many investors disapproved of at that time.

Until recently, the market has largely ignored CVS because of the debt it incurred from the Aetna deal.

However, the tides had turned when investors finally realized that the drugstore giant had been efficiently and effectively executing a brilliant strategy all this time.

With Aetna under its wing, CVS has been granted access to a multitude of healthcare and managed care benefits availed by more than 23 million members. The sheer number of subscribers transformed the company into the third-biggest health insurer in the United States—next only to decades-long established providers Anthem and UnitedHealth.

Riding this momentum, CVS has been aggressive in revamping its image and expanding its services.

On top of its HealthHubs and Aetna advantages, CVS has recently paired up with Teladoc (TDOC) to leverage its virtual healthcare services to offer even more convenience to its customers.

This is another massive market since CVS already has roughly 35 million digital customers subscribed to its CVS app.

These users are all ordering products and other prescriptions from CVS. Integrating Teladoc’s services to the mix would be a surefire way of boosting its membership and adding a lucrative revenue stream.

Keep in mind that the global market for telehealth services is projected to expand somewhere between $300 billion to $700 billion by 2028—and that’s a conservative estimate.

CVS’ move to use Teladoc software is a positive indication of early technology adoption, positioning the drugstore chain at the forefront of a healthcare revolution.

Overall, CVS can only be described as a company striving to become a unique business that offers a range of products that no one else in the industry provides.

Although it’s improbable that it’ll sustain a monopoly in these services, CVS has been gradually transforming and growing into an almost unbeatable force in the industry by leveraging its strengths in an effective and logical method.

Moreover, it has evolved from a stodgy drugstore into an early tech adopter and a revolutionary business that can stand to challenge the likes of Amazon.

Global Market Comments

January 22, 2021

Fiat Lux

Featured Trade:

(JANUARY 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(QQQ), (IWM), (SPY), (ROM), (BRK/A), (AMZN), NVDA), (MU), (AMD), (UNG), (USO), (SLV), (GLD), ($SOX), CHIX), (BIDU), (BABA), (NFLX), (CHIX), ($INDU), (SPY), (TLT)

Below please find subscribers’ Q&A for the January 20 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, NV.

Q: What will a significant rise in long term bond yields (TLT) do to PE ratios in general, and high tech specifically?

A: Well, the key question here is: what is “significant”. Is “significant” a move in a 10-year from 120 to 150, which may be only months off? I don’t think that will have any impact whatsoever on the stock market. I think to really give us a good scare on interest rates, you need to get the 10-year up to 3.0%, and that might be two years off. We’re also going to be testing some new ground here: how high can bond interest rates go while the Fed keeps overnight rates at 25 basis points? They can go up more, but not enough to hurt the stock market. So, I think we essentially have a free run on stocks for two more years.

Q: What about the Shiller price earnings ratio?

A: Currently, it’s 34.5X and you want to completely ignore anything from Shiller on stock prices. He’s been bearish on stocks for 6 years now and ignoring him is the best thing you can do for your portfolio. If you had listed to him, you would have missed the last 15,000 Dow ($INDU) points. Someday, he’ll be right, but it may be when the market goes from 50,000 to 40,000, so again, I haven't found the Shiller price earnings ratio to be useful. It’s one of those academic things that looks great on paper but is terrible in practice.

Q: Do you see any opportunity in China financials with the change of administration, like the (CHIX)?

A: I always avoid financials in China because everyone knows they have massive, defaulted loans on their books that the government refuses to force them to recognize like we do here. So, it’s one of those things where they look good on paper, but you dig deeper and find out why they’re really so cheap. Better to go with the big online companies like Baidu (BIDU) and Alibaba (BABA).

Q: Is it too late to enter copper?

A: No, the high in the last cycle for Freeport McMoRan (FCX) was $50 dollars and I think we’re only in the mid $ ’20s now, so you could get another double. Remember, these commodity stocks have discounted recovery that hasn’t even started yet. Once you do get an actual recovery, you could get another enormous move and that's what could take the Dow to 120,000.

Q: Do you see the FANGs coming back to life with the earnings results?

A: I think it'll take more than just Netflix to do that. By the way, Netflix (NFLX) is starting to look like the Tesla of the media industry, so I’d get into Netflix on the next dip. You could get a surprise, out-of-nowhere double out of that anytime. But yes, FANGs will come to life. They've been in a correction for five months now, and we’ll see—it may be the end of the pandemic that causes these stocks to really take off. So that's why I'm running the barbell portfolio and buying the FANGs on weakness.

Q: Are you recommending LEAPS on gold (GLD) and silver (SLV)?

A: Absolutely yes, go out two years with your maturity, you might buy 120% out of the money. That's where you get your leverage on the LEAPS. Something like a (GLD) January 2023 $210-$220 in-the-money vertical bull call spread and generate a 500% profit by expiration.

Q: Do you foresee a cool off for semiconductors ($SOX) even though there's been recent news of shortages?

A: No, not really. There are so many people trying to get into these it’s incredible. And again, we may get a time correction where we sideline at the top and then break out again to the upside. This is classic in liquidity-driven markets, which is what we have in spades right now. Thanks to 5G, the number of chips in your everyday devices is about to increase tenfold, and it takes at least two years to build a new chip factory. So, keep buying (NVDA), (MU), and (AMD) on dips.

Q: Where are the best LEAPS prospects (Long Term Equity Participation Securities)?

A: That would have to be in technology—that's where the earnings growth is. If you go 20% out of the money on just about any big tech LEAPs two years out, to 2023 those will be worth 500% more at expiration.

Q: What about SPACs (Special Purpose Acquisition Company) now, as we’re getting up to five new SPACs a day?

A: My belief is that a SPAC is a vehicle that allows a manager to take out a 20% a year management fee instead of only 1%. And it's another aspect of the current mania we’re in that a lot of these SPACs are doubling on the first day—especially the electric vehicle-related SPACs. Also, a lot of these SPACs will never invest in anything, but just take the money and give it back to you in two years with no return when they can't find any good investments…. If you’re lucky. There's not a lot of bargains to be found out there by anyone, including SPAC managers.

Q: Does natural gas (UNG) fall into the same “avoid energy” narrative as oil?

A: Absolutely, yes. The only benefit of natural gas is it produces 50% less carbon dioxide than oil. However, you can't get gas without also getting oil (USO), as the two come out of the pipe at the same time; so I would avoid natural gas also. Gas and oil are also about to lose a large chunk, if not all, of their tax incentives, like the oil depletion allowance, which has basically allowed the entire oil industry to operate tax-free since the 1930s.

Q: What about hydrogen cars?

A: I don't really believe in the technology myself, and when you burn hydrogen, that also produces CO2. The problem with hydrogen is that it’s not a scalable technology. It’s like gasoline—you have to build stations all over the US to fuel the cars. Of course, it produces far less carbon than gas or natural gas, but it is hard to compete against electric power, which is scalable and there's already a massive electric grid in place.

Q: If you inherited $4 million today, would you cost average into (QQQ), (IWM), or (SPY)?

A: I would go into the ProShares Ultra Technology ETF (ROM), which is double the (QQQ); and if you really want to be conservative, put half your money into (QQQ) or (ROM), and then half into Berkshire Hathaway (BRK/A), which is basically a call option on the industrial and recovery economy. I know plenty of smart people who are doing exactly that.

Q: Is it weird to see oil, as well as green energy stocks, moving up?

A: No, that's actually how it works. The higher oil and gas prices go, the more economical it is to switch over to green energy. So, they always move in sync with each other.

Q: I heard rumors that Amazon (AMZN) is likely to raise Prime’s annual fee by $10-20 a year in 2021. Will that be a catalyst for the stock to go higher?

A: Yes. For every $10 dollars per person in Prime revenue, Amazon makes $2 billion more in net profit. I would say that's a very strong argument for the stock going up and maybe what breaks it out of its current 6-month range. By the way, Amazon is wildly undervalued, and my long-term target is $5,000.

Q: Do you think that the spike in Apple (AAPL) MacBook purchases means that computers will overtake iPhones as the revenue driver for Apple in 2021, or is the phone business too big?

A: The phone business is too big, and 5G will cause iPhone sales to grow exponentially. Remember, the iPhones themselves are getting better. I just bought the 12G Pro, and the performance over the old phone is incredible. So yeah, iPhones get bigger and better, while laptops only grow to the extent that people need an actual laptop to work on in a fixed office. Is that a supercomputer in your pocket, or are you just glad to see me?

Q: Share buybacks dried up because of revenue headwinds; do you think they will come back in a massive wave, giving more life to equities?

A: Absolutely, yes. Banks, which have been banned from buybacks for the past year, are about to go back into the share buyback business. Netflix has also announced that they will go buy their shares for the first time in 10 years, and of course, Apple is still plodding away with about $100 or $200 million a year in share buybacks, so all of that accelerates. The only ones you won't see doing buybacks are airlines and Boeing (BA) because they have such a mountain of debt to crawl out from before they can get back into aggressive buybacks.

Q: Interest rates are at historic lows; the smartest thing we can do is act big.

A: That’s absolutely right; you want to go big now when we’re all suffering so we can go small later and run a balanced budget or even pay down national debt if the economy grows strong enough. The last person to do that was Bill Clinton, who paid down national debt in small quantities in ‘98 and ‘99.

Q: What do you think about General Motors (GM)?

A: They really seem to be making a big effort to get into electric cars. They said they're going to bring out 25 new electric car models by 2025, and the problem is that GM is your classic “hour late, dollar short” company; always behind the curve because they have this immense bureaucracy which operates as if it is stuck in a barrel of molasses. I don’t see them ever competing against Tesla (TSLA) because the whole business model there seems like it’s stuck in molasses, whereas Tesla is moving forward with new technology at warp speed. I think when Tesla brings out the solid-state battery, which could be in two years, they essentially wipe out the entire global car industry, and everybody will have to either make Tesla cars under license from Tesla—which they said they are happy to do—or go out of business. Having said that, you could get another double in (GM) before everyone figures out what the game is.

Q: Will you update the long-term portfolio?

A: Yes, I promise to update it next week, as long as you promise me that there won’t be another insurrection next week. It’s strictly a time issue. After last year being the most exhausting year in history, this year is proving to be even more exhausting!

Q: Do you see a February pullback?

A: Either a small pullback or a time correction sideways.

Q: Do you think the Zoom (ZM) selloff will continue, or is it done now that the pandemic is hopefully ending?

A: It’s natural for a tech stock to give up one third after a 10X move. It might sell off a little bit more, but like it or not, Zoom is here to stay; it’s now a permanent part of our lives. They’re trying to grow their business as fast as they can, they’re hiring like crazy, so they’re going to be a big factor in our lives. The stock will eventually reflect that.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

December 1, 2020

Fiat Lux

FEATURED TRADE:

(BET LIKE WARREN BUFFETT)

(MRK), (BRK.A), (AAPL), (JPM), (GILD), (PFE), (ABBV)

Warren Buffett’s moves via Berkshire Hathaway (BRK.A) showed some telling signs this third quarter.

For one, the Oracle of Omaha has surprisingly trimmed his holdings in Apple (AAPL) and even JPMorgan Chase (JPM).

Another telltale sign that change is coming can be seen in his positions in biopharmaceutical titans.

Let’s take a closer look at one of the three biggest biopharma investments of Berkshire to date: Merck.

While the New Jersey-based pharmaceutical titan has not been as widely reported as its counterparts in the COVID-19 race, Merck has actually been working on a promising coronavirus program.

In fact, the company is part of the first five COVID-19 programs included in Donald Trump’s Operation Warp Speed.

Just last week, the company added another promising COVID-19 treatment to its pipeline via the $425 million cash acquisition of Oncolmmune—a move that would give Merck access to the privately-owned company’s COVID-19 treatment, called CD24Fc.

If successful, CD24Fc will be a powerful treatment for mild to severe cases of COVID-19.

To date, only Gilead Sciences’ (GILD) Veklury has received FDA approval and even that treatment failed to address all the health concerns.

In comparison, CD24Fc is expected to undergo a smooth sailing journey from clinical trials to its market launch in 2021.

Meanwhile, Merck may have another ace in the hole with its COVID-19 program.

While the company is already months behind the frontrunners, Merck has a competitive advantage over the COVID-19 vaccine candidates submitted by Pfizer (PFE), Moderna (MRNA), and even AstraZeneca (AZN).

Its experimental COVID-19 vaccine does not require any freezing.

This means that unlike the candidates of Pfizer and Moderna, Merck’s vaccine does not need ultra-special handling and transportation.

On top of that significant advantage, Merck has been working with the nonprofit organization International AIDS Vaccine Initiative to develop a COVID-19 vaccine that only requires a single dose.

In contrast, the leading candidates today require two shots of their vaccines to become effective.

Apart from betting big on its COVID-19 program, Merck is also upping the stakes in its oncology pipeline.

Its recent move is the $2.75 billion acquisition of VelosBio—a partnership that adds another potent arrow to Merck’s already powerful quiver of cancer drugs.

This deal with VelosBio provides Merck with access to cancer treatments under development. Most of these home in on the deadly cancer cells but manage to spare the patients from several horrible side effects.

Prior to this, Merck shelled out $1 billion to gain an equity stake in Seagen (SGEN). The deal also grants Merck access to an extensive antibody drugs pipeline.

Aside from its oncology-related acquisitions—all of which have been home runs for its investors—Merck’s existing cancer pipeline has been consistent moneymakers.

Apart from lung cancer treatment Keytruda, which generated a whopping $11.9 billion in sales in 2019 alone, Merck has a virtually unbeatable arsenal against cancer.

In fact, its thyroid cancer drug Lenvima, which was initially approved for thyroid cancer in 2015, already expanded its indications to cover renal cell carcinoma and potentially even melanoma, endometrial cancer, NSCLC, and bladder cancer.

This could bring Keytruda-like success for Merck in the future.

Aside from Merck, Warren Buffett also invested in biopharmaceutical titans Pfizer and AbbVie.

As of September, Berkshire Hathaway holds 3.7 million Pfizer shares, 21.3 million AbbVie shares, and 22.4 million Merck shares.

These moves are especially noteworthy since the company has not owned any of these biopharma giants at the end of June.

Looking at the profile of these companies, there is no obvious connection or theme.

As discussed, Merck is heavily investing in its oncology pipeline.

AbbVie has been busy diversifying and building a pipeline independent from its megablockbuster Humira.

In fact, this biopharmaceutical giant has delved into dermatology with its massive acquisition of Allergan, aka the Botox-maker.

Meanwhile, Pfizer has been in the news thanks to its COVID-19 vaccine.

Aside from its coronavirus program, Pfizer has been focused on completing the merger between its Upjohn unit and generic drugmaker Mylan (MYL) to form a new company, called Viatris.

Analyzing all three closely though, one thing becomes clear: They are trading off their all-time highs and have been doing it for the entire 2020.

Do you know what that means?

Warren Buffett has been bargain shopping.

Global Market Comments

May 11, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEXT GOLDEN AGE HAS ALREADY STARTED)

(TLT), (TBT), (SPY), (INDU), (VIX),

(DAL), (BRK/A), (LUV), (AA), (UAL)

I always get my best ideas when hiking up a steep mountain carrying a heavy backpack.

Yesterday, I was just passing through the 9,000-foot level on the Tahoe Rim Trail when suddenly, the fog lifted and the skies cleared. I was hit with an epiphany.

It was my “AHA” moment.

The next American Golden Age, the next Roaring Twenties, started on March 23.

However, you have to dive deep into investor psychology to reach that astonishing conclusion.

The conundrum of the day is why stocks are trading at a plus 30X multiple two months into a Great Depression. The economic data has been so horrific that the mainstream news has been reporting them.

Some 30 million unemployed on the way to 51 million? Those are Fed numbers, not mine (click here for the link ). Over 52% of small businesses going bankrupt in the next six months? A GDP that is shrinking at an amazing -40% annualized rate?

Yet, we have a Dow Average that has risen a breathtaking 38% in six weeks. The market has essentially dropped 38% and risen 38% over three months, with the Volatility Index (VIX) making a brief visit to the $80 handle.

To understand these massive contradictions, you have to understand what investors think they are buying. They are not hoovering up stocks that are cheap, offer value, or at the bottom of an economic cycle.

Instead, they are investing in a hope, a vision, an expectation that the coming decade will bring a major economic boom. Yes, they are buying my coming American Golden Age.

Only 10% of the value of a stock is reflected in current year earnings, according to Dr. Jeremy Siegal at the Wharton School of Economics (click here to go to the site). The other 90% is in the following nine years. Investors have written off this year’s earnings and are paying up for the following nine.

Long term followers of this newsletter are well aware of my approaching forecast of the next Roaring Twenties (click here for the link).

Except that this time we have a catapult, the pump-priming effects of the pandemic. The government has stepped in with $14 trillion worth of fiscal and monetary stimulus. Creative destruction is taking place at an exponential rate. Companies have to become hyper-efficient overnight or die.

It’s not rocket science. More than 85 million millennials are aging into their peak spending years, buying homes, cars, and all the luxuries of life. Every time this has happened for the past century, US economic growth leaped to 4%.

It happened in the 1920s, the 1960s, the 1990s, and is about to take place in the 2020s. And with each pop in growth, the stock market rises about 400%. Look at your long-term charts and you’ll see I’m dead right.

That takes us from the March 23 Dow Average low at 18,000 up to 72,000 by 2030, except that it’s a low number. Throw in the hyper-acceleration of innovation by the technology and biotech sectors, a Dow 120,000 is within reach.

You may recall that number from my marketing pitches, except that this time it’s happening. In a decade you are going to look like an absolute genius by following the recommendation of the Mad Hedge Fund Trader.

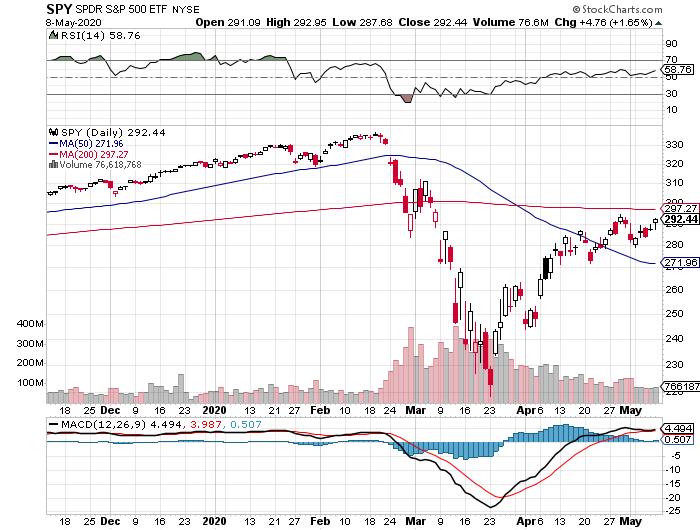

It also means that we may not see market corrections of any more than 10% this year. That would take us down to a Dow Average of 22,500, and an (SPX) of 2,600 in the coming months. That’s where you should jump in and buy with both hands. The only way I would be wrong is if the US epidemic explodes to unimaginable levels, which is not impossible.

Last week, U-6 unemployment rates exploding to a stratospheric 22.8%. The rate was far higher among high school graduates, but only 8% for college grads. Some 20.2 million lost jobs, ten times the previous record, and more than seen during the Great Depression. The BLS (click here) said the true figure was probably 5% higher due to counting anomalies and a huge backlog of data. And this is just the beginning. The good news is that next month, only 10 million jobs will be lost.

NASDAQ (QQQ) turned positive for 2020, and the followers who piled into tech LEAPS at the March bottom are eternally grateful. Tech and biotech are the only places to be. Everywhere else is a waste of time and money. The entire country is turning into a tech economy or going out of business. Buy tech on dips.

Warren Buffet sold all his airline shares, taking a major loss, including Delta (DAL), Southwest (LUV), American (AA) and United (UAL). The Fed’s $50 billion airline bailout blocked him from making a real killing. His Berkshire Hathaway (BRK/A) (click here) owned close to 10% of all of them. The complete collapse of tourism and business travel are the issues. He sees no recovery in the foreseeable future. They don’t call him the “Oracle of Omaha” for nothing.

US Auto Sales are down a mind-blowing -48% in April, the worst on record. Only 8.6 million cars were sold in the US against last year’s annual rate of 17 million. Toyota and Honda saw the biggest falls as their ships can’t unload due to lack of storage space.

The US Treasury will borrow $3 Trillion this Quarter to fund the massive bailout programs. Announced programs amount to 20 times the $789 billion 2009 rescue package, which Republicans opposed. I’m increasing my bond shorts. Sell short (TLT) again, even if we don’t get a decent rally. Oh, and Trump is threatening a default too. He doesn’t see the connection.

Bonds crashed on massive issuance, with the Treasury announcing a record 20-year bond floatation. Yields hit a one-month high. With the (TLT) down $18 from its recent high, I am taking profits on my bond shorts. I’ll be selling the next rally….again. This could be my core trade for the next decade.

Consumer Debt soared to $14.3 trillion in Q1, a new all-time high. A lot of people are living on their credit cards right now.

Trump threatens to cancel China trade deal, blaming them for Covid-19, sending stocks into a 400-point dive. The last time he did this, shares plunged 20%. It’s all part of an effort to divert attention from the administration’s disastrous handling of the pandemic. America’s Corona deaths are now 20 times China’s, and they are still an emerging nation. Just what we needed, a renewed trade war on top of a pandemic-caused Great Depression, as if the market needed more uncertainty. Sell rallies in the (SPY)

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years again, up a gob-smacking +6.46%. We are now only 0.65% short of a new all-time high.

My aggressive short bond positions came in big time on the back of theannounced $3 trillion in new debt issuance in Q2. Short bonds are far and away the better quality trade of buying stocks at these elevated levels.

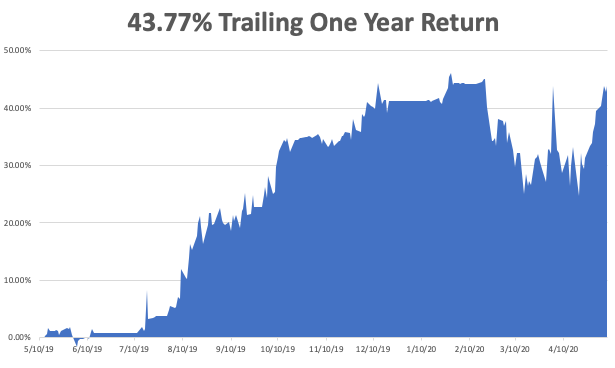

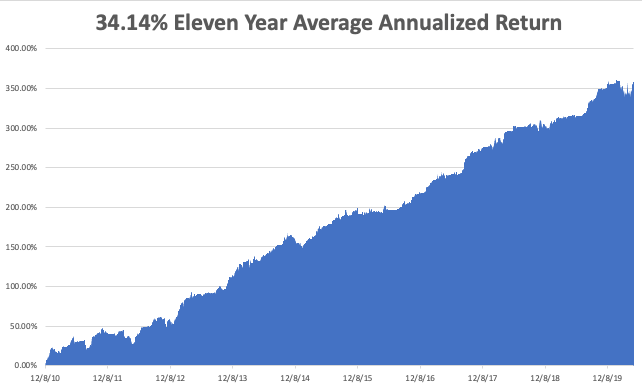

May is up +6.46%, taking my 2020 YTD return up to 2.59%. That compares to a loss for the Dow Average of -13.43% from the February top. My trailing one-year return exploded to 43.77%. My ten-year average annualized profit returned to +34.14%.

This week, Q1 earnings reports continue, and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

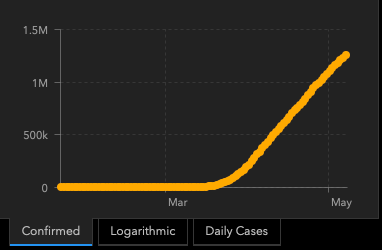

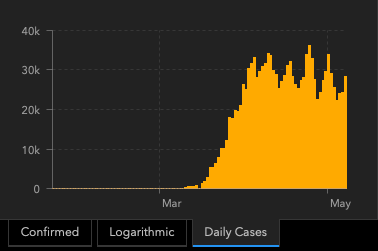

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 11 at 10:00 AM, the April US Inflation Expectations are out. Caesar’s Entertainment (CZR) and Marriot International (MAR) report earnings.

On Tuesday, May 12 at 5:00 PM, the NFIB Small Business Optimism Index for April is released. Toyota Motors (TM) reports earnings.

On Wednesday, May 13 at 9:30 AM, the ever fascinating weekly Cushing Crude Oil Stocks is announced. Cisco Systems (CSCO) reports earnings.

On Thursday, May 14 at 8:30 AM, we get another blockbuster Weekly Jobless Claims. Advanced Micro Devices (AMD) reports earnings.

On Friday, May 15 at 7:30, AM the Empire State Manufacturing Index is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll continue my solo circumlocution of the 160 mile Tahoe Rim Trail every afternoon in ten-mile segments. Why solo? Do you know anyone else who wants to hike 160 miles at 10,000 feet in two weeks?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader