Mad Hedge Biotech & Healthcare Letter

January 19, 2021

Fiat Lux

FEATURED TRADE:

(CAN NOVAVAX EXTEND ITS WINNING STREAK?)

(NVAX), (MRNA), (PFE), (AZN), (BNTX), (BTC)

Mad Hedge Biotech & Healthcare Letter

January 19, 2021

Fiat Lux

FEATURED TRADE:

(CAN NOVAVAX EXTEND ITS WINNING STREAK?)

(NVAX), (MRNA), (PFE), (AZN), (BNTX), (BTC)

Would you believe that there was a bigger winner than Bitcoin (BTC) in 2020?

Amid the fanfare generated by COVID-19 vaccine developers like Moderna (MRNA) and Pfizer (PFE), there’s one biotechnology company that has quietly boosted its humble $4 share price to an impressive $128: Novavax (NVAX).

As incredible as that sounds, this isn’t the most unbelievable prediction for Novavax.

Despite recording a jaw-dropping 2,600% increase last year, this Maryland-based biotechnology company is projected to sustain the momentum in 2021 and beyond.

Let me share how Novavax can achieve a long-lasting winning streak.

Unlike Moderna and Pfizer, Novavax did not utilize RNA technology to develop NVX-CoV2373. Instead, the company opted for a more established approach.

The decision to pursue a more established technology could be viewed as a cost-cutting strategy for Novavax.

Doing so means dramatically lowering supply chain pressures, such as storage issues.

In effect, the Novavax vaccine would be the more convenient option that offers an equally potent result.

At this point, Novavax has yet to reveal its Phase 3 trial results. The tests, which involve trials in the UK, would prove to be the turning point for the company’s future.

Here’s a rough estimate of how the results could affect Novavax shares.

If the results show that NVX-CoV2373 is 90% effective, this would put the vaccine in the same league as Pfizer and Moderna. Consequently, shares will go up by 30% with this news.

Meanwhile, an efficacy result clocking in at less than 80% would have the stock falling by up to 20% primarily due to the strong competition in the COVID-19 market.

Approximately $40 billion in COVID-19 revenue is at stake this year.

While competitors Pfizer, Moderna, and AstraZeneca (AZN) have already had their vaccines approved for emergency use, Novavax still has a strong chance of getting a piece of the action.

Despite these candidates getting rolled out in other countries, Novavax’s NVAX-CoV2373 remains a heavy favorite among experts and analysts alike.

At this rate, NVX-CoV2373 could generate at least $4 billion of the $40 billion COVID-19 market in 2021.

Considering that Novavax has an $8 billion market capitalization, this alone more than justifies the company’s valuation.

Admittedly, Pfizer and Moderna hold the competitive advantage in being the first to market. It wouldn’t be surprising if both would end up gobbling up market share while Novavax awaits regulatory approval.

More importantly, both have achieved the coveted name recognition when it comes to COVID-19 vaccine so that could offer them power in the soon-to-be-crowded marketplace down the road.

However, both vaccine leaders have a considerable drawback.

Their vaccines require extremely delicate storage and transportation.

In fact, Pfizer and BioNTech’s (BNTX) BNT162b2 must be stored at minus 94 degrees—a requirement that not all countries, much less commercial distributors could adhere to.

This is where Novavax’s vaccine comes in.

NVX-CoV2373 can be stored and transported at refrigerated temperatures. This means it would be easier to distribute particularly in remote areas.

Any hiccups with storage or transportation involving the Moderna or Pfizer vaccines could offer Novavax an opening to generate vaccine sales that would otherwise no longer be available.

This scenario would translate to a more dominant presence of Novavax in the second half of 2021 until the early part of 2022.

Pfizer and Moderna may have been the first to market, but Novavax’s vaccine holds the potential to generate a sizable impact on sales over the long term.

In terms of revenue, the vaccine would be a significant boost for Novavax. It would transform from a zero product revenue to billions in a short period.

While Novavax has yet to announce the official pricing for the product, we can use its US price of $16 per dose as a benchmark for the rest of the contracts.

So far, Novavax has secured roughly orders for 300 million doses in the US alone. This would amount to $4.8 billion in sales—and all signs point to the number climbing higher this year.

Novavax has been ramping up its capacity to produce as many as 2 billion doses by mid-2021.

In comparison, Pfizer has a maximum capacity of 1.3 billion doses this year while Moderna would peak at 1 billion.

Evidently, Novavax holds an edge over the two companies in terms of capacity to fill orders.

Outside its COVID-19 efforts, Novavax has another potential blockbuster in its pipeline.

Although data is sparse, the company is expected to file for regulatory approval for its experimental flu vaccine called NanoFlu.

Oddly enough, NanoFlu was the reason that Novavax trounced the cryptocurrency surges in 2020.

Investors got all fired up following the promising showing of the flu vaccine candidate, with the stock gaining unprecedented attention when it reported remarkable results in a head-to-head study against the leading flu vaccine in the market today, Sanofi’s (SNY) FluZone Quadrivalent.

With all these in mind, Novavax’s earnings outlook is showing strong signs of even more stellar and stronger performance than that of Moderna this year.

So far, earnings per share for Novavax this year is estimated at $21 while Moderna’s is $10.

Another possible game-changer for Novavax is its plan to combine a flu-coronavirus vaccine to be marketed post-pandemic.

Before making any moves though, it’s important to invest in Novavax with all the facts out in the open.

Inasmuch as it’s a promising stock, this is still a risky investment. This means that only aggressive investors should consider buying this biotechnology stock.

In a number of ways, Novavax and Bitcoin share some similarities.

Both are speculative assets that could either skyrocket or sink. They’re extremely attractive to aggressive investors on the lookout for big wins but also unafraid of massive risks.

The main difference is that with Novavax, it’s simpler to understand the reason for its rise or fall.

The potential drivers for its success or failure appear to be less cryptic than those behind the cryptocurrency.

Mad Hedge Biotech & Healthcare Letter

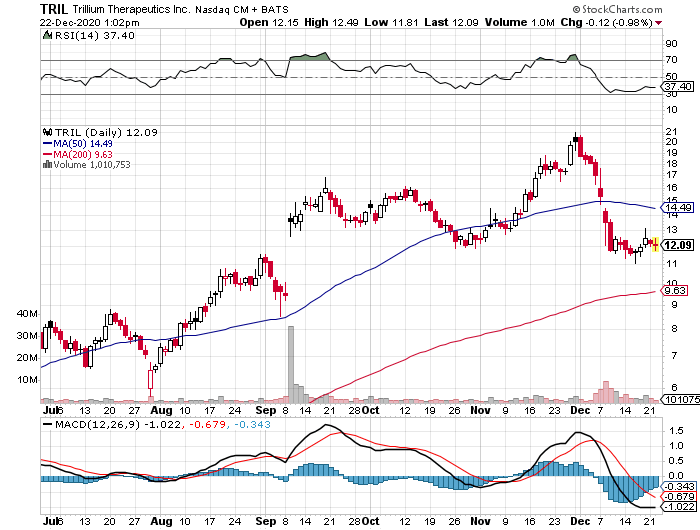

December 22, 2020

Fiat Lux

FEATURED TRADE:

THE MOST FAMOUS CANCER STOCK YOU’VE NEVER HEARD OF

(TRIL), (NVAX), (PFE), (IMMU), (SHOP), (GILD), (ABBV)

Biotechnology stocks have proven time and time again to be excellent growth vehicles for risk-tolerant investors.

Underscoring this claim are companies like COVID-19 vaccine frontrunner Novavax (NVAX), which generated jaw-dropping returns on capital for their investors within an impressively short period.

Now, another biotechnology stock is showing telltale signs of following their footsteps: Trillium Therapeutics (TRIL).

Trillium’s story is a familiar one in the biotechnology industry.

Trading only in the penny stock range back in 2019, the company’s share price practically quadrupled since the start of 2020.

Taking into consideration that this meteoric rise actually happened while COVID-19 was blasting the world to smithereens, it’s hardly surprising that this news didn’t receive much media attention.

Trillium’s shares are currently up by an astounding 1,260% -- and the company still has so much room to grow from here.

For context, Trillium had a market capitalization of $7 million in November 2019. This number skyrocketed to $1.3 billion since its shift to cancer technology.

Although a lot of factors came into play, the key turning point for Trillium was when the company decided to go all-in on its cancer programs.

Ultimately, Trillium’s goal is to challenge chemotherapy.

The move to shutter its lead programs on tumor treatments and instead focus on developing cancer-fighting technology was the gamble of a lifetime for the company.

This gutsy move impressed investors, and Trillium was never the same since then.

Today, Trillium is the No. 1 stock on Canada’s S&P/TSX Composite Index, overtaking its previous leader e-commerce giant Shopify (SHOP) by almost 10-fold.

In the US, Trillium shares rank as the No. 4 best-performing company on the Nasdaq Composite Index.

While its epic stock market rally may have some investors feeling left out, all signs point to further gains in the future even for those who missed the initial boom.

Among the major capitalists of this biotechnology company is giant biopharmaceutical company and COVID-19 vaccine leader Pfizer (PFE), which invested $25 million in Trillium’s common stock.

While this equity stake may seem small in relation to Pfizer’s $212.16 billion market capitalization, this initial show of confidence is hailed as a prelude to an even bigger investment in the future.

So far, the most exciting cancer treatments in Trillium’s pipeline are TTI-621 and TTI-622.

These programs are in the same class of emerging cancer technologies, called CD47-based therapies, that prompted Gilead Sciences’ (GILD) $4.9 billion acquisition of Forty Seven, Inc. in April this year.

Aside from Gilead, AbbVie (ABBV) has also been reported to have invested a huge sum in this technology.

In simplest terms, CD47-based therapies can bypass the “don’t eat me signal” put up by some cancer cells in an effort to evade immune detection.

Thus far, both TTI-621 and TTI-622 have been showing promising results. Trillium recently announced that it will increase the dosage in these programs.

While Trillium leaders have not been specific in terms of being open to an acquisition, their recent statements indicate that they are not completely opposed to one.

It’s either that or a partnership with a company as big or even bigger than Pfizer.

As with all the biotechnology stocks, however, there will always be a risk.

For Trillium, the most evident one is competition.

While it’s true that the company has been recognized as the leader in the CD47 arena, more and more competitors are entering the immuno-oncology space.

Right now, the most obvious rival is Gilead, which added Immunomedics (IMMU) to its arsenal via a $21 billion acquisition deal.

Given the sheer amount of money that Gilead has been spending to practically corner the immuno-oncology market, it’s to be expected that more biopharmaceutical titans will enter the fray.

This is one of the reasons Trillium has been tagged as a prime candidate for a massive acquisition deal soon. So far, Pfizer is considered the most probable suitor.

Despite its astonishing performance this year, Trillium’s market capitalization still remains within the small-cap territory. That’s to be expected since its lead assets are still undergoing trials.

Considering that it is an early-stage biotechnology stock, Trillium does not have much in terms of income.

However, the company does have enough cash to last for a while. At the moment, it has $130 million cash.

With its total expenses of $38.8 million in 2019, I say this could offer the company more than three years of breathing room financially.

But it would be shocking if Trillium’s value won’t enter the large-cap territory (higher than $10 billion) if and when the company’s high-value assets reach the late-stage studies.

The fact that it’s also an attractive acquisition candidate offers incredible incentive to its investors.

Simply put, Trillium’s stock could get as much as 1,000% gain over the coming two to three years, making it an ideal investment for risk-tolerant investors.

Mad Hedge Biotech & Healthcare Letter

December 8, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS STOCK A DISCOUNT TO MODERNA?)

(NVAX), (MRNA), (PFE), (BNTX), (AZN), (JNJ), (MSFT)

Eighteen months ago, an unknown vaccine developer called Novavax (NVAX) confronted an existential terror: getting delisted by the NASDAQ stock index.

This threat came on the heels of the company’s second failed vaccine study in less than three years, plunging Novavax shares to less than $1 for 30 straight days and triggering a warning from NASDAQ.

Desperate to keep the company going, Novavax sold two of its manufacturing plants in Maryland, cutting the payroll by over 100 employees.

By January 2020, Novavax only had 166 employees in its roster and was priced at $4 per share.

By December of the same year, Novavax more than tripled its workforce and the stock has risen to $128 per share.

What a difference a year—and a global pandemic—could make.

To date, Novavax stock has already skyrocketed to over 3,000%—shattering even the wildest dreams of its early investors. And this isn’t the best news yet.

Like Moderna (MRNA), another small biotechnology that skyrocketed this year, Novavax is projected to enjoy more room for growth in the succeeding years.

Despite the similarities in their achievements, there has been a notably sizable gap between the valuations of these two biotechnology companies in the Operation Warp Speed list.

The valuation gap would probably make more sense now, especially since Moderna has the golden ticket when it comes to high efficacy results for the COVID-19 vaccine, while Novavax has yet to prove its candidate’s worth.

However, Novavax isn’t out of the race just yet. Novavax plans to end 2020 with a bang by launching pivotal COVID-19 vaccine trials for its candidate, NVX-CoV2373, in the US and Mexico.

While the old saying, “The early bird gets worm,” is frequently accurate and we’ve seen how first-movers generally attain the highest success, this may not be the case here.

In view of the COVID-19 vaccine race, there’s a realistic possibility that Novavax will come out as a bigger winner than Pfizer (PFE) or Moderna (MRNA) in the long run.

Admittedly, it’s encouraging for vaccine developers to know that RNA vaccines, such as Pfizer and BioNTech’s (BNTX) BNT162b2 and Moderna’s mRNA-1273, are effective.

It’s definitely even more encouraging to learn that the second type of vaccine, which is being developed by AstraZeneca (AZN) and Oxford, also offer successful trials.

However, the potential of Novavax’s vaccine candidate proves that there are many ways to skin the cat.

This protein-based vaccine, which also caught the attention of Microsoft (MSFT) co-founder Bill Gates, is expected to show the best results among all the developers.

Although its competitors are months ahead in their tests, NVX-CoV2373 actually outshone the rest of the developers on key metrics in the monkey and even human tests.

Moreover, Novavax’s technology offers versatility, which means it can be applied to other vaccines and treatments as well.

If NVX-CoV2373 gains approval, the company will easily continue this momentum in 2021 and in the next years.

The market opportunity presented by the demand for a COVID-19 vaccine is unbelievable.

Priced at $16 per dose, Operation Warp Speed shelled out $1.6 billion to buy 100 million doses of the Novavax vaccine.

Considering that this is a two-shot vaccine, this would only cover 50 million people.

Although the price may be higher or lower depending on various factors, $16 per dose is a good starting point for a back-of-the-envelope calculation.

What we know so far is that Novavax has already secured agreements to manufacture more than 2 billion doses.

Taking into consideration the price point of $16 for each dose, that easily gives the company a potential revenue of a whopping $32 billion in 2021.

The upside is surreal.

Plus, we still have no guarantee whether the need for a COVID-19 vaccine will be a one-time requirement or a yearly ritual like flu shots, which Novavax also has covered with the production of its new drug, Nanoflu.

As the market continues to swoon over the huge updates from Pfizer and Moderna, it no longer comes as a surprise when other candidates are glossed over.

Novavax isn’t about to start selling its COVID-19 vaccine tomorrow, but it’ll probably release critical data in the next months.

Assuming that it gets regulatory approval by the first half of 2021, it’ll begin to realize the upside almost instantaneously.

At $8 billion market capitalization, Novavax stock could easily triple to $24 billion by the time the vaccine is released.

I believe Novavax offers a potential long, and I find myself getting bullish on this stock.

Although it has a limited pipeline at the moment, I think positive data from its COVID-19 vaccine candidate will serve as a catalyst for this stock to trade much higher in the future.

While I can see that Novavax is widely considered as a dark horse in this race, I believe it’s going to be a dark horse that can lead us out of this darkness soon.

Mad Hedge Biotech & Healthcare Letter

December 3, 2020

Fiat Lux

FEATURED TRADE:

(IT’S TIME TO JOIN THE COVID-19 VACCINE BANDWAGON)

(PFE), (BNTX), (MRNA), (NVAX), (AZN), (JNJ), (MRK)

In the history of corporate ventures, Pfizer (PFE) is one of the select few that can claim that their contributions genuinely contribute to the betterment of mankind.

This giant biopharmaceutical company has rapidly developed a promising vaccine candidate for the deadly COVID-19—an achievement that could potentially put an end to the global pandemic that has transformed 2020 into an apocalyptic year.

To date, Pfizer and its partner BioNTech (BNTX) have submitted the vaccine, BNT162b2, to the FDA for review—a move that could take us all a step closer to returning to our normal everyday lives, where we can be with our friends and loved ones without fretting over deadly infections.

If BNT162b2 gains approval, Pfizer and BioNTech can start the distribution by Christmas.

As expected, the COVID-19 vaccine will provide a quick and substantial boost to the company’s revenue this year.

Outside its COVID-19 program, Pfizer has a number of blockbuster treatments that have been generating steady growth despite the health and financial crises this year.

At the top of the list are breast cancer drug Ibrance and stroke and blood clot medication Eliquis. Other stars of Pfizer’s strong lineup include rheumatoid arthritis medication Xeljanz, heart failure treatment Vyndaqel, and prostate cancer drug Xtandi.

In terms of its pipeline, Pfizer has at least six programs queued for regulatory approval and an additional 21 candidates undergoing late-stage trials.

While Pfizer and BioNTech are leading the charge in the COVID-19 vaccine race, this is not necessarily a winner-take-all-market.

Days after Pfizer announced the results of its trials, fellow vaccine developer Moderna (MRNA) also released promising data. Another biotechnology company, Novavax (NVAX), has been sending out impressive results as well.

Even AstraZeneca (AZN), which has been working with Oxford, offered good news despite the delays in its own trials.

Meanwhile, Johnson & Johnson (JNJ) and Merck (MRK) have been making progress in their own COVID-19 programs as well.

However, there’s a crucial role played by Pfizer’s success.

It introduced to us the possibility of jumpstarting a vaccine program and shortening the development period that typically takes at least 10 to 15 years to complete.

More impressively, Pfizer has managed to come up with a vaccine with 95% efficacy – an amazing feat considering that 90% to 95% of vaccine trials tend to fail from the very beginning.

Most importantly, Pfizer’s recent results showed that we can now explore new options in vaccine development.

Taking BNT162b2 into consideration, this program opened doors for treatments created based directly on the molecular and even genetic structure of viruses.

Needless to say, Pfizer is a compelling stock to buy at a time when it is the norm to complain about having nothing to purchase at a reasonable price.

Additionally, Pfizer shares offer a dividend yield of 4.2% – a major advantage in a financial market that appears to be starved for any sort of security.

For those patient enough, the current conditions look to be ripe to use options to make the most of the short-term volatility to position yourselves for long-term gains.

By selling puts and buying calls, you can get the options market to pay them to purchase stock at cheaper prices and even participate in any rallies.

With Pfizer stock priced at around $36.18 these days, you can sell the January $36 put and buy the January $38 call for a credit of roughly 60 cents.

If Pfizer stock rallies, then you profit.

If the stock falls, then you can just buy it at the put strike price, although at a minimal discount because of the credit, or simply cover the put and move on.

If Pfizer stock hits $43 at the January expiration though, the call would be worth $5.

This risk-reversal plan is based on the prediction that good things are expected to happen to Pfizer—and to the world—soon.

Obviously, the key risk is that the stock rolls over and falls before the January expiration.

Given the new COVID-19 vaccine, however, that seems highly unlikely.

Mad Hedge Biotech & Healthcare Letter

October 22, 2020

Fiat Lux

FEATURED TRADE:

(IS THIS COVID-19 VACCINE OUTLIER ON THE FAST LANE?)

(NVAX), (PFE), (AZN), (JNJ), (SNY), (MRNA), (TAK)

It is not at all surprising that the biggest names in the healthcare industry are dominating the COVID-19 vaccine race.

After all, Big Pharmas such as Pfizer (PFE), AstraZeneca (AZN), Johnson & Johnson (JNJ), and Sanofi (SNY) are backed with vast resources that even media favorites like Moderna (MRNA) find challenging to compete against.

For months now though, going head to head with these big-name frontrunners is a clear outlier: Novavax (NVAX).

So far, there are only 10 COVID-19 vaccine candidates that have reached late-stage testing and Novavax’s NVX-CoV2373 has been performing at par (if not better) than its rivals—and the market has definitely noticed.

When 2020 started, Novavax’s market capitalization was less than $130 million and traded at roughly $4 per share.

Ten months into the pandemic, this small biotechnology company’s market cap grew to over $6.5 billion and has been trading at $110 per share—and that is already after a price decrease in the past weeks.

Given the disparity in its size and resources compared to its competitors, it’s safe to say that Novavax has been punching way above its weight class particularly in terms of landing supply agreements for its COVID-19 program.

Novavax first received a CEPI grant in March worth $4 million, which was immediately dwarfed by the $384 million the biotech company got in May.

In a matter of months, Novavax joined the major league players and secured a $1.6 billion funding courtesy of the US government’s Operation Warp Speed program.

In exchange, the biotech company will supply 100 million doses of NVX-CoV2373 to the US upon approval.

Novavax also inked an agreement with the UK for 60 million doses and another with Canada for 76 million doses.

Novavax has also landed deals with Japan through Takeda Pharmaceutical (TAK) and India via the Serum Institute of India.

As expected, the grants and supply agreements were perceived as votes of confidence on Novavax’s work and the company reaped the rewards.

In March, the prices started moving from less than $10 per share to almost $50.

By May, the price moved up to roughly $80 per share.

After its Operation Warp Speed contract in July, Novavax’s price per share soared all the way to $189 before eventually falling to $110 this October.

Novavax has only conducted late-stage testing in the UK. But, Phase 3 is expected to begin in the US soon as well.

Admittedly, a lot is riding on NVX-CoV2373.

However, the company has actually offloaded the majority—if not all—of its financial risks linked to the program.

Riding the momentum of its COVID-19 vaccine candidate, Novavax has been working on a related influenza vaccine called Nanoflu.

Given the market size for this, Nanoflu is estimated to rake in an annual revenue somewhere between $550 million and $1.7 billion.

Another potential blockbuster is respiratory syncytial virus (RSV) vaccine ResVax, which is projected to reach peak sales of $2 billion.

Novavax is also working on a vaccine candidate for the Ebola virus, the Middle East Respiratory Syndrome (MERS-CoV), and Severe Acute Respiratory Syndrome (SARS).

While NVX-CoV2373 is anticipated as Novavax’s moneymaker in the coming years, the biotech company can only realistically expect massive sales from this until 2023.

Looking at the company’s manufacturing partnerships and the aggressive timeline it has taken, Novavax is expected to produce 2 billion doses of its COVID-19 vaccine by mid-2021.

This is great news for its investors because of Novavax’s smaller market capitalization compared to its competitors.

Since the biotech company is projected as one of the first companies—if not the first—to offer a vaccine, then it can cover a substantial market share before its bigger rivals take over the market.

Even if Novavax prices its COVID-19 vaccine cheaply, say, $10 per dose, it can still generate $20 billion in annual sales.

Moreover, the late-stage success of NVX-CoV2373 will definitely cause Novavax’s stock price to skyrocket.

Despite this potential though, it’s important to keep in mind that this biotech company still has a way lower market cap than its rivals.

That means its share price will move a lot higher compared to the stocks of the other vaccine leaders.

Therefore, Novavax’s small size is not a negative for its investors—it is actually an advantage.

So for biotech investors who are searching for a promising COVID-19 vaccine stock, there’s nothing cheaper and more promising than Novavax.