Mad Hedge Biotech & Healthcare Letter

November 5, 2020

Fiat Lux

FEATURED TRADE:

(IT’S GO TIME FOR BIOGEN’S ALZHEIMER’S DRUG)

(BIIB), (LLY), (AXSM), (MYL)

Mad Hedge Biotech & Healthcare Letter

November 5, 2020

Fiat Lux

FEATURED TRADE:

(IT’S GO TIME FOR BIOGEN’S ALZHEIMER’S DRUG)

(BIIB), (LLY), (AXSM), (MYL)

Investing in beaten-up stocks in this period of uncertainty demands nerves of steel.

In fact, some biotechnology and healthcare stocks have been left for dead in recent months. Meanwhile, there are others that continue to deliver amidst the ongoing pandemic.

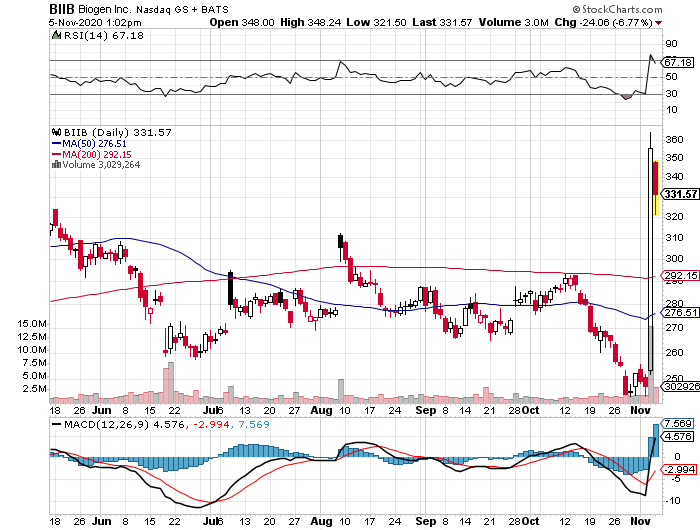

One of them is Biogen (BIIB).

Biogen has been consistently tagged as a high-risk-high-reward stock even before the COVID-19 pandemic started.

However, people seem to miss the fact that the company has relatively low debt and a surprisingly positive free cash flow in the past years.

Since 2019, the banner headline for Biogen has been its experimental Alzheimer’s disease treatment Aducanumab.

Recently, Biogen released promising progress following its decision to submit the Alzheimer’s candidate for a priority review to the FDA. It has also been accepted for review by European health regulators.

Although this move appears risky, the goal is to accelerate FDA’s timeline for Aducanumab.

That is, Biogen’s decision to submit the drug for approval earlier than expected also pushes the decision to an earlier date, which is March 7, 2021.

If approved, then Aducanumab will be the first-ever approved drug for Alzheimer’s disease.

The road to this point was not easy though. Biogen went through a series of failed trials and even a brief period of giving up on the project before the company gave the effort another chance.

Looking at the market opportunity for this sector, Biogen’s about-face no longer comes as a surprise.

For decades now, companies have been looking into ways to at least slow the progress of the condition, treat the symptoms, and offer faster ways to diagnose it.

There is currently no cure for this disease, which is ranked as the sixth leading cause of death in the country and accounts for approximately 2 million deaths globally.

Given that this disease takes years to progress, it means tens of millions of patients live with the condition on a daily basis -- and this sector comprise the target niche for Aducanumab.

In the United States alone, over 5 million people are diagnosed with Alzheimer’s disease annually and this number is projected to increase to nearly triple by 2050.

With all the treatments geared towards Alzheimer’s disease, sales for these products were estimated at $3.5 billion in 2018. This cost is expected to hit a 7.2% compound growth rate yearly until 2030.

If successful, Aducanumab can reach peak sales somewhere between $10 billion and $20 billion.

For context, the annual sales of Biogen today is only under $15 billion.

This underscores the significance of Aducanumab for the company as the drug can more than double its total earnings and even its market capitalization. It can also offer a 3x to 4x jump in Biogen’s share price.

Apart from Biogen, other big names working on an Alzheimer’s treatment are Eli Lilly (LLY) and Axsome Therapeutics (AXSM).

Outside Biogen’s work on Aducanumab, the company also has an impressive asset portfolio.

Its second quarter earnings results for 2020 showed that revenues from its multiple sclerosis drug segment contributed significantly to the company’s profits, with Ocrevus raking in $2.3 billion for the period.

The newly acquired rare spinal muscular atrophy disease drug Spinraza also performed well, reporting approximately $2 billion in annual sales.

Even its embattled multiple sclerosis treatment Tecfidera, which has been facing patent exclusivity issues with generic companies like Mylan (MYL), reported an increase from its notable $1 billion in revenue for the first quarter of the year to $1.2 billion in the second quarter.

Finally, Biogen has been working on expanding its biosimilar segment to increase its competitive advantage particularly for its drugs that are nearing the end of their patent exclusivity.

Amid the pandemic, Biogen’s revenue was up by 1% to hit $3.5 billion in the first quarter of 2020 and increased by 2% to reach $3.7 billion in the second quarter.

The company’s financial results also rose by approximately $100 million in the first three months of this challenging year.

However, a widely known caveat not only for Biogen but also for a number of biotechnology companies is the volatility of the stocks.

There is no one-size-fits-all formula for investing in beaten-up stocks. It comes with zero guarantees that their past performances would make a repeat either.

The strategy for these things though is quite basic. Make sure to look at businesses that offer sufficient bandwidth to bounce back once things normalize and the effects of the pandemic start to ease.

Looking at its overall performance, Biogen has achieved an impressively strong financial position despite the setbacks along the way. The company even offers room for growth regardless of the performance of its much-awaited Aducanumab.

Mad Hedge Biotech & Healthcare Letter

September 1, 2020

Fiat Lux

Featured Trade:

(RACE TO THE FINISH LINE)

(PFE), (BNTX), (MRNA), (AZN), (INO), (ZTS), (MYL)

One of the leading companies in the COVID-19 vaccine race is getting closer to the finish line.

Pfizer (PFE) shocked the scientific community when it announced that it would be ready to submit its COVID-19 vaccine candidate, BNT162b2, for FDA approval by October.

The company said that it is now more than 50% done with the recruitment for its Phase 3 clinical trial, which requires 30,000 volunteers.

Earlier this year, Pfizer and its vaccine partner BioNTech (BNTX) were included in the US government’s Operation Warp Speed project. Although the two rejected government funding, their candidate is still included in the fast-track priority list of the FDA.

To date, the US government already secured a contract with Pfizer and BioNTech for 600 million doses of their vaccine, with the initial payment of $1.95 billion for the first 100 million doses.

Other countries across the globe have also shown faith in the science of Pfizer.

The UK government completed a deal with Pfizer for 30 million doses, while Japan ordered 120 million doses.

Since it has been preparing its manufacturing facilities while also conducting its trials, Pfizer is confident that it can produce 1.3 billion doses of BNT162b2 in 2021.

Given this timeline, it is possible for the company to launch its COVID-19 vaccine to the market by the fourth quarter of 2020, with peak sales of the product reaching $1.7 billion in 2021.

Revenue for BNT162b2 is expected to slide to $850 million by 2023, with the vaccine raking in an average of $500 million to $600 million in annual sales by then.

However, there is no such thing as a perfect solution.

A potential competitive disadvantage of Pfizer’s vaccine candidate lies in its storage requirements, which entail a storage temperature of −94°F.

While tertiary hospitals and laboratories can meet this requirement, it would make it difficult for traditional offices or pharmacies to store the product.

This shortcoming might prompt other governments and private institutions to consider other vaccine candidates with simpler storage requirements.

Although the results have yet to be released, early data show that competitors like Moderna (MRNA), AstraZeneca (AZN), and Inovio Pharmaceutical (INO) might offer less complicated solutions.

Outside its widely publicized COVID-19 vaccine efforts, Pfizer has been working on additional spinoffs to boost and diversify its revenue stream.

Investors of the company would agree that Pfizer is the kingpin of spinoffs.

A prime example of this is its animal healthcare Zoetis (ZTS) spinoff, which was established in 2013. Since then, the investors have experienced impressive returns with over 289% yields.

Now, Pfizer is aiming to replicate this feat with the $195 billion merger of its own off-patent and generic drugs unit Upjohn with Pennsylvania-based company Mylan (MYL).

The two companies are slated to form a mega-company, called Viatris, where Pfizer stakeholders will also receive shares.

Looking at its portfolio and pipeline candidates, Viatris is projected to generate approximately $19 billion to $20 billion in annual revenue and record $4 billion in free cash flow.

On top of the Viatris spinoff, Pfizer is also working on the Nasdaq IPO of Cerevel Therapeutics.

This is an interesting move from Pfizer since Cerevel is a neuroscience company, which focuses on diseases of the central nervous system like Alzheimer’s, Parkinson’s, and epilepsy.

Pfizer owns 25% stake of the neuro company while Bain Capital holds 75%. The two established Cerevel in 2018.

Just last July, Cerevel announced its merger with Arya Sciences Acquisition Corp II.

When the merger is finalized, the new company will be called Cerevel Therapeutics Holdings and will be under the ticker symbol “CERE” in Nasdaq. The deal is expected to be completed by the fourth quarter of 2020.

Although it will be a relatively unknown and new company, Cerevel is expected to receive at least $445 million to use for its growth by the end of the year.

Needless to say, this is expected to be another “Zoetis-in-the-making” strategy from Pfizer.

For 2020, Pfizer raised its revenue guidance and estimates that it can generate somewhere between $48.6 billion and $50.6 billion while recording an earnings per share of roughly $2.85 and $2.95.

Looking at its balance sheet, Pfizer has proven itself capable of weathering one of the most debilitating downturns since The Great Depression.

In fact, the company amassed revenue of $12 billion and showed off a respectable 12% operational growth in its biopharma unit in the first three months of this year.

In its second quarter earnings report, when the COVID-19 pandemic was already well underway, Pfizer raked in $11.8 billion in revenue.

With all the publicity surrounding the COVID-19 vaccine efforts, it is understandable that investors are buying at artificially high prices. However, Pfizer remains incredibly undervalued.

Pfizer’s star power would inevitably surge if BNT162b2 proves to be safe and effective. Even without the vaccine though, the company’s diverse portfolio and impressive acquisition strategies already make it a great buy.

Plus, its healthy dividend, which yields approximately 3.9%, is no doubt the icing on the cake for this incredibly undervalued stock.

Mad Hedge Biotech & Healthcare Letter

July 14, 2020

Fiat Lux

Featured Trade:

(GILEAD SCIENCES REMDESIVIR MIRACLE)

(GILD), (RHHBY), (LLY), (MYL)

Gilead Sciences (GILD) has been in the spotlight for months now. The company gained even more attention when the FDA granted it emergency authorization to use its drug Remdesivir as a COVID-19 treatment.

To date, there are roughly 20 clinical trials for Remdesivir across the globe --- and Gilead is wasting no time to expand the use of this drug.

In a recent announcement, the company shared that Remdesivir will also be tested as an inhaled formulation for outpatients.

To compare, the drug is currently given in intravenous form to patients who are already considered severe cases. This latest iteration of the drug could offer a COVID-19 treatment to those with mild cases which could eventually lead to early treatment of the disease, making hospitalization unnecessary.

At the moment, Remdesivir shortens the recovery period of hospitalized COVID-19 patients by four days or roughly 31%.

Gilead will test this inhaled formulation of Remdesivir on 60 healthy participants in the US.

Aside from testing its inhaled formulation, the company is also planning to test an IV version of Remdesivir. This could be used for outpatient settings, such as nursing homes and infusion centers.

There are also trials to determine whether the efficacy level of Remdesivir could increase if combined with other drugs. For this, Gilead is working with Roche (RHHBY) for its Actemra and Eli Lilly (LLY) to test Olumiant. Both are used to treat rheumatoid arthritis.

Since the pandemic started and Gilead’s COVID-19 efforts, the company’s shares jumped by 17.5% so far, topping the 2% decline of the S&P 500 Index.

A notable factor that has been fueling Gilead’s improvement is the US government’s confidence in Remdesivir.

In early July, the Department of Health and Human Services all but wiped clean the company’s Remdesivir supply as it contracted Gilead to sell 500,000 treatment courses to US hospitals through the end of September.

This purchase adds up to $1.2 billion in Remdesivir sales in the third quarter of 2020 alone, with the drug estimated to generate $1.8 billion in the fourth quarter.

This puts the estimated total sales of Remdesivir at $3 billion for this year.

The company set the price for each course of Remdesivir treatment at $2,340 for the government, with a price tag of $3,120 for private US insurers. At this price point, every patient is estimated to save $12,000 in hospital bills.

This is actually lower than the anticipated pricing of Remdesivir. Initially, the cost per treatment course was projected to reach $5,080.

However, this pricing estimate is intended for developed countries.

For developing countries, Gilead forged deals with various generic manufacturers to ensure that the treatment is provided at substantially lower prices.

So far, the company has established licensing deals with generic drugmakers in 127 developing countries.

One of them is Mylan N.V. (MYL), which has received authorization from the Indian government to market its generic version of the Remdesivir.

Mylan’s version, which will be sold under the brand name Desrem, is expected to be around $62.40 per vial.

This is about 80% cheaper than Gilead’s Remdesivir, which costs $390 for each vial.

Outside its COVID-19 efforts, Gilead’s FDA application for rheumatoid arthritis drug Filgotinib is expected to inject the company’s top line with a much-welcomed sales growth.

Although Gilead’s 2019 top line fell flat, its first-quarter earnings report showed a promising 5% year-over-year bump in its sales. This growth is primarily attributed to the continuous improvement of its HIV product line, which showed a 14% increase in sales.

Overall, Gilead remains a value buy.

Gilead stock currently trades at 11.6 times its expected earnings over the course of the next 12 months, which is well above its average 7.3 times earnings.

The stock offers a quarterly dividend of $0.68, yielding a reasonable 3.5% annually. As modest as it sounds, this still well above the usual 2% that shareholders typically expect from an average stock.

![]()

Mad Hedge Biotech & Healthcare Letter

June 9, 2020

Fiat Lux

Featured Trade:

(HERE ARE FIVE VACCINE FRONTRUNNERS TO BUY NOW)

(MRNA), (AZN), (JNJ), (MRK), (PFE), (GSK), (SNY), (NVAX), (INO), (MYL)

Among hundreds of companies working on a coronavirus disease (COVID-19) vaccine, the US Government has picked five companies as the most likely candidates to develop the much-needed immunization shot soon.

This is a part of a process that usually takes years and even decades to complete. The goal is to have a COVID-19 vaccine available for Americans by January 2021.

The decision to winnow the field even before final results are out is the administration’s way of focusing its energy and resources on the most promising vaccine candidates, thereby coming up with a solution faster.

Four of the five companies are based in the United States and one is from the United Kingdom.

The list includes Massachusetts-based biotechnology firm Moderna (MRNA), which has a market capitalization of $22.63 billion.

It also features biotechnology and healthcare giants Johnson & Johnson (JNJ), with its $388.08 billion market cap; Merck & Co. (MRK), which has $207.63 billion in market cap, and Pfizer (PFE), with a market cap of $199.92 billion.

Cambridge-based pharmaceutical and biopharmaceutical company AstraZeneca rounds up the list.

Both Moderna and AstraZeneca are already in Phase 2 trials, which means the companies are testing their candidates on human subjects.

Looking at their timeline, the two would most likely move forward to Phase 3, which involves large-scale human trials, in July.

The Phase 3 trials will require roughly 30,000 participants for each vaccine candidate. If all five vaccine candidates reach Phase 3, then that means 150,000 people will be asked to participate as test subjects.

What we do know so far is that the agreements involve commitments from the biotechnology companies regarding intellectual property, the number of doses expected, and the estimated price limits.

Here’s a brief background of the top five companies under Trump’s COVID-19 vaccine radar today.

Moderna (MRNA)

Moderna’s vaccine, called mRNA1273, is undergoing Phase 2 trials. When news broke about Moderna’s progress with the COVID-19 vaccine, shares of the company exploded by more than 200% year-to-date.

For its Phase 2 trial, Moderna seeks to enroll 600 healthy individuals to test mRNA-1273 administered 28 days apart.

Throughout the COVID-19 crisis, Moderna has been a clear favorite of NIH’s Dr. Anthony Fauci.

He called the vaccine “quite promising” and described the results of the Phase 1 study to be “better than we thought.” What we know about the vaccine is that it can “neutralize” the virus in patients.

In terms of its release, Moderna is projected to deploy mRNA-1273 by the end of 2020.

AstraZeneca (AZN)

AstraZeneca joined forces with Oxford University to develop AZD1222, which is now undergoing clinical trials in many sites in the UK.

Although the two have yet to complete its trials, AstraZeneca already agreed to supply 400 million vaccine doses to both the US and the UK in May.

Earlier this month, the company again completed a $750 million agreement with the Coalition for Epidemic Preparedness Innovations (CEPI), Gavi the Vaccine Alliance, and the Serum Institute of India (SII) to provide 1 billion vaccine doses to low and middle-income patients.

Johnson & Johnson (JNJ)

Johnson & Johnson aims to begin its Phase 1 clinical trial by September, with the ultimate goal to supply over 1 billion doses of COVID-19 vaccine across the globe.

Although Moderna and AstraZeneca are ahead in terms of vaccine development, JNJ has been impressing investors with its efforts outside COVID-19.

In the first quarter of 2020, the healthcare giant showed off a 3.3% year-over-year jump in its sales and a 54.6% increase in its net earnings.

The revenue of its pharmaceutical division rose by 8.7% while its health division saw a 9.2% increase.

Dubbed as the “Dividend King” in the industry, JNJ stayed true to its title as it continues its 58-year streak of raising its quarterly dividend.

Reports show that the company raised its quarterly dividend by 6.3% to reach $1.01 per share, reaping a solid yield of 2.73%.

Regardless of its performance in the vaccine race, JNJ has proven its resilience not only in the COVID-19 crisis but also in past crises like the dot-com bubble and the collapse of the housing market.

Merck (MRK)

Merck’s strategy is to build on the technology of its successful Ebola vaccine and establish partnerships with non-profit research groups.

Like JNJ, Merck is also a stable dividend stock that investors can buy and hold for years. In the past 10 years, this biotechnology leader has posted a profit, even managing to hit double-digits the majority of the time.

This is a trend Merck once again showcased in the first quarter of 2020.

In its latest report, the company showed off $3.2 billion in profit in sales worth $12.1 billion — demonstrating a decent profit margin of 27%.

Sales increased by 11% year over year, with cancer drug Keytruda heading the charge with its 45% revenue growth from the same period in 2019.

Pfizer (PFE)

Pfizer has been collaborating with German drugmaker BioNTech (BNTX) to develop BNT162.

The pharma giant is expected to have the vaccine candidate ready by October this year and be able to produce “hundreds of millions” of COVID-19 doses by 2021.

Although Pfizer and BioNTech joined the race later than Moderna, the big healthcare company’s edge is that it’s actually working on four vaccines simultaneously.

Simply put, this strategy offers them more than a single change of winning.

Along with the other three big biotechnology companies, Pfizer is a safe bet for those looking to invest in cutting-edge vaccine efforts but don’t feel comfortable risking it with a clinical-stage firm.

Like JNJ and Merck, Pfizer’s vaccine work sounds promising, but even if its COVID-19 program falters, the healthcare giant can still make a strong case as an excellent investment.

In its first-quarter report for 2020, Pfizer’s biopharma arm indicated an 11% jump, thanks to top performers like blood clot treatment Eliquis whose sales climbed by 29% to reach $1.3 billion.

Breast cancer medication Ibrance also contributed $1.2 billion, showing off a 10% year-over-year growth while Xtandi sales increased by 25% year over year to record $209 million.

Aside from these, Pfizer is hard at work in spinning off its Upjohn unit to combine with Mylan (MYL). This deal will guarantee Pfizer shareholders with 57% share of the new company called Viatris.

Just a few weeks ago, Trump compared Operation Warp Speed to the Manhattan Project, which was a government-initiated program that led to the development of nuclear weapons in World War II.

However, critics say that the “Skunk Works” initiative in California is a more fitting comparison for this COVID-19 effort. That is, the government could simply be wasting its resources on candidates that might never be able to leave the design stage.

Regardless of where you stand on Trump’s Operation Warp Speed, the fact remains that countless biotechnology and healthcare companies — big and small — are working on a COVID-19 vaccine.

Outside the five companies chosen by the Trump administration, the list of strong contenders includes GlaxoSmithKline (GSK) and Sanofi (SNY).

Even smaller biotechnology companies like Inovio (INO) and Novavax (NVAX) are going all out on this.

Of course, it would also be foolish to completely disregard CanSino Biologics, which has been giving Moderna a run for its money since Day 1.

Despite not making the cut, these biotechnology and healthcare companies are still in hot pursuit and it’s still very much a neck-to-neck race.

Mad Hedge Biotech & Healthcare Letter

May 19, 2020

Fiat Lux

Featured Trade:

(PFIZER’S LATEST COVID-19 VACCINE ENTRY)

(PFE), (BNTX), (MRNA), (INO), (CTLT), (SVA), (EBS), (MYL)

Clearly, the long-term solution to this health crisis, and possibly the only hope we have to returning to “normal,” is a safe and effective vaccine.

Companies and health experts around the world have stepped up to that challenge, with investors eagerly anticipating the stocks of the businesses to successfully deliver a vaccine to catapult in value overnight.

This is one of the driving forces behind Pfizer’s (PFE) relentless pursuit of a coronavirus vaccine.

Here’s a quick recap of where Pfizer was before this major announcement.

Pfizer was first recognized as an aggressive player in the vaccine race when the healthcare giant partnered with German biotechnology company BioNtech (BNTX).

After months of working together, Pfizer announced that it aims to produce 10 million to 20 million doses of COVID-19 vaccine by the end of 2020.

So far, Pfizer is testing at least four distinct variations of its vaccine called BNT162. The trials will test roughly 360 individuals, with the study expanding to involve thousands of volunteers if one or two variations of the vaccine indicate progress.

Conclusive data will be available in June or July this year. Meanwhile, Pfizer’s coronavirus vaccine candidate, co-created with BioNtech, is projected to be ready for launch by October.

In an effort to make room for the production of BNT162, Pfizer decided to outsource the production of some of its own branded products to various manufacturers such as Catalent (CTLT).

This move means that instead of paying contract manufacturers to produce millions of doses of a vaccine that might fail to even leave the warehouse, Pfizer has taken it upon itself to produce BNT162 in its own facilities.

According to the company’s estimates, it will cost approximately $150 million to produce BNT162. Since Pfizer is using its own facilities, it could jumpstart the distribution of up to 20 million doses of COVID-19 vaccine even before 2020 ends.

This move to ramp up the manufacture of an experimental drug candidate is a surprising gamble for Pfizer. However, the possibility of having millions of doses of this potential vaccine ready to ship at a moment’s notice could make it a worthwhile risk.

In terms of competition, Pfizer is racing against several biotechnology companies searching for a COVID-19 vaccine in the US and abroad.

One of them is Moderna (MRNA), which has a $19 billion market cap and funding access worth $2.4 billion including government endowment.

Moderna collaborated with Lona (OTC: LZAGY), which is an international chemical manufacturer, to scale up its production power.

Apart from this, smaller biotechnology companies like Inovio Pharmaceuticals (INO) and Novavax (NVAX) are involved in the COVID-19 vaccine race as well.

Inovio is backed by its history of vaccine research on the swine flu outbreak in 2009 and the 2013 avian flu.

Novavax, which has a modest market cap of $82.2 million, received government funding worth $4 million to help the company move forward with clinical trials.

Additional financial support was also sent by the Coalition for Epidemic Preparedness Innovations. In terms of manufacturing, Novavax has been working with Emergent BioSolutions (EBS) to meet production demands.

Outside the US, two of the frontrunners are Chinese companies CanSino Biologics and Sinovac Biotech (SVA).

The stocks of various micro-cap companies have been on the news since the COVID-19 vaccine race started. Several of these smaller firms used their newfound popularity to boost their stock price and generate additional capital to fund their operations.

I think there are several biotechnology and healthcare companies that warrant following. However, there remains a dearth of data on these companies working on the COVID-19 vaccine. Choosing the best stock from these names at this point demands too much guesswork, an investment strategy I have never endorsed.

The harsh reality is that most of these smaller companies will most probably never manage to get a program off the ground and into a conclusive efficacy trial. The main reasons are limited capital, restricted bandwidth, and lack of will to move forward.

Small companies, particularly in the biotechnology and healthcare sectors, typically lack the money and manpower to efficiently run a program without sacrificing the rest of their R&D efforts. For those companies that manage though, the pace will likely be too slow to actually merit a meaningful place in the market.

Investors looking to invest in the surging COVID-19 vaccine space should turn to companies that hold the greatest odds of success. That means larger and more established companies with global testing, regulatory, and manufacturing capacities.

This is not to dissuade anyone from taking a dip into the small-cap companies pool though.

Rather, I would recommend to simply keep these biotechnology companies on your watch list and see how the situation develops. After all, these are decent stocks on their own right.

Nonetheless, it’s still too early to tell how their long-term business models look like outside the search for a coronavirus vaccine.

In comparison, Pfizer has a proven track record of being a great investment. The company has been showing off a decent dividend growth for 10 consecutive years, reporting an annualized dividend worth $1.52 per share.

More importantly, this biotechnology and healthcare company is showing no signs of slowing down anytime soon. In 2019 alone, Pfizer introduced six new drugs on the market and shared that it has 95 more in its pipeline.

Keep in mind as well that Pfizer’s current price of roughly $37 per share -- a far cry from its 52-week high that reached $44.56 -- is significantly lower than the industry average at the moment. For a stock that presents such a wealth of opportunities, Pfizer offers significant value to its investors.